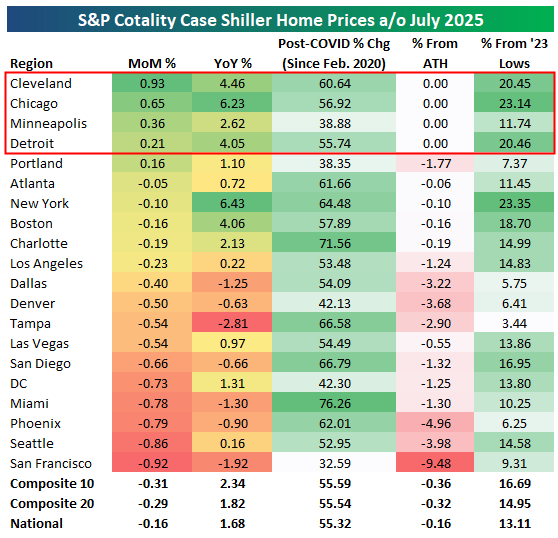

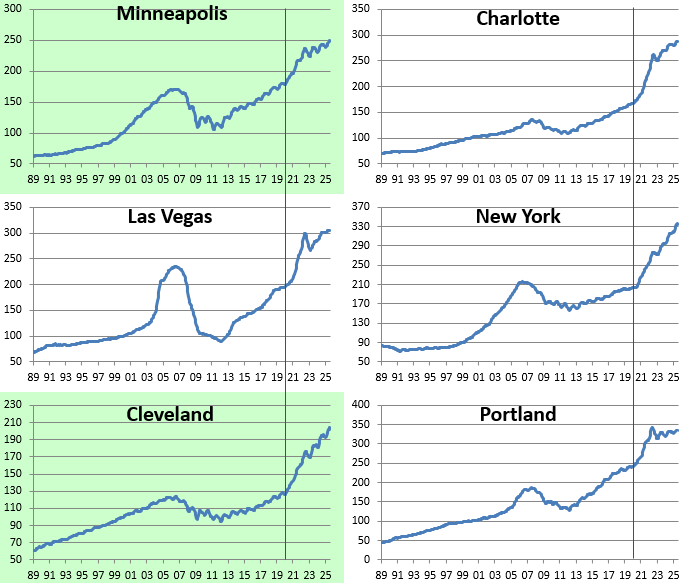

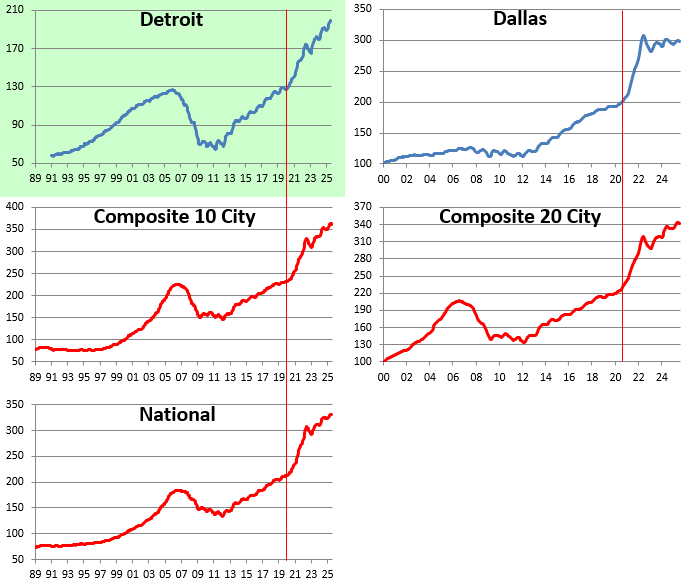

Midwest Resilience vs. Coastal Fatigue

The latest S&P Case-Shiller home price data paints a clear regional divide in the U.S. housing market. Midwest cities were up on the month and remain at all-time highs (Cleveland, Chicago, Minneapolis, Detroit), while cities in the South and West continue to struggle.

