Chart of the Day: Down Goes Energy

ISM Non Contraction Index

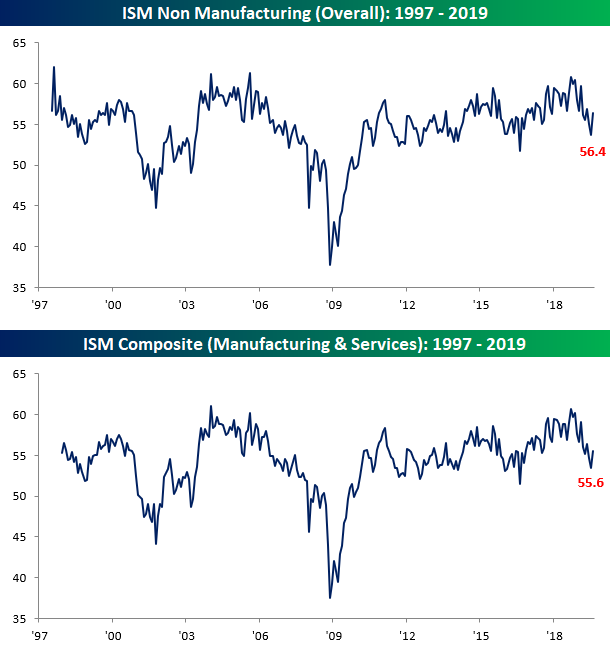

Just two days after one of the weakest ISM Manufacturing reports in years, Thursday’s release of the ISM Non-Manufacturing report for the month of August was a complete 180 from its Manufacturing counterpart. While economists were expecting the headline index to rise from 53.7 in July up to 54.0, the actual reading was considerably higher at 56.4. While it’s only the highest reading since May, the fact that it increased at all was a surprise to many. On a combined basis and accounting for each sector’s share in the overall economy, the Composite ISM for August rose from 53.4 up to 55.6 for its biggest monthly gain since February.

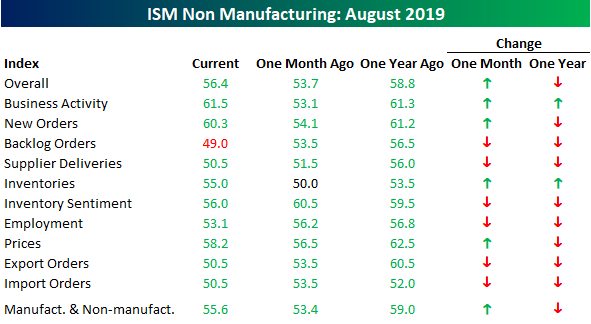

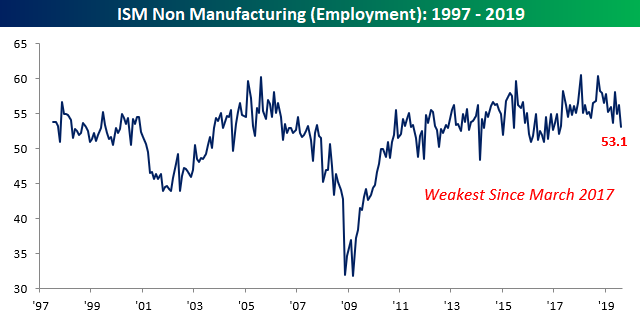

In terms of the breadth of this month’s report, it wasn’t particularly strong, but it wasn’t bad either. On a m/m basis, just four components increased while six declined. On a y/y basis, though, things were much weaker as just two components (Business Activity and Inventories) were higher this August than last. The biggest gainers on a m/m basis were Business Activity and New Orders, while on the downside Backlog Orders, Inventory Sentiment, and Employment saw the largest declines. In the case of Business Activity, that component’s 8.4 m/m increase was the largest since February 2008. Ahead of Friday’s Non-Farm Payrolls report, though, the decline in the Employment component is especially notable as its level is now the lowest since March 2017. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

