The Closer – Spreads, Sentiment, Rates Vol – 8/18/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a look into credit spreads (pages 1 and 2) and how rates volatility has shaped up (page 3). We finish with an update on positioning (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

International Breakouts to Watch

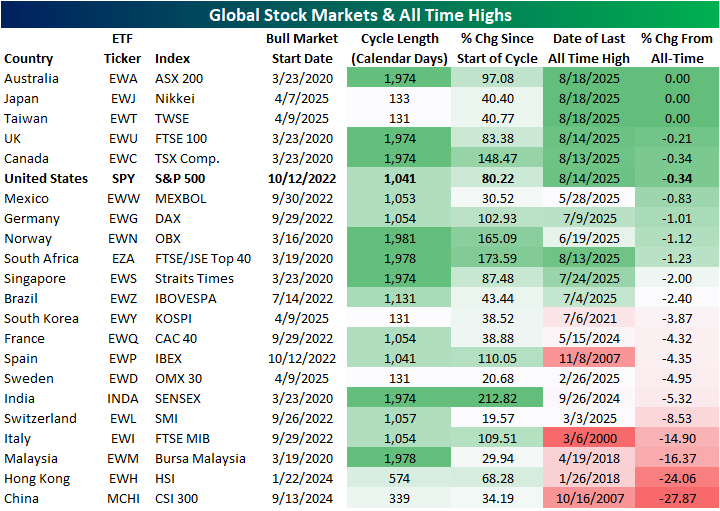

The S&P 500 has seen a slight dip off of record highs in the past few days with many other equity markets around the globe seeing similar price action. As shown below, of 22 major global markets we track, there are currently seven that are within 1% of record highs (priced in local currencies). That includes the S&P 500 which is 0.34% away and three countries trading at record highs as of mid-day Monday: Australia, Japan, and Taiwan. Of those, Japan and Taiwan are actually some of the fresher bull markets (all 22 of these countries are currently in bull markets) whereas Australia is still in the same bull market that has been in place since the COVID Crash lows. The four others within 1% of a high include the UK, Canada, United States, and Mexico. Mexico is the only country within 1% of a fresh high that has yet to have a record close in August. As for the other countries that are further below prior highs, Italy, Malaysia, Hong Kong, and China are the only ones that are still more than 10% away.