Strength in the Midwest appears to be driven by relatively lower absolute price levels, tight supply, and steady migration in from more expensive regions.

In the South and West, many metros that were pandemic-era darlings are now rolling over. Places like San Francisco, Phoenix, Seattle, Las Vegas, Tampa, and Miami all saw monthly declines and remain below all-time highs. San Francisco was down the most of any metro on the month with a drop of 0.92%, while Tampa is down the most year-over-year at -2.8%.

Along with the Midwest, major metros in the Northeast like Boston and New York that are also supply constrained remain up solidly year-over-year and were only down slightly on the month.

Based on the latest Case Shiller data, the dynamic has flipped: instead of “Sun Belt boom, Rust Belt lag,” the post-COVID housing cycle now features a Midwest resilience vs. coastal fatigue narrative.

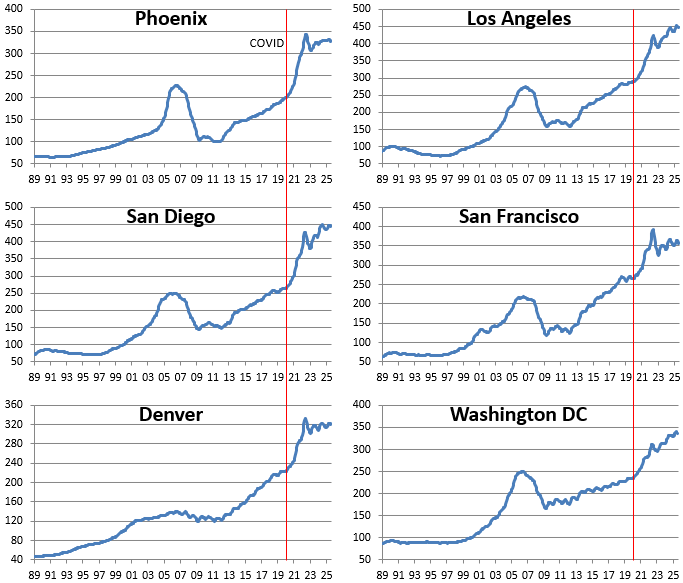

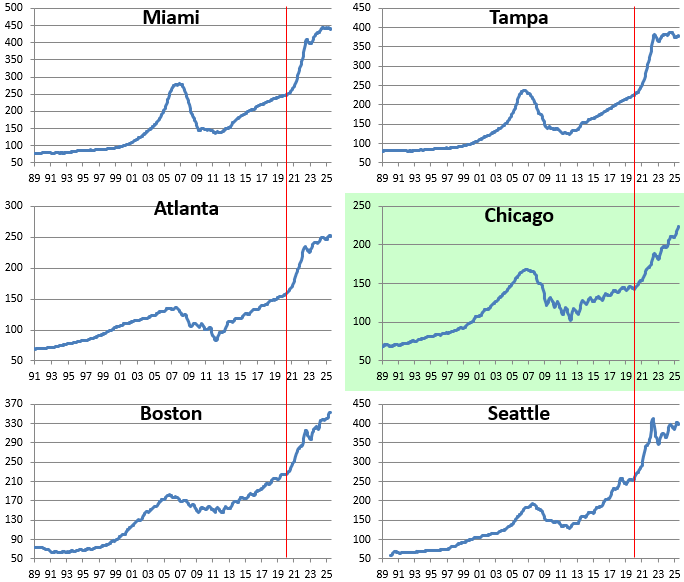

Below are price charts for each of the metros tracked. The four Midwest cities that hit all-time highs in the latest month are highlighted in green.

Bespoke’s Morning Lineup – 9/30/25 – Tuesday, The New Monday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is easy to ignore the rain if you have a raincoat” – Truman Capote

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Be sure to catch Paul Hickey today on CNBC’s Squawk on the Street at 10 AM.

