Bespoke’s Morning Lineup – 5/29/26 – Nine For Nine

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In a crisis, be aware of the danger–but recognize the opportunity.” – John F. Kennedy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are modestly higher this morning following a mostly positive session in Asia, where South Korea rallied 3.6% to take its weekly gain to 8%. The Nikkei also rallied 2.5% for a weekly gain of nearly 5%. Asia’s positive moves have flowed through to Europe this morning, and the STOXX 600 is up 0.6%, led higher by Spain, Italy, and France.

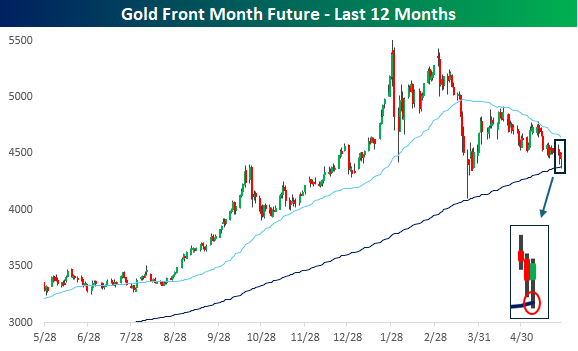

Outside of equities, treasury yields and crude oil are modestly lower on reports that the Iran-US ceasefire will be extended, and gold is bouncing after briefly trading below its 200-DMA yesterday.

An AI compute deal between Anthropic, Alphabet (GOOGL), Broadcom (AVGO), Apollo (APO), and Blackstone (BX) was reported on by Bloomberg last night. The deal has a lot of moving parts to it, and raises concerns over complex transactions and whether it’s just a lot of smoke and mirrors. We broke it all down in the commentary section of today’s Morning Lineup and explained why it’s nothing like the transactions that took place leading up to the Financial Crisis, so make sure to check that out.

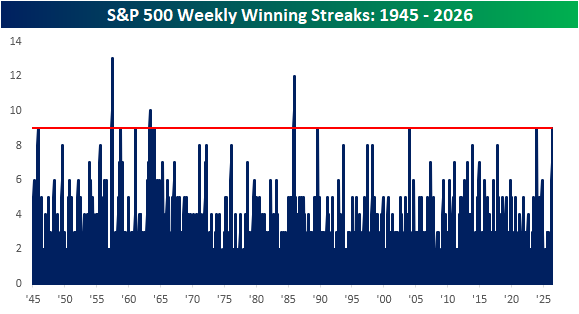

In our experience, we’ve seen enough to know never count anything out, but with the S&P 500 up over 1% already this week, it’s looking likely that the S&P 500 will finish higher this week, extending its weekly streak of gains to nine. The last time the S&P 500 traded higher for nine straight weeks was in December 2023, and the last time there was a longer streak of weekly gains was way back in 1985!

The chart below shows S&P 500 winning streaks in the post-WWII period, and while there have been eleven other nine-week streaks, only four made it to a tenth week or longer. In 1985, the S&P 500 went 12 straight weeks without a decline, and in 1957, the index went 13 weeks, or 3 months, without a weekly decline.

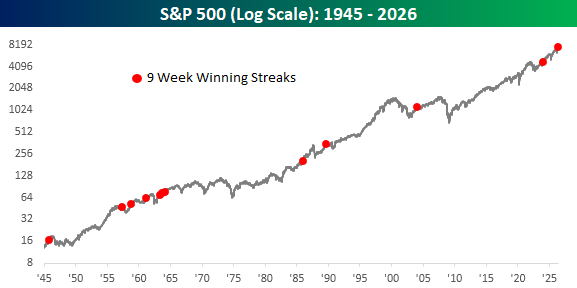

The chart below shows each prior streak on a long-term chart of the S&P 500. Besides the fact that none of these prior periods occurred right near a major top in the market, it’s also interesting to note that they didn’t really occur early on in bull markets coming out of extended bears.

While the S&P 500 keeps chugging along, gold prices have been under pressure for months now, which is a stark contrast to earlier this year when the metal could do no wrong. From the peak in late January, gold prices briefly dropped into bear market territory (on an intraday basis) before rallying intraday. In the process of that decline, gold prices also briefly dipped below the 200-day moving average (DMA) for the first time in 2.5 years.