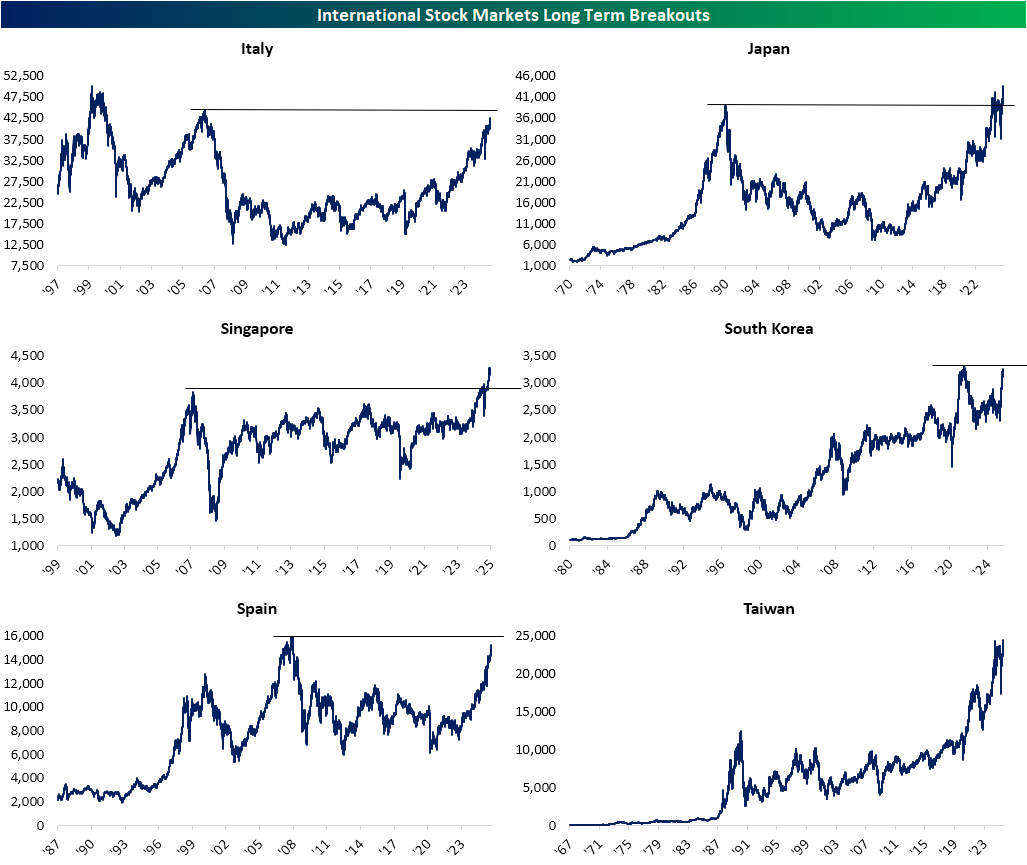

As discussed above, Japan is one of three countries trading at fresh all time highs. While notable on its own, Japan’s rally is even more impressive when put in the context of the past several decades. After peaking on December 29, 1989, Japan didn’t move into the black from those levels until February of last year. While the past 18 months since that initial breakout have seen some fluctuations around those prior highs, this latest rally more clearly defines the breakout. Elsewhere in the APAC region, Taiwan is also at a fresh highs after recently breaking out above more short term resistance of its highs from July 2024. Those are not the only two long term breakouts though. In the first week of this year, Singapore finally reclaimed its peak from October 2007. Outside of the spring dip as trade became front and center, Singaporean equities have left those prior highs in the dust.

While those breakouts have been confirmed, a few other areas are setting up to breakout. Italy and Spain have rallied solidly so far into the 2020s, and as a result of those gains are pressing up towards highs not seen since 2007. For Italian equities, a breakout above those levels would still leave resistance at its early 2000 all time high in play whereas a Spanish breakout would result in all time highs. Over in South Korea, a post-pandemic stock surge sent the KOSPI up to records in the first half of 2021. However, it has now been a few years below those highs. That is until this year. The KOSPI has rallied over 30% since this April’s lows and now it is within 4% of that 2021 peak.

ICYMI: New Charts from Latest Bespoke Report

Chart of the Day: The “So What?” Earnings Season

Bespoke’s Morning Lineup – 8/18/25 – Rocky Road

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you’re afraid – don’t do it, – if you’re doing it – don’t be afraid!” – Genghis Khan

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Given some of the stronger inflation data, in hindsight, last week could have been worse. Looking at futures this morning and the performance of international markets overnight and this morning, it appears as though investors thought the same over the weekend. Futures are lower, but the losses are admittedly modest, so maybe it’s just the bulls taking a breather. This week will be a busy week for earnings from retailers, which should shed some light on how tariffs are impacting results, but for today, things are pretty quiet as the only report on the calendar is Homebuilder Sentiment at 10 AM, and the only earnings report of note is Palo Alto Networks (PANW) after the close.