It’s a modestly negative tone this morning as S&P 500 futures trade down 0.2% and the Nasdaq is down slightly less. Headline writers are attributing the weakness to concerns over a government shutdown, but those fears didn’t seem to bother anyone yesterday. Maybe it’s just Tuesday (see below). Treasury yields are slightly higher, crude oil is down nearly 1%, gold and other precious metals are lower across the board, as is crypto.

Overnight, Asian stocks were mostly lower. Japan traded down 0.3% as market expectations for a rate hike increase, and the government raised its forecasts for consumer spending for the first time in over a year. PMI data in China was mixed, with the manufacturing component coming in slightly ahead of forecasts (but still below 50) while the services index missed expectations.In Europe, most major indices are little changed as economic data in Germany (Retail Sales) and France (CPI) missed expectations.

In the US today, we’ll get the Chicago PMI, which always seems to disappoint, at 9:45 followed by JOLTS and Consumer Confidence at 10 AM. The only earnings report of note is Nike (NKE) after the close.

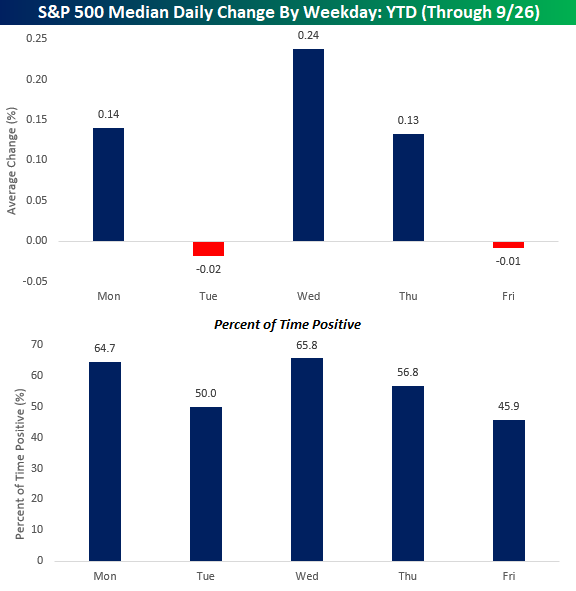

What’s so bad about Monday anyway? Lately, not much. The S&P 500 rallied 0.26% yesterday for its fourth straight positive start to the week and continuing a trend that has been in place for most of the year. Through last Friday, Mondays have been the second most positive weekday of the year with a median gain of 0.14% and gains 64.7% of the time. The only day of the week that has been stronger this year is Wednesday, with its median gain of 0.24% and gains 65.8% of the time.

\While Mondays have been strong, Tuesday is the new Monday as it ranks as the weakest weekday of the year with a median decline of 0.2% this year and gains just half of the time. The only other day of the week that has experienced negative returns on a median basis this year is Friday. So, maybe it shouldn’t come as any surprise that futures are lower this morning.

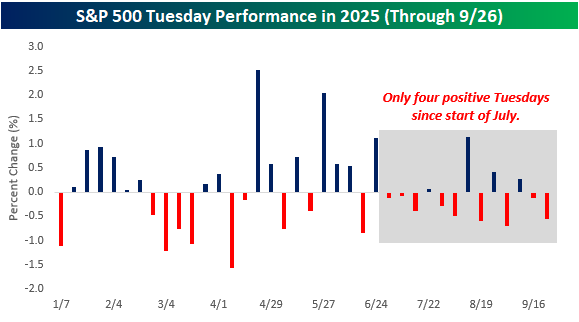

Looking at Tuesday performance more closely, the third quarter has been especially weak. Since the start of July, only four of the twelve Tuesdays have seen gains, so if the S&P 500 can manage to squeeze out a gain today, it would break what has been a pretty consistent trend of recent weakness.