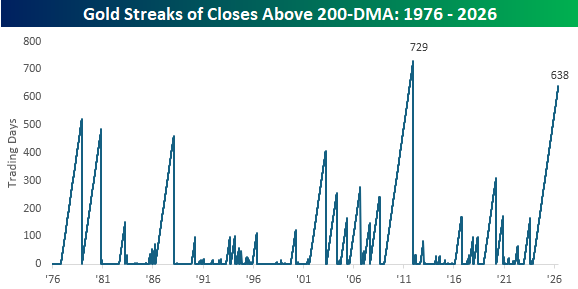

While the streak of trading without a breach of the 200-DMA on an intraday basis ended yesterday, the streak of closes above that level remains intact, and at 638 trading days, it ranks as the second-longest streak on record, trailing only a 729 trading day streak that ended in December 2011. In order for the current streak to break the record, gold would have to stay above its 200-DMA through the summer months and into late October, but it has been an impressive streak.

The decline in gold since its January high, however, should serve as an important reminder that the tide on a trade that can seemingly do no wrong can quickly go out.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.

Q1 2026 Earnings Conference Call Recaps: Dollar Tree (DLTR)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Dollar Tree (DLTR) Q1 2026 earnings call.

![]()

Dollar Tree (DLTR) operates roughly 9,400 discount stores selling everyday essentials, seasonal goods, and discretionary items at low price points, with 85% of its assortment priced at $2 or below. Comps came in at 3.5%, ahead of expectations, and adjusted EPS grew 38% year-over-year to $1.74. The standout story was shrink, which improved for the first time in years thanks to store standards programs. The share of stores operating below internal standards dropped from 42% to under a third in roughly a year. Tariffs were a headwind but were fully offset by operational improvements, and notably, zero tariff refunds were included in the results. The company raised full-year EPS guidance to $6.70 to $7.10, though management was deliberately conservative, absorbing higher fuel costs tied to the Middle East conflict as a full-year headwind rather than flowing Q1 upside through. Traffic is still slightly negative but improving, and management expects it to turn positive in the back half as easier comparisons kick in. DLTR gained 18% on 5/28 after beating EPS and revenue expectations…

Continue reading our Conference Call Recap for DLTR by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q1 2026 Earnings Conference Call Recaps: Kohl’s (KSS)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Kohl’s (KSS) Q1 2026 earnings call.

![]()

Kohl’s (KSS) is a mid-tier department store chain with roughly 1,100 locations serving low-to-middle income shoppers across the US. It sells apparel, footwear, home goods, and beauty through its own private labels and national brands, with Sephora shop-in-shops as a key traffic driver. This was the best quarterly comp in four years, down just 1.1%, and management is cautiously optimistic. The clearest win was private label brands, up 6%, driven by juniors’ clothing brand “So” and activewear brand “Flex,” both resonating strongly with value-seeking customers. The Kohl’s card customer, historically the most loyal and productive cohort, went from down mid-single digits in Q4 to flat in Q1, a 600 basis point swing that suggests the turnaround is gaining real traction. Sephora was the one notable disappointment, running down low single digits with weakness in makeup and skincare, though MAC, a cosmetics brand, is rolling out to all stores later this year. Store traffic is still declining, and getting customers back more frequently remains the central challenge. Kohls’s rallied 20% on 5/28 after beating both EPS and revenue expectations…

Continue reading our Conference Call Recap for KSS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q1 2026 Earnings Conference Call Recaps: Salesforce (CRM)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Salesforce’s (CRM) Q1 2027 earnings call.

![]()

Salesforce (CRM) is the world’s largest customer relationship management software company, providing cloud-based tools for sales, customer service, marketing, data analytics, commerce, and workplace collaboration through Slack. Salesforce now processes 28.6 trillion AI tokens quarterly and said Agentforce ARR surpassed $1 billion, highlighting how quickly large enterprises are experimenting with autonomous AI tools. This quarter’s earnings call focused almost entirely on AI monetization and Salesforce’s push to become the “operating system” for enterprise agents. Management repeatedly emphasized that customers are moving beyond pilots into production deployments, with companies like PenFed and UCLA Health using AI agents to reduce call center workloads, automate patient inquiries, and consolidate sprawling software systems. Slack was another major focus, with management calling it the central workspace for both humans and AI agents as Slack AI usage surged 350% quarter-over-quarter. Salesforce also introduced “Headless 360,” allowing AI tools like Claude and ChatGPT to access Salesforce data directly through MCP APIs. After posting better-than-expected EPS and revenue, CRM shares fell 0.75% on 5/28…

Continue reading our Conference Call Recap for CRM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q1 2026 Earnings Conference Call Recaps: Best Buy (BBY)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Best Buy (BBY) Q1 2027 earnings call.

