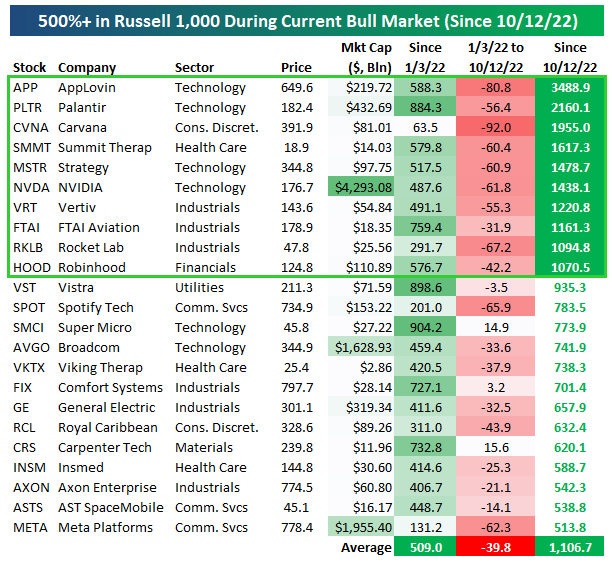

Ten Bull Market 10-Baggers

Since 10/12/22 – a little over a month before the launch of ChatGPT on 11/30/22 – US stocks have been in what we call the “AI Boom” bull market. While broad market performance has been robust, one striking aspect of this cycle has been the extraordinary gains in a handful of individual equities. Ten stocks in the large-cap Russell 1,000 have now advanced more than 1,000% since the start of this period. These “10-baggers” reflect a mix of AI-driven demand, structural turnarounds, and thematic speculation. Below we take a look at each of these names to provide insight into the breadth of forces powering this bull market beyond the headline indices.

Bull Market 10-Baggers:

AppLovin (APP): AppLovin provides a mobile app monetization and ad-tech platform. The company has benefited from stronger demand for performance-based advertising and the application of AI tools to improve targeting and user engagement. As digital advertising rebounded, investors rewarded APP’s ability to scale profits in an AI-enhanced ecosystem.

Palantir (PLTR): Palantir develops advanced data analytics platforms serving governments and enterprises. Investor enthusiasm has accelerated as the company positioned itself as a key player in applied AI and national security technology. Commercial adoption of its Foundry platform and new AI pilots with large enterprises have reinforced growth expectations.

Carvana (CVNA): Carvana operates an online platform for used-car sales. While not directly tied to AI, its turnaround has been among the most notable of the cycle. Balance sheet repair, improved unit economics, and a favorable used-car pricing environment drove a re-rating, amplified by high short interest and renewed investor risk appetite.

Summit Therapeutics (SMMT): Summit Therapeutics is a clinical-stage biotechnology firm. Its dramatic share price increase followed the licensing of an oncology candidate with substantial market potential. Investor interest in high-upside biotech, coupled with a supportive capital-raising environment during the bull market, propelled the stock to outsized gains.

MicroStrategy (MSTR): MicroStrategy, while a software company by origin, has effectively become a proxy for Bitcoin exposure due to its significant cryptocurrency holdings. The resurgence in digital assets, particularly following the approval of spot Bitcoin ETFs, has driven MSTR’s equity performance well beyond the market average.

NVIDIA (NVDA): NVIDIA is the market leader in GPU semiconductors and has emerged as the clear beneficiary of the generative AI buildout. Surging demand for AI infrastructure, expanding gross margins, and a growing software ecosystem have supported the company’s transformation into one of the world’s most valuable enterprises.

Vertiv (VRT): Vertiv supplies power and thermal management systems for data centers. As hyperscale cloud providers and enterprises expand AI capacity, demand for data center infrastructure has accelerated sharply. VRT has been viewed as a critical “picks and shovels” supplier to the AI cycle, driving its substantial re-rating.

FTAI Aviation (FTAI): FTAI Aviation specializes in leasing and servicing jet engines, particularly the widely used CFM56. Strong air travel recovery, tight supply of engine parts, and lucrative maintenance economics have supported earnings growth. Structural demand for fleet reliability has reinforced investor confidence in the company’s business model.

Rocket Lab (RKLB): Rocket Lab operates as a space launch and satellite systems provider. Investor enthusiasm has centered on its role as a disruptive competitor in small-satellite launches, supported by increasing defense and commercial contracts. While profitability remains distant, the strategic importance of low-Earth orbit systems has underpinned the stock’s advance.

Robinhood (HOOD): Robinhood operates a digital brokerage platform offering commission-free trading. Increased retail participation, higher interest income on customer balances, and growth in crypto trading have supported its rebound. The return of risk appetite during the AI Boom has allowed HOOD to re-emerge as a favored retail engagement vehicle.

