Qualcomm (QCOM) All-Time Highs

If the first trade you made in 2000 was to buy Qualcomm, congratulations! It’s finally profitable. Learn more about Bespoke Premium.

Bespoke’s Consumer Pulse Report — August 2020

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

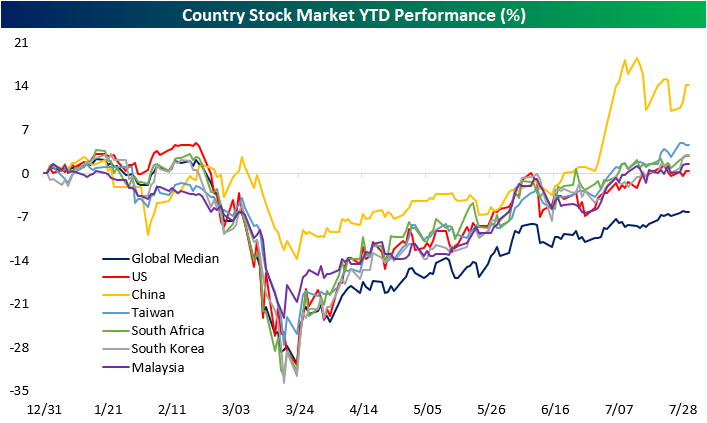

China Running Away YTD

Every Wednesday, we publish our Global Macro Dashboard which provides a high-level summary of market and economic data of some of the world’s largest economies. Of the 23 stock markets tracked, just six including the US are positive year to date at the moment (in local currency). In the chart below we show the YTD performance of these six countries as well as the global median in 2020. As shown, even though it was actually the first to tip into the green YTD following the global sell-off in February and March very briefly back in early June, the US is up the least of this group with a YTD gain of 0.4%. China’s stock market is up the most at +14%. Taiwan, South Korea, South Africa, and Malaysia are also outperforming the US but are up more modestly than China with the best of these, Taiwan, gaining 4.53% this year. Meanwhile, the median country in our Global Macro Dashboard remains down 6.2% YTD.

Given it is up the most on a year to date basis, China has also gained the largest share of global equity market cap in 2020. As shown in the table below, China has gained 1.7 percentage points of global market cap in 2020 and now takes up 10.14%. China now joins the US as the only other country with a double-digit share of total world market cap. Despite this, China has actually lost share since the bear market lows on 3/23. Meanwhile, the US, Germany, Canada, India, South Korea, and Australia have all gained a significant share since 3/23. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: FOMC Days Intraday Performance

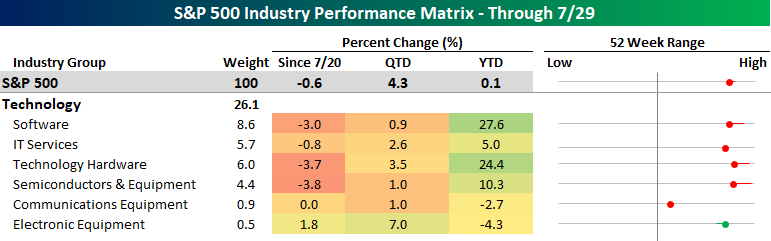

Tech Takes a Back Seat

For a little over a week now since it last made a new high on 7/20, the Nasdaq Composite has been churning around and consolidating its gains as investors await today’s testimony ahead of Congress from Alphabet (GOOGL), Amazon (AMZN), Apple (AAPL), and Facebook (FB) and then earnings reports from all four companies after the close on Thursday. Needless to say, the next two days will go a long way in defining the backdrop for the Technology sector through the rest of the summer.

Since the Nasdaq’s high on 7/20, only one of the Technology sector’s six industries has posted positive returns, and it’s also the smallest industry in the sector. While the Electronic Equipment industry has gained 1.8% since 7/20, larger industries like Semis, Tech Hardware, and Software are all down over 3%. While these industries have pulled back a bit over the last week or so, QTD they’re all still in the black, and on a YTD basis, they still remain among the market’s top performers with double-digit percentage gains for all three. On the right side of the image below, we show where each industry is trading relative to its 52-week range, while the tail indicates the change since 7/20. At the Nasdaq’s peak on 7/20, all three industries mentioned above were either at or right near record highs as investors sought growth in a growth starved market.