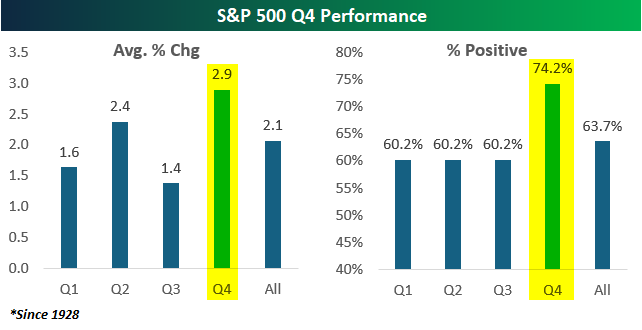

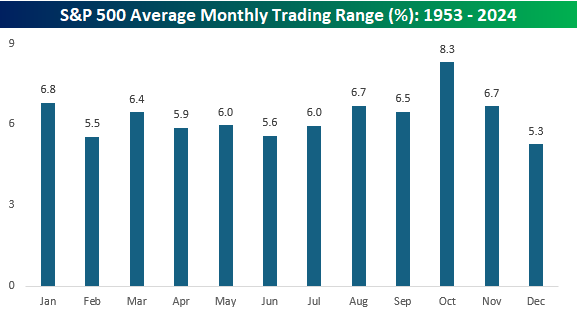

Today marks the last trading day of Q3, which has historically been the weakest quarter of the year. Since 1928, the S&P 500’s average performance during Q3 has been a gain of 1.4% with positive returns 60.2% of the time, but returns in Q4 have been better than and more consistent to the upside with an average gain of 2.9% and gains just under three-quarters of the time. For more analysis on quarterly seasonality, make sure to check out Monday’s Chart of the Day.

While Q4 has historically been strong, buckle up for some volatility. The chart below shows the average monthly trading range of the S&P 500 since 1953 (when the five-day trading week in its current form started). October’s average high-low spread (%) has been 8.3% which far surpasses the average monthly range of any other month. The next closest month is January at 6.8%. What’s notable about the 1.5 percentage point spread between the most volatile and second most volatile months is that it’s also the same as the spread between the second most volatile (January) and the least volatile months (December).

The Closer – Credit Cooking, Retail Risk, AI Targets – 9/29/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a check up on the health of leveraged loan activity (page 1) followed by an update on regional Fed manufacturing indices (page 2). We then review the performance of some of today’s top performing stocks, namely those associated with retail risk appetite (page 3) in addition to how far AI stocks are trading relative to price targets (page 4). We finish with an update on some Brazilian data releases (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q3 2025 Earnings Conference Call Recaps: Carnival (CCL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Carnival’s (CCL) Q3 2025 earnings call.

![]()

Carnival (CCL) is the world’s largest cruise company, serving millions of guests annually across North America, Europe, and Asia, offering vacation experiences that blend transportation, lodging, dining, and entertainment in one package. Its global footprint gives insight into leisure travel demand, consumer discretionary spending, and how travel trends shift across regions. Carnival’s scale, private island destinations, and disciplined capacity growth make it a bellwether for evolving consumer preferences in the broader travel industry. Carnival posted record net income of $2B, with yields up 4.6% on strong close-in demand and onboard spending. Bookings set new highs, with nearly half of 2026 already sold at higher prices and 2027 off to an “unprecedented” start. Celebration Key, the company’s new private Caribbean destination, generated 1.5B media impressions and is driving ticket premiums, while a pier expansion at Half Moon Cay will add lift in 2026. Minimal capacity growth (about 0.8% in 2026) and diversified strength in Europe and Alaska provide a favorable supply-demand backdrop. CCL shares popped 5.3% at the open on 9/29 but slumped more than 9% from the opening high despite the triple play…

Continue reading our Conference Call Recap for CCL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Q4 Seasonal Trends

Bespoke’s Morning Lineup – 9/29/25 – 1999 All Over Again?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Never make anything more accurate than it needs to be.” – Enrico Fermi

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After last trading to record highs last Monday, US equities are kicking off the week on a positive note once again this week as deal-making activity provides a boost to investors concerned about market valuations. Both the S&P 500 and the Nasdaq are indicated to open up by over 0.50%. Crude oil is down over 2%, which also helps, while gold is up over 1% and Bitcoin and Ethereum are both up close to 2% after some rough trading last week.