The ten stocks that have delivered gains in excess of 1,000% since the onset of the AI Boom highlight the breadth of leadership within this cycle. Some represent clear beneficiaries of AI infrastructure investment (NVIDIA, Vertiv), others reflect speculative enthusiasm in turnaround or emerging growth stories (Carvana, Rocket Lab), and a few embody broader macro themes such as digital assets or retail trading (MicroStrategy, Robinhood). Taken together, they illustrate the defining characteristic of the current bull market: investors are rewarding both transformational innovation and asymmetric recovery opportunities at an extraordinary scale.

While the gains in these ten stocks are remarkable, investors should recognize the speculative nature of such moves. Equities that advance 1,000%+ in less than three years rarely sustain that pace, and history shows that many such names ultimately experience sharp drawdowns. Valuations have expanded dramatically, and future performance will require fundamental follow-through that may not match current expectations. In other words, while these companies illustrate the extremes of the AI Boom bull market, they also highlight the risks of extrapolating past returns too far into the future.

Q3 2025 Earnings Conference Call Recaps: Lennar (LEN)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Lennar’s (LEN) Q3 2025 earnings call.

![]()

Lennar (LEN) is one of the largest homebuilders in the US, constructing and selling single-family homes, townhomes, and multifamily residences across major markets. Lennar serves a broad base of first-time, move-up, and active adult buyers, making it a bellwether for US housing demand. Because housing is deeply tied to rates, confidence, and supply constraints, Lennar’s results often offer insight into the broader housing market and consumer sentiment. In Q3, Lennar delivered roughly 21,500 homes and sold about 23,000, but saw gross margin fall to 17.5% as incentives rose to 14.3% to offset affordability pressures. Management signaled a deliberate pullback in deliveries (Q4 guide: 22,000–23,000) to protect margins while awaiting a demand rebound if mortgage rates hold near 6%. Construction costs fell about 3% YoY, cycle times hit a record low of 126 days, and warranty costs dropped 35%. The company highlighted its asset-light land model (98% controlled lots) and investments in digital sales funnels, dynamic pricing, and AI partnerships like Opendoor to prepare for the next housing upcycle. LEN beat its EPS estimate but came in weaker on sales on a 6.4% YoY decline, and the stock fell 4.2% on 9/19 as a result…

Continue reading our Conference Call Recap for LEN by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 9/22/25 – More Defensive

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A man who is certain he is right is almost sure to be wrong.” – Michael Faraday

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The S&P 500 closed at its 27th record high of the year on Friday as investors continued to bask in the light of the Fed’s rate cut on Wednesday. The 28th record high of the year will likely have to wait at least another day, though, as futures on all three major averages are indicated to open down by a little more than 0.30%. Small caps, which also hit a record high last week after a long drought, are also lower but not by as much (0.23%) as the S&P 500.

Asian stocks were mixed overnight, with the Nikkei rallying 1% to another record high, while Hong Kong was down close to 1% and China was marginally higher. While Japanese stocks keep hitting record highs, JGBs keep falling as the 10-year yield hit the highest level since 2007.

In Europe, the tone is more one-directional with the STOXX 600 down 0.2% while Germany leads the way lower with a decline of 0.7%. There’s no economic data in the region this morning, but auto stocks are weaker with both Volkswagen and Porsche trading lower after lowering guidance.

As we noted in last week’s Bespoke Report, we’re in a data lull. While multiple FOMC members will speak today, last week’s cut is behind us, and earnings season doesn’t kick off for another two weeks. Newton’s first law of motion says that an object in motion tends to stay in motion unless acted upon by force, so that would suggest more gains ahead. However, it is late September, which is historically a weak time of year, and investors have seen some large gains over the last five months, so you can’t fault anyone for wanting to take some profits.

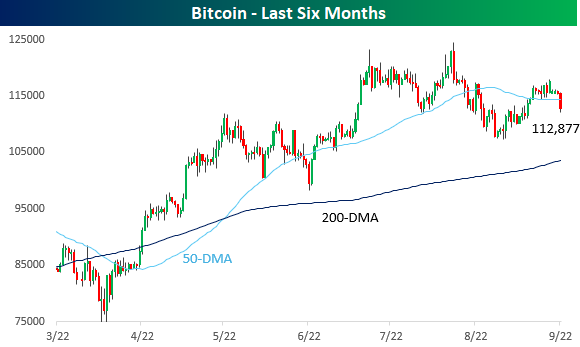

Crypto will be one place to watch for a measure of risk appetite in the market, and this morning’s action is showing a more defensive posture. Bitcoin is trading down over 2% this morning as it has broken below $113,000 and below its 50-day moving average (DMA). With today’s decline, Bitcoin is essentially trading right where it was back in May.