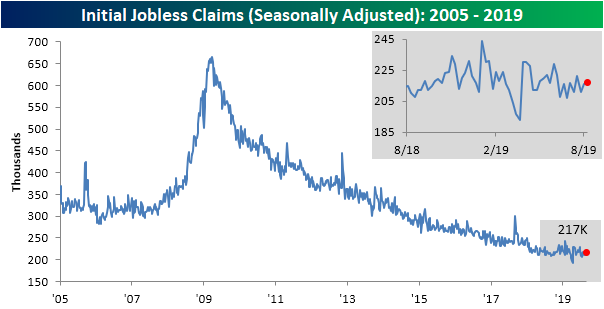

No New Lows Despite 100 Week Streak For Claims

This week’s reading on initial jobless claims was expected to come in unchanged from last week at 215K. Instead, the indicator disappointed slightly with last week’s number being revised up to 216K and this week’s data showing 217K new jobless claims filed. In terms of the seasonally adjusted data, claims continue to remain in the middle of the past year’s range. Even though they were also flat over the past year (visible in the inlaid chart below), claims have in fact still been at very healthy levels. The streak of consecutive weeks at or below 300K has now grown to 235 weeks. This week also marked the 100th straight week of claims coming in at or below 250K! As has been the case for some time now, claims may not be improving or degrading at any significant rate, but the labor market is still holding up just fine.

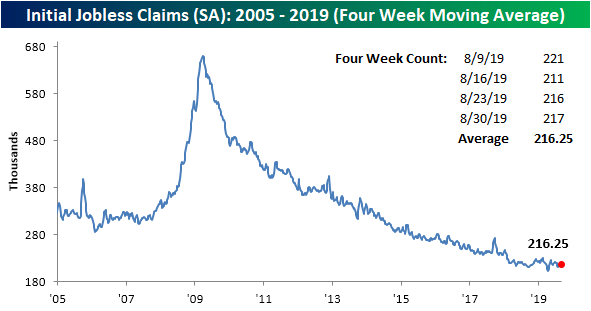

The four-week moving average reinforces this point as it has also been flat for the past year and a half outside of the spike lower in April. This week, the moving average ticked up to 216.25K as the lower reading of 211K from the first week of August rolled off the average to be replaced with this week’s higher 217K. Again, as with the weekly seasonally adjusted data, the moving average is still at healthy levels relative to history even though the pace of improvements has slowed. Fortunately, looking ahead to next week, there is a good chance the moving average can make a move lower as the recent high of 221K will come off the average.

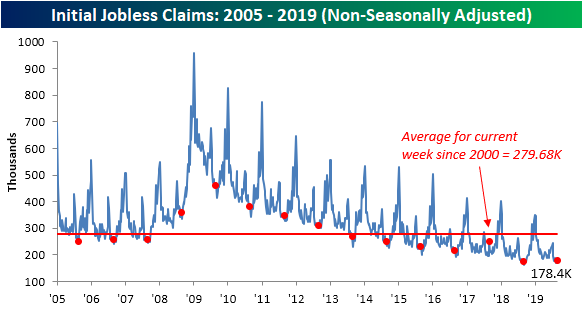

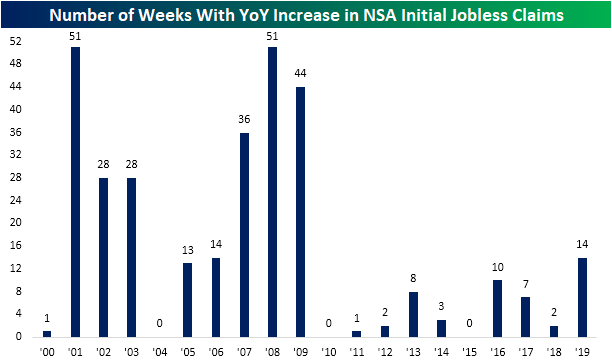

As we discussed last week, the end of August and beginning of September typically see the smallest average week-over-week changes in non-seasonally adjusted initial jobless claims data despite the yearly low typically coinciding around this time of year as well. That continues to hold true this week as the NSA data only rose by 1.5K compared to the average absolute move of 8K. This week’s reading of 178.4K is still well below the average for the current week since 2000, but it was 4.8K higher than the comparable week last year. The only other year of the cycle that the current week saw a YoY increase was in 2017 when it saw an unusual 32.9K increase YoY. Looking ahead to next week, the comparable week last year marked the lowest level in NSA data of the cycle at 162.6K. It would be a promising sign to see this low taken out, but given the higher frequency of YoY increases this year (second chart below), it is questionable if we will see that happen. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke CNBC Appearance (9/4)

Bespoke co-founder Paul Hickey appeared on CNBC’s Power Lunch on Wednesday to discuss markets heading into September. Please click the image below to view the appearance.