While Tech has taken a backseat role in recent days, Industrials has been picking up some of the slack. Although the sector has a lot more industries than the Technology sector, it has a much smaller market cap accounting for just 7.9% of the S&P 500 versus Technology’s 26.1% share. Of the twelve industries in the sector, ten are up since the Nasdaq’s peak on 7/20. Leading the way higher, Air Freight, Machinery, Commercial Services, and Building Products have all gained more than 3.5% To the downside, only Airlines and Industrial Conglomerates are in the red since 7/20.

What’s interesting to note about the Industrial sector’s recent performance is that despite the Covid-induced recession, the majority of industries in this sector are much closer to 52-week highs than 52-week lows. The stock market is typically forward-looking, so the recent strength in these cyclical industries suggests that either the market is uncharacteristically clueless or it sees better economic times ahead. Click here to view Bespoke’s premium membership options for our best research available.

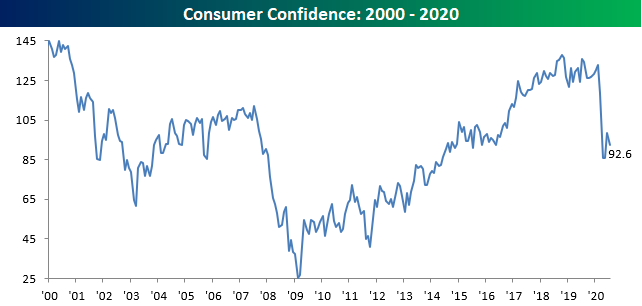

Consumer Confidence Experiences a Setback

As Covid case counts were rising in the South and Southwest earlier this month, Consumer Confidence took a hit in July as the Conference Board’s Index of Consumer Confidence dropped from 98.3 down to 92.6, which was below the consensus forecast of 95.0. While many economic indicators have seen significant bouncebacks in recent weeks, Consumer Confidence hasn’t been one of them. However, if the recent declines in case counts among many of the problem states continue to recede that could provide a boost to sentiment in August.

Underneath the surface, this month’s report was mixed. While the Expectations component dipped along with the headline inline, the reading on current conditions saw a modest increase.

Due to the diverging paths of the Expectations and Present Situations indices, the spread between the two actually moved back into positive territory. This is notable in that normally once the spread turns meaningfully negative, it takes months for it to bounce back to positive levels.

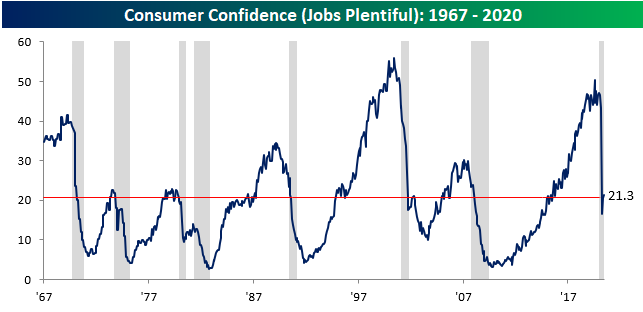

The last item we wanted to highlight is the index of Jobs Plentiful. In July this reading bounced to 21.3 from 20.5. Two things to note with this index concern the recent low reading and the current level. Regarding the recent trough of 16.5, if that low holds, it would be the highest trough for the indicator during and coming out of a recession since the mid-1960s. In terms of the current level, we would note that back in the early 2000s we saw a similar bounce before the index started to roll over again. Based on July’s pullback in the overall headline reading, a rollover in this index next month (like the one in 2002) wouldn’t be a welcome development. Click here to view Bespoke’s premium membership options for our best research available.

Richmond on the Rise

The final regional Fed manufacturing index of the month came out today from the Richmond Fed. The headline index continued to improve rising 10 points in July indicating the first expansion in the region since March and the highest reading for the index since January.