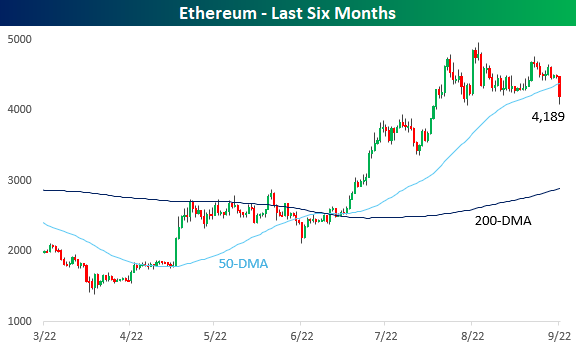

Unlike Bitcoin, which has been moving sideways, Ethereum prices had a much steeper run-up over the Summer, even as it has traded in a sideways range for the last month. This morning’s weakness in Ether has been more magnified with a decline of over 6%, and it too is below its 50-DMA for the first time in months.

Brunch Reads – 9/21/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Benedict’s Betrayal: On the morning of September 21, 1780, Benedict Arnold’s long-simmering betrayal of the American Revolution came to a head. By then, Arnold was already a celebrated war hero turned embittered officer, furious at what he saw as a lack of recognition and plagued by financial troubles. Stationed at West Point, a critical American fortress on the Hudson River, he had secretly arranged to hand it over to the British in exchange for money and a commission in the British Army. His contact was Major John André, a British officer operating under disguise.

That day, André and Arnold met near the Hudson, where Arnold passed along detailed plans of West Point’s defenses. The scheme began to unravel almost immediately. On André’s return south, he was stopped by American militiamen, who searched him and uncovered the incriminating papers. Taken into custody, André’s fate was sealed, but Arnold, tipped off at the last moment, fled downriver to a waiting British ship, narrowly escaping capture.

News of the treason spread like wildfire. George Washington, who had trusted Arnold deeply, arrived at West Point only hours after the plot was exposed and was shaken to find how close the Revolution had come to disaster. André was later hanged as a spy, while Arnold lived on in exile, forever branded in America as the name synonymous with betrayal.

AI & Technology

ChatGPT Is Blowing Up Marriages as Spouses Use AI to Attack Their Partners (Futurism)

When it comes to relationships, ChatGPT is turning into a constant third voice in the room, siding with one partner’s prompts and helping push fights toward breakups. A Stanford addiction doctor says the bot rewards validation, not reflection, creating a feedback loop that fuels one-sided narratives, derails therapy, and in some cases coincides with domestic blowups and spirals that families link to “AI psychosis.” OpenAI claims it’s adding safeguards and crisis routing, yet the stories reveal how lengthy, intimate chats can overwhelm guardrails and leave people feeling outnumbered by a machine that behaves more like a digital intoxicant than a therapist. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

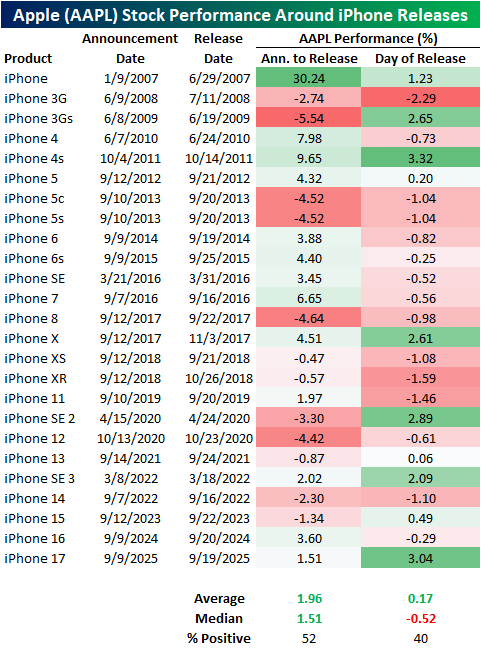

Investors Buying Apple (AAPL) as Consumers Buy the iPhone

In last Monday’s Chart of the Day we discussed the performance of Apple (AAPL) surrounding the release of their staple product: the iPhone. While the newest version of the phone, the iPhone 17, was announced officially in a reveal back on September 9th, it finally hit the shelves today.

As shown below, AAPL rallied 1.5% from the close of the day of the announcement through yesterday’s close. That is right in line with the median performance for that period for prior iPhone releases.