Bespoke’s Morning Lineup – Who Said Talk is Cheap?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Cross-Asset Recap, Trade, Beige, Fund Flows – 9/4/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a recap of price action in the S&P 500, VIX and credit spreads, EMFX, the USD, and precious metals. We then look at the US trade balance, including a look at trade between the US and China. We finish with a review of today’s Beige Book release and ICI fund flows.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Fixed Income Weekly – 9/4/19

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we discuss the extreme level of oversold readings for global bond yields.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

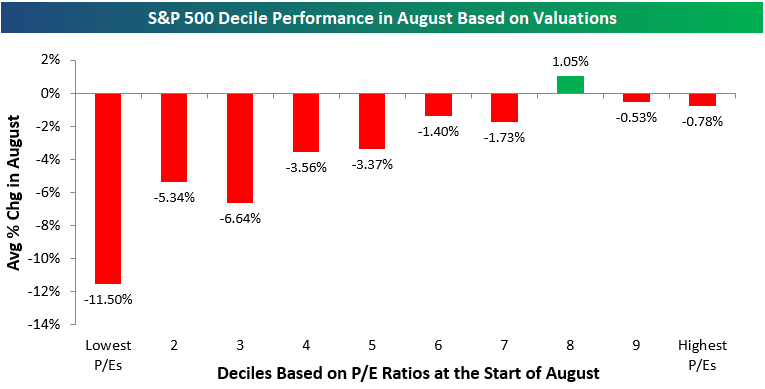

Low P/E, Low Return

Most investors are trying to forget about August performance as quickly as possible, but we wanted to highlight a noteworthy data set about the month before it gets too far into the rear-view mirror. At the end of every month, we run our decile analysis of the S&P 500 to see which stock characteristics drove performance the most. One characteristic we look at is valuation, and in August, valuations played a big role in performance.

Below we’ve broken up the S&P 500 into deciles based on P/E ratios (trailing 12-month). Decile 1 contains the 50 stocks in the S&P with the lowest P/Es at the start of August, while decile 10 contains the 50 stocks in the index with the highest (or negative) P/Es. Each bar in the chart shows the average percentage change in August of the 50 stocks in each decile.

As shown, the 50 stocks in the S&P with the lowest P/E ratios at the start of the month fell an average of 11.5% in August! The next two deciles with the lowest P/E ratios fell more than 5% as well. On the other end of the spectrum, the 50 stocks with the highest P/E ratios fell only 0.78% in August.

You’ve certainly heard a lot about the “death of value investing” recently, and this is why! We have to think that at some point the scales will tip and head in the other direction. Start a two-week free trial to Bespoke Premium to see our full decile analysis report for August.

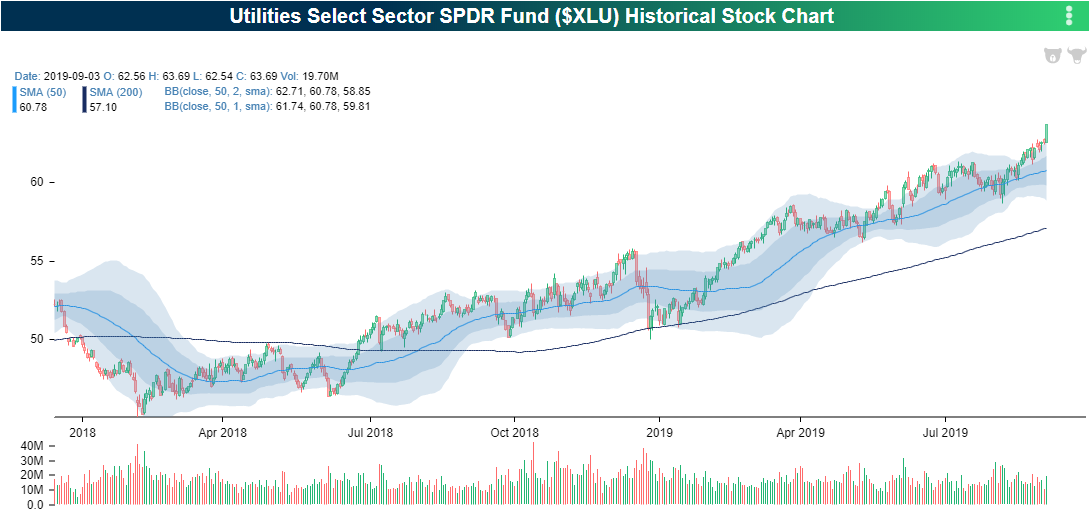

Utilities (XLU) Still On the Up And Up

As with other defensive sectors and safe assets, Utilities (XLU) has been on a tear all year with a 22.2% gain. The sector has been in a strong long term uptrend for some time now with the most recent leg higher bringing it to extremely overbought levels. XLU now sits over 3 standard deviations above its 50-DMA thanks to yesterday’s 1.77% rally. In the past year, there have only been four other days with larger single-day gains: June 5th, May 10th, and January 31st of this year, and October 24th of last year. Only the occurrence in June also coincided with XLU moving over 3 standard deviations above its 50-day in the surrounding days.