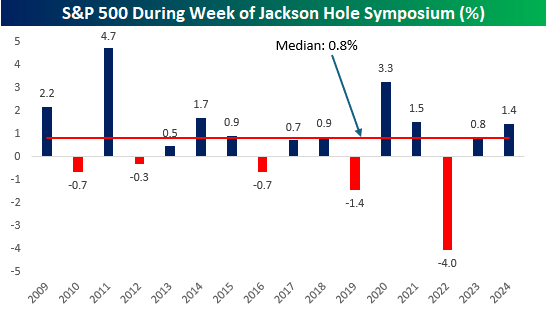

The end of August is a popular time for vacations, and the Fed is no exception as the Kansas City Fed hangs up its ‘gone fishing’ sign and holds its annual meeting every year at the Jackson Lake Lodge in Grand Teton National Park. Fed officials are only human, so like the rest of us, they’ll never turn down the opportunity for a ‘work’ conference that happens to be at one of the most beautiful and scenic places in the world. The conference is so ‘intense’ that the chair of the Federal Reserve himself (or herself) even makes the trip to give a speech every year.

With Fed officials from around the world attending the conference every year, members of the media who follow the Fed also attend the conference each year. With all these policymakers, cameras, and microphones in one place, the result is that many newsworthy events have ended up taking place. In 2010, Fed Chair Ben Bernanke laid the groundwork for quantitative easing, which became a staple of Fed policy in the ensuing years. Then in 2014, ECB chief Mario Draghi acknowledged that inflation expectations in Europe were dangerously below the central bank’s 2% target, setting the stage for more fiscal and monetary stimulus.

More recently, back in 2022, when inflation was still raging, markets were hoping that Powell would use the conference as an opportunity to take a kinder and gentler approach to markets reeling from an aggressive run of rate hikes. Shortly after he stepped up to the podium, however, he dashed any of those hopes. He started his speech with, “Today, my remarks will be shorter, my focus narrower, and my message more direct.” Then he finished with the promise that “We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.” In other words, the beatings will continue!

With Powell scheduled to speak at the end of the week, and facing intense pressure from the President to cut rates (who knows maybe President Trump will hire one of those planes you often see at the beach towing a message behind it to further criticize Powell), anticipation to Friday’s speech is already high, and investors are expecting volatility, but how volatile does the market really get around the Jackson Hole speech?

The chart below shows the S&P 500’s performance in the week of the Jackson Hole conference every year since the end of the Financial Crisis in 2009. More often than not, it’s been a positive week. Of the 16 years shown, the S&P 500 has only been down five times, with only two years where the drop was more than 1% (2019 and 2022). Overall, the S&P 500’s median performance has been a gain of 0.8%.

Brunch Reads – 8/17/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Golden Greatness: On August 17, 2008, Michael Phelps won his eighth gold medal in a single Olympics, breaking a record held by Mark Spitz at the time, who had swam for seven golds at the 1972 Munich Games. Yes, that’s a record that stood for 36 years. Spitz is the second most decorated Olympic swimmer in terms of gold medals, with a total of nine. First, of course, is Michael Phelps with twenty-three medals across four Olympic Games. It’s hard to understate how staggering that number is. The milestone eight golds in the 2008 Beijing Games came in the 4×100-meter medley relay, where Phelps swam the butterfly leg and helped the US team set a world record time of 3:29.34. It was the culmination of a grueling schedule of 17 races in just nine days, with each gold accompanied by a world record or Olympic record. Phelps also became the overall most decorated swimmer at those games, leaving with 16 career medals (14 gold, 2 bronze). At that point, Soviet gymnast Larisa Latynina still held the record with eighteen Olympic medals from 1956–1964. Phelps surpassed her four years later at the London 2012 Games, where he earned his nineteenth career medal on July 31, 2012, in the 4×200-meter freestyle relay. If there is a textbook definition of “dominance,” Michael Phelps’ career is just that.

Economic Trends

The private sector can’t replace official statistics—but could be a great partner (PIIE)

After Trump ousted the head of the Bureau of Labor Statistics over accusations of “rigged” jobs data, questions flared about whether private companies could step in if official numbers lose credibility. The piece weighs the strengths of proprietary data against the irreplaceable scope, consistency, and public trust of government statistics, noting that even private metrics depend on public benchmarks. It warns that recent budget cuts, erosion of data confidentiality, and dismantling of expert advisory channels are undermining both public agencies and the very partnerships needed to modernize and enrich economic data. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – Healthy Rotation or Something More?