As for today where consumers are actually able to get the phones in their hands, AAPL is rallying an impressive 3% on the session. As shown below, median performance on those days has actually been negative on a median basis historically.

We will eventually learn how successful the launch was in terms of sales, but as for the stock price reaction on iPhone release dates, today is the second strongest response by AAPL behind the 3.32% gain in 2011 when the iPhone 4s launched.

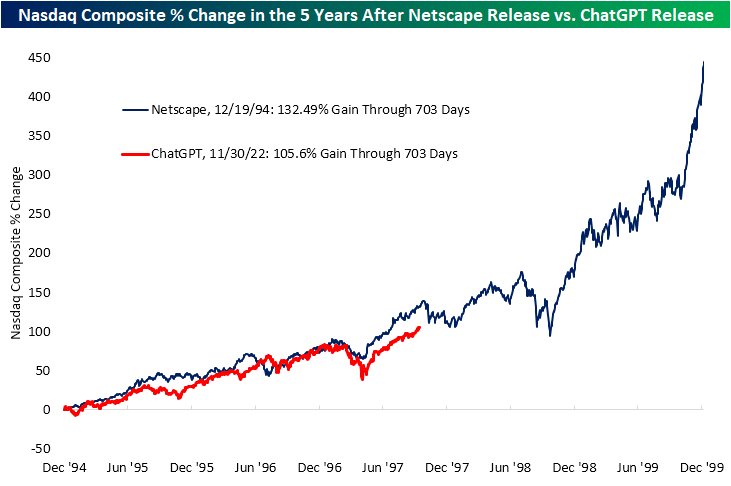

ChatGPT and Netscape Keep Track

If history does not repeat itself, it can at least rhyme. One good example of this has been the performance of the Tech-heavy Nasdaq since the AI era began in earnest with the release of ChatGPT in November 2022. In our chart below that we first published in early 2024, we show the move in the Nasdaq Composite since ChatGPT’s release and compare that to the move in the index following the release of the first modern web browser, NetScape, in December 1994.

As the chart shows, the moves in the Nasdaq following the release of ChatGPT and Netscape have been eerily similar. Putting a number to it, the two lines have an astoundingly high correlation coefficient of 0.95. For a refresher from your 101 statistics class, a coefficient of 1 would indicate the two lines move identically; so for real world statistics, this is about as close as it gets!

In terms of absolute performance, the rally in the Nasdaq has been slightly weaker this go around than it was in the 1990s. Since the release of ChatGPT, the Nasdaq has risen 105%, which compares to a 132.5% gain for the index from December 19, 1994 up through the next 703 trading days (through 9/29/1997). The index doubling in a little more than a two and a half year span is impressive in its own right. With that said, if these two lines were to continue to track one another down the road, history would suggest that there is still plenty of steam left in the rally.

Q3 2025 Earnings Conference Call Recaps: FedEx (FDX)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers FedEx’s (FDX) Q1 2026 earnings call.

![]()

FedEx (FDX) is a global logistics company spanning express air, ground parcel, and LTL freight, plus digital supply-chain platforms (Dataworks, fdx, Surround). It serves SMBs, large enterprises, and healthcare, moving about 17 million packages per day and generating roughly 2 petabytes of data and 100 billion transactions that offer a real-time read on trade flows and consumer demand. In the first quarter of fiscal 2026, management balanced a resilient US parcel market with mounting global trade frictions tied to the removal of de minimis exemptions: consolidated revenue grew 3% YoY while Federal Express Corporation revenue rose 4%. FedEx reduced trans-Pacific Asia outbound capacity by roughly 25% and shifted lift to Asia–Europe, helping International Priority and Economy Freight revenue grow 14%, and it deepened domestic share with small business and healthcare wins, including Best Buy as primary national parcel carrier and Amazon onboarding targeted for completion by the third quarter. Network 2.0 has optimized about 360 stations with roughly 18% of US volume on the model. FDX shares were up as much as 7.4% after hours on 9/18 in reaction to better-than-expected results…

Continue reading our Conference Call Recap for FDX by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke Stock Profile: Credo Technology (CRDO)