Along with the headline index, just about every sub-index posted expansionary readings. Shipments, Capacity Utilization, and Availability of Skills are in the upper decile of historical readings. When it comes to the indices for future expectations. even more categories are around some of their highest readings on record. For example, the indices for future conditions for Shipments, New Orders, Order Backlogs, Capacity Utilization, Vendor Lead Times, Local Business Conditions, and Number of Employees are all in the 90th percentile or better.

The only areas that remain on the weak side for both present and future conditions are for expenditures. For current conditions, Capital Expenditures, Equipment & Software Expenditures, and Services Expenditure are all at the low end of historical readings with little improvement in July. Additionally, a greater share of companies continue to report decreases than increases in their workforce as the index for the Number of Employees remained below zero for a fifth consecutive month. Altogether, this points to a generally improved backdrop for mid-Atlantic manufacturing businesses, though they remain hesitant to invest back into and expand their businesses.

Even though the manufacturing sector has staged a massive turnaround, the same cannot be said for the services sector. Service sector businesses did report Local Business Conditions improved in July, but Demand, Revenues, Expenditures, and employment all remain in contraction. Expectations are more optimistic, but there were some large declines this month, namely in the expectations indices for Revenues, Demands, and Local Business Conditions. Click here to view Bespoke’s premium membership options for our best research available.

Chart of the Day: Early Earnings Results Strong

Recreational Vehicles, Outdoors, and More

Throughout the pandemic, we have frequently highlighted how Google searches for things like boats, camping, gardening, and many other outdoor activities have been sharply on the rise. Consumer shifts towards outdoor recreational activities from sea to shore have been the benefit of many names. Below we show just over two dozen stocks that are in some form related to things like recreational vehicles, camping, sporting goods retailing, boating, golf, gardening, and the likes. As shown, while they had fallen by nearly 50% during the bear market, off the lows they have surged. 21 of these names have risen by at least 100% and their average gain since 3/23 is more than 200%. We find it fascinating how much these stocks got “thrown out with the bathwater” in the initial stages of the pandemic. With an average decline of 48% during the 2/19-3/23 bear market, investors certainly were not thinking about a big shift towards socially-distanced outdoor activities at the time.

Given the runs they’ve had, they’re generally very elevated. On average, these stocks are 23.81% above their 50-DMAs and 52.9% above their 200-DMAs. Granted, there is a sizeable range in regards to distance from the moving averages. For example, Winnebago (WGO) is less than 1% from its 50-DMA while Big 5 Sporting Goods (BGFV) is over 90% above its 50-DMA. The same goes for the 200-DMA Camping World (CWH), which we highlighted in a post yesterday, is almost 150% above its 200-DMA while Columbia Sportswear (COLM) is actually under its 200-DMA; the only of these stocks that this applies to.

Given the elevated price levels and massive runs, short interest has built up for several of these names. Hibbett Sports (HIBB) is the worst of these with 34.57% of float sort. Camping World (CWH), OneWater Marine (ONEW), and Dick’s Sporting Goods (DKS) also all have readings above 20%. By comparison, the average stock in the S&P 1500 has 6% of float short.

Below, we show all of the charts of these names over the past year and five years. The huge rallies over the past few months are glaring, especially since many of these stocks have been in long term downtrends headed into the COVID pandemic. The strong returns over the past few months have obliterated those downtrends. For others like TSCO, YETI, PII, and MBUU, the longer-term trends have been stronger with uptrends or breakouts of some sideways price action. In the case of PII, an earnings triple play today resulted in the breakout to the upside to a 52-week high. We have created a custom portfolio of all these names to keep track of them in the Trend Analyzer and Chart Scanner tools.

Bespoke CNBC Appearance (7/27)

Bespoke co-founder Paul Hickey appeared on CNBC’s Closing Bell yesterday to discuss the current state of the markets and company performance based on international exposure. To view the segment, click on the link or image below. Click here to view Bespoke’s premium membership options for our best research available.

Company Performance Based on International Exposure