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. Get caught up on everything going on in the investment world with the stock market at new highs by reading this week’s newsletter. Click here to sign up now!

Bespoke’s Morning Lineup – 8/15/25 – Busy End for a Summer Friday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The greatest danger occurs at the moment of victory” – Napoleon Bonaparte

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

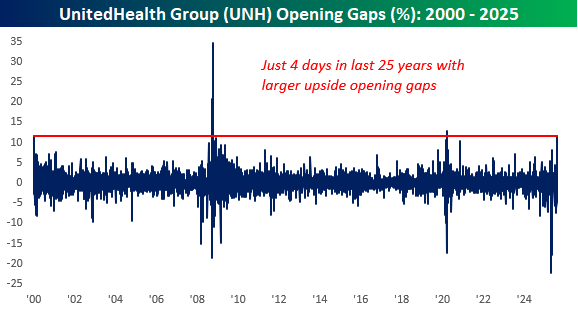

It may be a summer Friday, but there’s plenty of economic data to deal with this morning as Retail Sales and Import Prices were released at 8:30. At 9:15, we’ll get updates on Industrial Production and Capacity Utilization, and then at 10, Business Inventories and preliminary Michigan Sentiment will hit the tape. Heading into all the data, futures were mixed. Dow futures are sharply higher, but that’s all due to an 11% rally in UnitedHealth (UNH) following news that Berkshire Hathaway (BRK/b) has acquired a $5 bln stake in the company. Based on its current price, UNH is on pace to have its fifth-largest upside opening gap in the last 25 years.

It’s worth noting, though, that with the stock trading at $303 in the pre-market, it’s still trading more than 20% below its average closing price in Q2. We have no way of knowing Buffett’s cost basis on the position, but the odds are that Buffett is still underwater or barely positive on the position.

In Asia overnight, the Nikkei reversed Thursday’s losses following a better-than-expected GDP report and finished the day at another record with gains of over 1.5%. Chinese stocks were also higher, but economic data for the world’s second-largest economy missed forecasts as Retail Sales and Industrial output both came in weaker than expected.

European equities are higher across the board with modest gains as the STOXX 600 is up 0.20, led by France and Italy.