The pace of earnings activity will be incredibly slow this week, with Nike (NKE) the only notable report of the week (Tuesday). Economic data will pick up the slack, though, with multiple PMI readings, Consumer Confidence, and Non-Farm Payrolls.

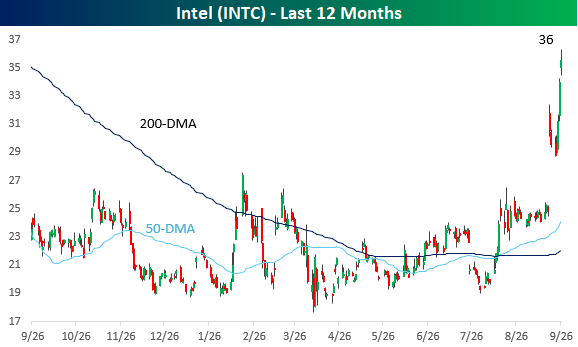

Like the S&P 500, which hit an all-time high last week before pulling back modestly, the Philadelphia Semiconductor Index (SOX) also hit an all-time high last Monday and then pulled back a little bit but still managed to finish the week up by 1.2%. What’s been interesting about the SOX this year, though, is which stocks are leading. A list of some of the index’s best performers this year looks like a time warp from the late 1990s, with stocks like Rambus (RMBS), Micron (MU), Lam Research (LRCX), and Intel (INTC) all up over 75%! INTC was up over 20% just last week! Meanwhile, Nvidia (NVDA), the leader of the AI revolution, has been in the middle of the pack, managing a gain this year of ‘only’ 33%.

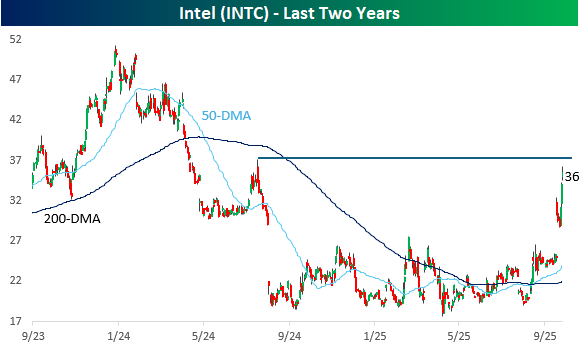

On a one-year basis, INTC’s chart looks a lot like ones from the 1990s as the stock has gone parabolic over the last two months, surging close to 90%!

On a two-year basis, INTC’s move looks more modest. Last Friday’s surge topped out just shy of the high it reached in the summer of 2024 right before it plunged 50% in a matter of weeks!

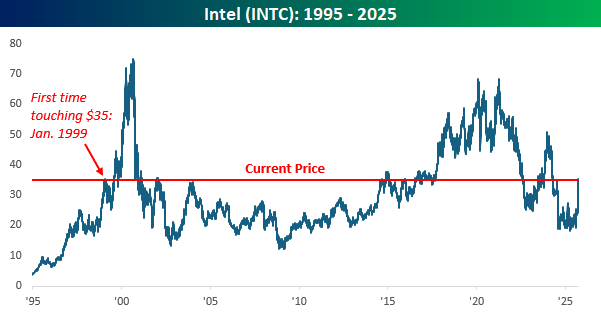

As impressive as INTC’s run has been in the last couple of months, it is still a shell of its former self. It’s still down close to 50% from its high in 2021. Additionally, while there has been a lot of talk lately about the market feeling like 1999, with INTC closing at $35 and change last Friday, it’s back to levels it first crossed back in January 1999!