Since the Utilities Sector ETF first began trading in 1999, it has been rare to see XLU trade over 3 standard deviations above its 50-DMA. In fact, of all trading days that the ETF has been on the market, only 36 have seen XLU close at this extreme of overbought levels. Utilities do not stay this extended for long. The longest streak that where XLU has remained this overbought was 9 trading days in 2017; a majority of the time it only lasts for a single day.

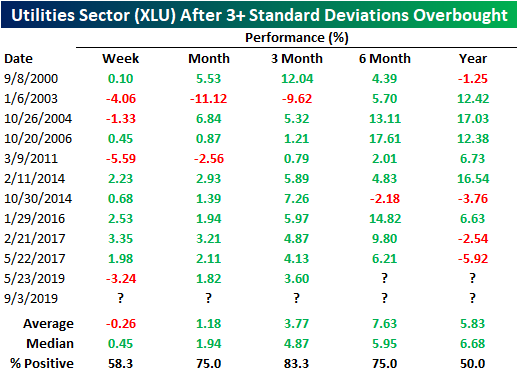

Although it can be reasoned that extremely overbought levels would lead to some degree of downside mean reversion, historically that has not necessarily been the case. As shown in the table below, performance following periods where the ETF closed over 3 standard deviations above its 50-DMA after having not done so for 80 days have actually generally held a positive bias. Only in the following week has XLU averaged a decline, but median performance is positive with a 45 bps gain. Returns are consistently positive one month, three months, and half a year later. For both three and six months out, there has only been one occurrence each that XLU was not higher. Six months later has been the strongest of these time periods, averaging a 7.63% gain. One year later, while still positive on average with multiple occurrences of double-digit returns, XLU has only been higher 60% of the time. Start a two-week free trial to Bespoke Institutional to access our interactive Security Analysis tool and much more.

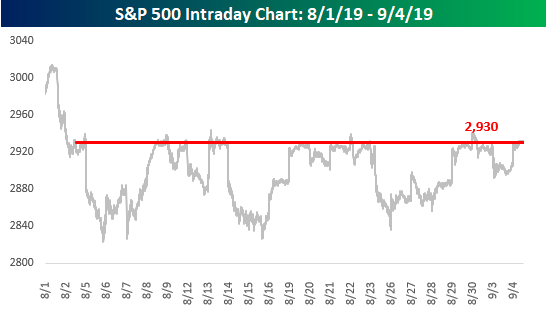

Make Up Your Mind Already

Talk about indecisive! After a moderate decline to kick off the week yesterday, US equities have more than erased those losses today. While a pretty big drop in the equity market followed by a big gain isn’t unheard of, when it goes on and on for more than a month, it’s enough to drive you nuts. Ever since early August, investors are being whipped around by a series of contradictory tweets, headlines, and “reports”. One day the trade war with China is at the point of no return. The next day the two sides are talking. It was only a couple of days ago that a peaceful solution to the protests in Hong Kong was almost out of the question. Today, everything is copacetic as CEO Carrie Lam withdrew the extradition bill that caused all the protests in the first place. On some days, Consumer Confidence, Retail Sales, Jobless Claims, etc suggest that a recession is out of the question, but then the next, reports like the ISM Manufacturing sector fall into negative territory.

Where does all the indecision leave us? Since the start of August, the S&P 500 has seen a series of eleven different rallies ranging between 1% and 4%. In between each of those rallies, though, we have seen ten different declines in the range of between 1% and 4% as well. With all the ups and downs, the S&P 500 finds itself trading at a level right around 2,930, which is a level it has crossed above and below on an intraday basis countless times over the last month, and for that matter the last year. We’ve already heard a number of stories about how companies are putting off big investment decisions until issues with trade and the economy start to sort themselves out, and based on the last month, the market has joined them. Start a two-week free trial to Bespoke Institutional to access our interactive market tools and all of our analysis.