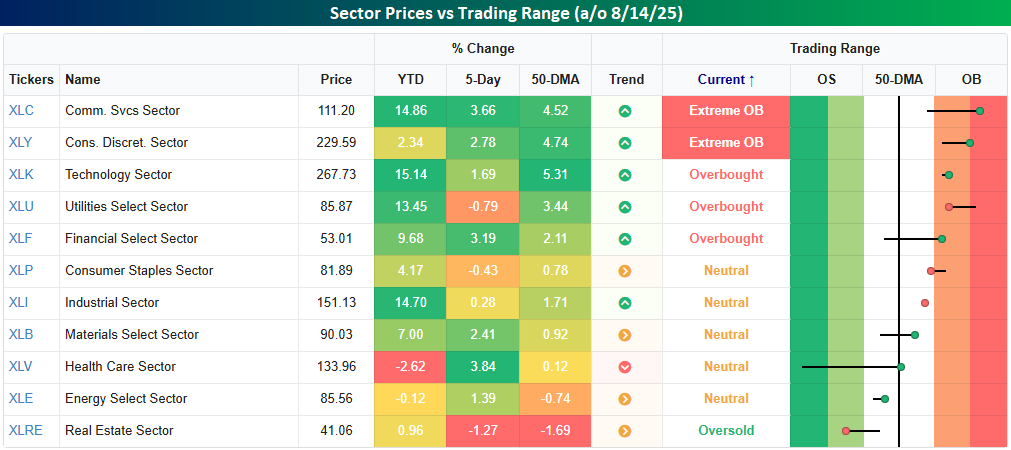

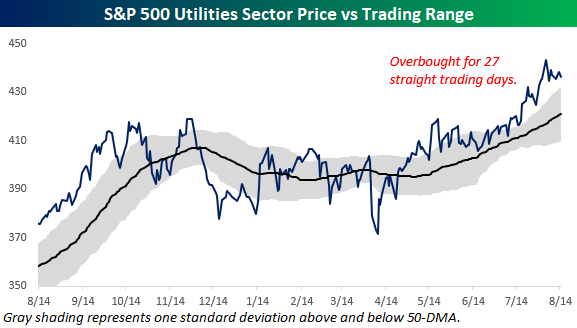

Looking through the various sectors and where they stand relative to their short-term trading ranges, we noted an interesting collection of sectors trading at overbought levels. Topping the list were Communication Services and Consumer Discretionary, which closed yesterday at ‘extreme’ overbought levels (2+ standard deviations above 50-DMA). Behind these two sectors, Technology, Utilities, and Financials all finished the day yesterday at overbought levels (1+ standard deviation above 50-DMA). It’s perfectly normal to see most of these sectors trading at overbought levels at a time when the market is in rally mode. The one exception is Utilities. Given its more defensive characteristics, Utilities tend to lag when the market is hitting all-time highs.

Utilities has been doing anything but lagging the broader market these days. As noted in last night’s Sector Snapshots report, the sector closed at overbought levels for the 27th day in a row yesterday.

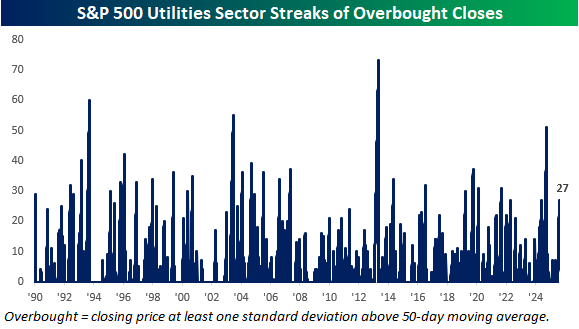

At 27 days, the current streak of overbought closes for the Utilities sector is the longest since last October. As the chart below illustrates, though, this current streak is hardly extreme. The streak last October ended at 51 trading days, and there have been many other longer streaks in recent years.

The Closer – PPI, Best of Breed, Transportation – 8/14/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, wekick off with a look into the latest PPI report (pages 1 and 2) followed by an update on our Best of Breed basket (pages 3 and 4). We finish with a look into the disconnect between the Dow Transports and the semis (page 5) and then close out with a look at the latest freight data from Cass (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