![]()

Best Buy (BBY) is the largest consumer electronics retailer in the US, selling everything from laptops and TVs to appliances and gaming gear. Comps came in at 2%, ahead of the 1% guide, with broad-based strength across gaming, computing, and mobile. The consumer picture remains consistent: value-focused but still willing to spend, with no signs of trade-down. The biggest news was a one-year national exclusive on RGB TVs, the first major new display technology since OLED in 2013, arriving just as the 49 million TVs sold during 2020 enter their replacement window. On the cost side, rising DRAM prices are pushing up PC prices industry-wide, but Best Buy is pulling inventory forward to lock in lower costs and betting its broad assortment will keep customers shopping within their budgets. Best Buy Ads is approaching $1 billion in annual revenue, and Marketplace hit $250 million GMV in the quarter alone. CEO Corie Barry also announced she is stepping down in November, with incoming CEO Jason Bonfig taking over. Best Buy’s share price is up nearly 18% after EPS and revenue beat expectations…

Continue reading our Conference Call Recap for BBY by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

The Closer – AI Bull Back on Top, GDP, PCE – 5/28/26

Log-in here if you’re a member with access to the Closer.

- Even after working off of its lows, the S&P 500 Software and Services industry’s distance from its price targets is in the 10th percentile of all periods since 2003.

- GDP was revised down 0.4%-pt QoQ SAAR as non-residential investment remained the biggest driver of growth.

- Due to a combination of weak hiring, slowing wage growth, and higher inflation, purchasing power has been driven down as real household earnings registered a 4th percentile reading.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

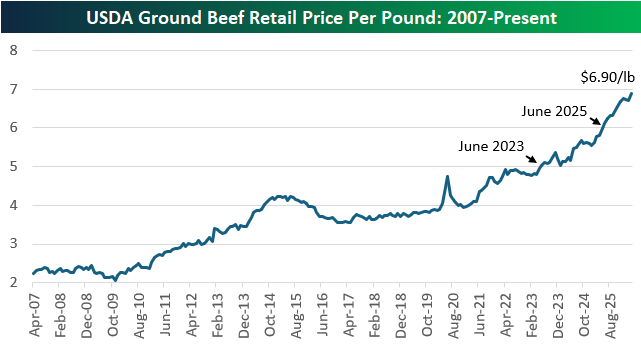

Beef Up, Eggs Down

After first surging past $5/lb in June 2023, then $6/lb in June 2025, the retail price for USDA Ground Beef jumped 20 cents to $6.90/lb in April and is on pace to hit $7 this summer.

Beef prices have jumped $1.10/lb (18.9%) over the last year and have doubled since the end of 2013.

As we highlighted a couple months ago, the backyard burger is becoming a delicacy! Make sure to enjoy each and every savory bite this summer.

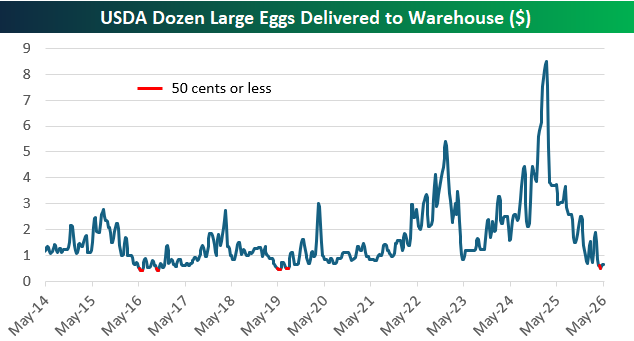

At the same time that ground beef approaches $7/lb, they’re practically giving away eggs. Just over a year ago in early 2025, the wholesale price of a dozen large eggs topped $8. Earlier this month, that same dozen eggs got down to just $0.50!

Since 2014 when weekly USDA data begins, a dozen eggs have only dipped to 50 cents or less two other times: mid-2019 and mid-2016.