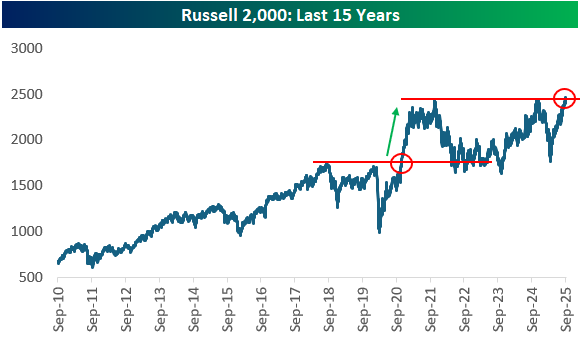

Small-Caps Finally Make New High

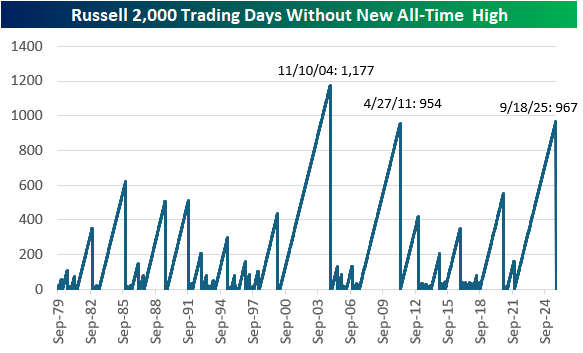

Yesterday, the small-cap Russell 2,000 finally managed to close at a new all-time high when it broke above prior peaks made in December 2024 and December 2021. The last time the index had a breakout after a long period without one was in late 2020 following the COVID Crash. Back then, the index made a huge leg higher after the breakout. Small-cap bulls would love to see a repeat.

Yesterday also marked the end of a 967-trading day streak without a new all-time high for the Russell 2,000. It was the second-longest streak without a new all-time high in the index’s history behind the 1,177 day streak that ended in November 2004. The only other comparable streak was the 954 trading days it went without a new high that ended on April 27th, 2011.

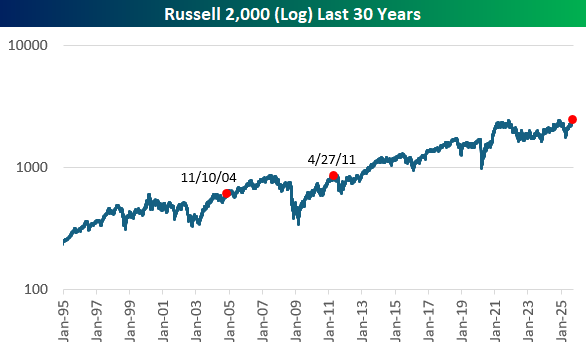

Below is a log chart of the Russell with red dots marking the end of the two prior long streaks without new all-time highs mentioned above. Following the 2004 streak, the index continued to chug along higher, but the index saw a pretty nasty sell-off in the months following the end of the 2011 streak.

Bespoke Morning Lineup – 9/19/25

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Language fits over experience like a straight-jacket.” – William Golding

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

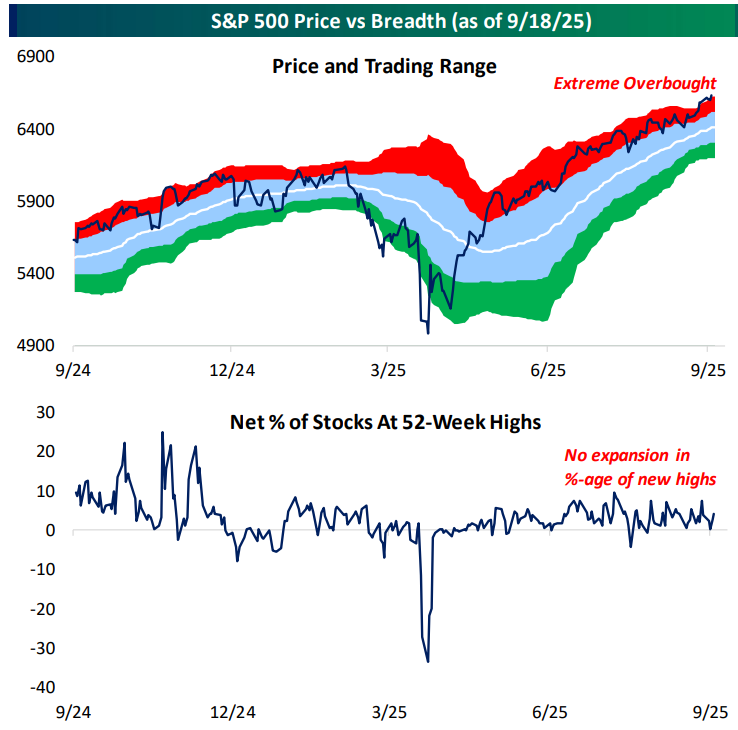

It’s important to continue to note that the S&P is trading in extreme overbought territory, but there hasn’t been a similar move with underlying breadth. Yet another breadth indicator that remains totally neutral is the percentage of stocks in the S&P trading at new 52-week highs.