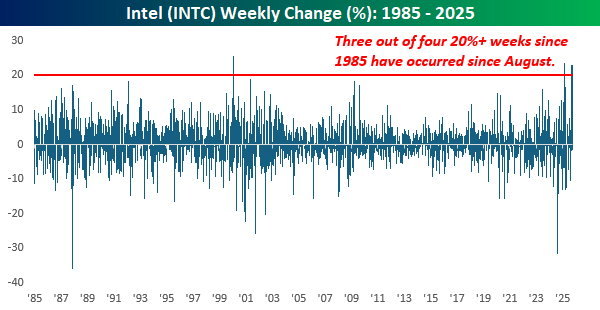

Perhaps the most amazing thing about the recent moves in INTC is that last week’s gain of 20% was the third week in the last seven that the stock rallied 20%+. How crazy is that? Since 1985, there has only been one other week outside of the last seven that the stock rallied 20%+.

Brunch Reads – 9/28/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Fourth Time’s A Charm: On September 28, 2008, a slender rocket named Falcon 1 rose from the remote Kwajalein Atoll in the Pacific and carved SpaceX into aerospace history. It was the company’s fourth attempt to prove it could pull it off, after three consecutive failures. SpaceX had just enough money and parts for this final shot, and a failure could have ended the company before it truly began. When the rocket cleared the atmosphere and delivered its payload into orbit, Falcon 1 became the first privately developed, liquid-fueled rocket to reach space. The moment validated not just the engineering team’s relentless work but also Musk’s insistence that a startup could challenge an industry long dominated by governments and defense contractors. Within weeks, NASA awarded the company a major contract for cargo resupply to the International Space Station, giving SpaceX a lifeline and a mandate. From that improbable success in 2008, SpaceX would scale up, build Falcon 9, and ultimately redefine the economics of spaceflight.

AI & Technology

America’s top companies keep talking about AI — but can’t explain the upsides (Financial Times)

Big companies talk up AI, but their own filings show fuzzy payoffs: 374 S&P 500 firms mentioned AI on earnings calls, and most were upbeat, while risk sections stress cyber attacks, legal fights, and projects that don’t work. Clear wins cluster around the data-center boom and back-office chores, boosting power suppliers, miners, and equipment makers, while some consumer brands point to things like making TV ads. A recent study finds that most workplace pilots fail, and many 10-Ks warn that AI may not lift profits at all. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

Q3 2025 Earnings Conference Call Recaps: Costco (COST)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Costco’s (COST) Q4 2025 earnings call.

![]()

Costco (COST) is a membership-based warehouse retailer selling a limited, high-turn assortment of essentials and “treasure-hunt” discretionary items under national brands and its Kirkland Signature (KS) label. It operates 914 warehouses worldwide, plus growing e-commerce and last-mile channels, serving households and small businesses seeking quality and value. What’s impressive is the company’s cult-like loyalty (92.3% US/Canada renewal). Because Costco buys in bulk and keeps prices tight, it’s a good read on what shoppers want, where costs are rising (food, labor, tariffs), and how global sourcing is changing. Beyond groceries, it also sells travel, has pharmacies/optical, big gas volumes, and is starting to make ad dollars from its website. It’s still opening stores in the US and overseas, and expanding Business Centers for small businesses. Comparable sales rose 5.7% (6.4% ex-gas/FX) and e-commerce +13.6%. Membership fees hit $1.72B and paid members reached 81M, with executive members totalling 38.7M (74% of sales). Longer hours added about 1% to weekly US sales, and faster checkout and lower spoilage helped offset wage hikes. To handle tariffs, Costco is moving suppliers and leaning into Kirkland. Digital upgrades included passwordless sign-in, anti-bot “waiting rooms,” and tracking “digitally enabled” sales. Despite EPS and sales beats, COST shares declined more than 2.5% on 9/26…

Continue reading our Conference Call Recap for COST by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

The Bespoke Report – 9/26/25 – Upside Volatility & The Impact of AI

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. This week we are focused on two themes: the increasingly volatile foundations of the stock market rally and the circular AI boom along with its impacts on valuations, the energy system, and economic growth. We also review a series of key economic data this week that should ease many fears of slowing consumer spendingas well as inflation data and the week that was in global asset markets. Give it a read!