While a burger for lunch or dinner is killing consumer pocket books, at least breakfast is getting cheaper.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

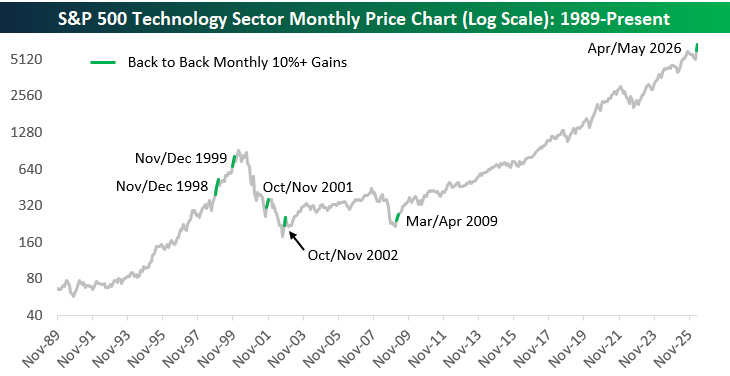

Tech Looking for Back to Back 10%+ Monthly Gains

The S&P 500 Technology sector gained more than 17% in April, and with one trading day left in May, it’s currently up 12%.

The last time the Tech sector saw back-to-back 10%+ monthly gains was in March and April 2009 coming out of the Financial Crisis bear market.

Before 2009, the sector only had back-to-back 10%+ monthly gains four other times: Nov/Dec 1998, Nov/Dec 1999, Oct/Nov 2001, and Oct/Nov 2002.

Below is a look at where these huge two-month moves happened on a price chart for the sector going back to 1989:

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.

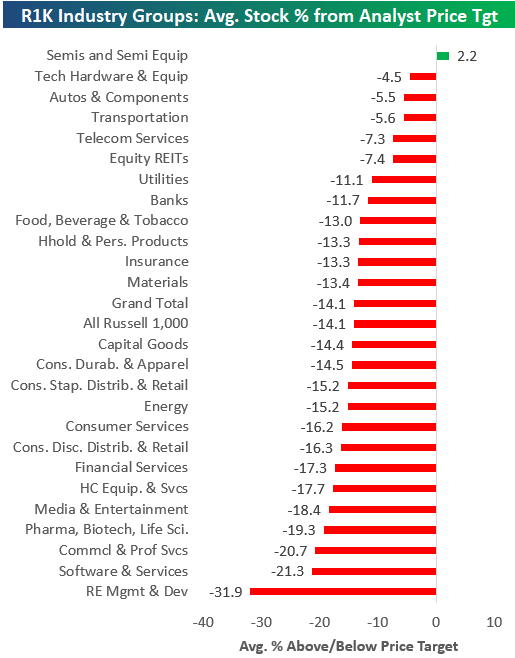

Semis Race Past Analysts

The average stock in the Russell 1,000 trades about 15% below its consensus analyst price target, but the semis have rallied so far so fast that the group has raced past Wall Street expectations.

As shown below, the average stock in the Semiconductor group is currently 2.2% above its average analyst price target.

You don’t usually see many individual stocks move above their average analyst price target, so for an entire group to do it is practically unheard of.

When this happens, either the analysts are forced to up their price targets even more (which typically causes more buyer enthusiasm), or share prices eventually pull back from overbought levels.

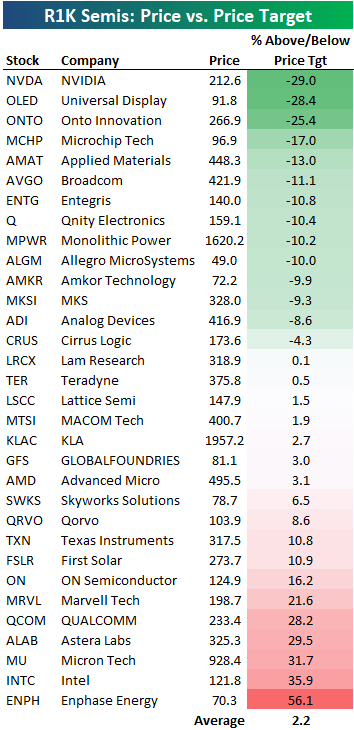

Below is a look at the Russell 1,000 semis stocks and where they’re trading relative to consensus analyst price targets. Enphase Energy (ENPH) came into today more than 50% above its price target, while Intel (INTC) and Micron (MU) are more than 30% above.

Notably, the largest semi of them all — NVIDIA (NVDA) — is 29% below its price target, the farthest away in the entire group and more than double the distance that the average Russell 1,000 stock is trading from its price target.

Want more from Bespoke? You can start by joining our Think BIG mailing list where you’ll receive an interesting market stat in your inbox a few times per week. All we need is your email address. Join now by clicking here or on the image below.