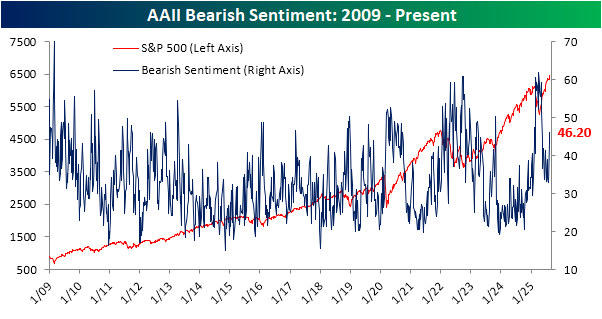

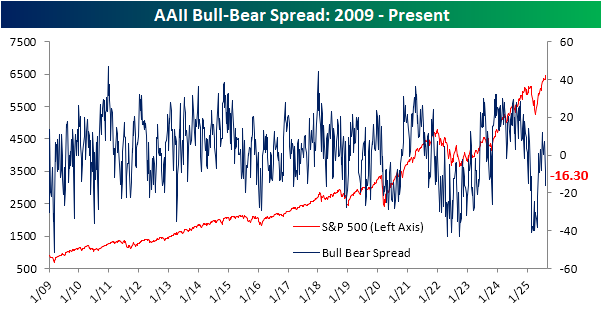

Sentiment and Stock Prices Diverge

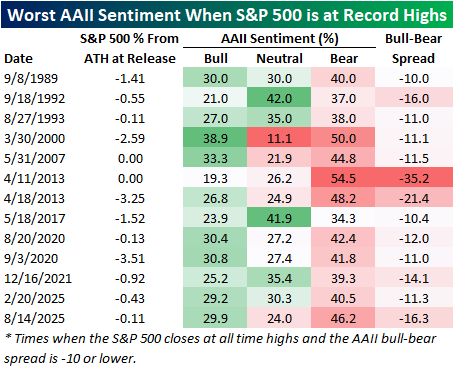

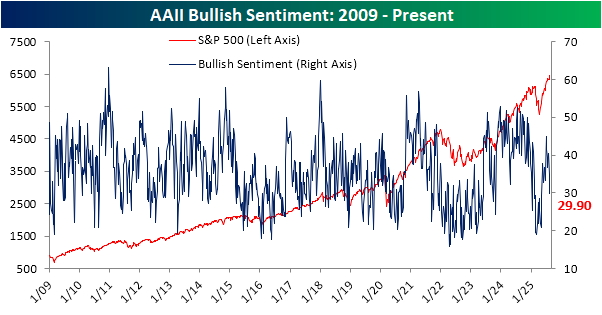

The S&P 500 has had a couple of closes at record highs since last week’s update on sentiment from the American Association of Individual Investors (AAII). However, looking at the latest update, you wouldn’t have guessed the market was doing well. Bullish sentiment shed five points week over week, down to 29.9%, a level not seen since early May.

The lack of bulls coincides with a spike in bears up to 46.2%, which is the most elevated since May 8th.

Put together, bears are now outnumbering bulls by 16.3 percentage points, which is the lowest spread since the spring. Additionally, holding aside the fact that the S&P 500 is near record highs, this week’s reading is significantly lower than normal. Historically, the average bull-bear spread has been +6.4, putting the current spread 1.25 standard deviations below the historical average. In other words, sentiment has tipped into what can be considered elevated bearish levels.

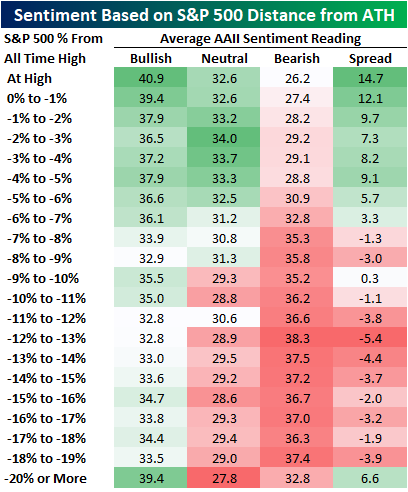

Again, it is one thing for bears to be out in full force to an extreme degree when stocks are weak. It is another entirely more surprising thing to see these levels when stocks are hitting record highs. In the table below, we show the average readings for bulls and bears in the AAII survey based on how far the S&P 500 is trading from all-time highs. As might be expected, sentiment has historically tended to be the most bullish/least bearish when the S&P 500 is closer to all-time highs. However, sentiment also tends to be more bullish when stocks are in pronounced pullbacks of at least least 20%. Comparing that to now, current levels of bullishness are about 11 points lower than what might be expected, and the level of bears is 20 points higher than what might be expected.

The degree to which investors reported as bearish was historic this week. In the history of the weekly AAII investor sentiment survey dating back to 1987, the bull-bear spread has only been lower in a week where the S&P 500 made an all-time high two other times. Both of those instances were in back-to-back weeks in 2013. Other than that, there have only been 13 weeks (including those two in 2013 and now) when the S&P 500 hit record highs and the bull-bear spread was -10 or lower. Before this week, there was also an occurrence earlier this year, almost exactly six months ago, right before the Q1 peak.