Brunch Reads – 10/19/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Be Kind. Rewind: On October 19, 1985, the very first Blockbuster Video store opened in Dallas, Texas, changing how Americans watched movies. Blockbuster wasn’t just another mom-and-pop video rental shop, but a sleek, systematized operation that could stock thousands of titles at once, all neatly arranged by genre and alphabetized for easy browsing. At a time when most video stores carried only a few hundred tapes, walking into Blockbuster felt like entering a movie lover’s paradise. By the 1990s, those blue-and-yellow storefronts were everywhere. There were more than 9,000 locations worldwide at its peak. Families made Friday night trips to Blockbuster a ritual, hoping the latest release hadn’t already been rented out (imagine if you couldn’t watch a movie on your favorite streaming service because too many people wanted to watch at once!).

Unfortunately for all of us who held Blockbuster near and dear, its reign didn’t last forever. Netflix’s rise and the overwhelming transition to streaming hit the rental giant hard, and by the early 2010s, its empire collapsed. Blockbuster was a place to discover films in a shared, physical space, which is a nostalgic experience that today’s younger generations miss out on, despite its inconvenience compared to streaming. We’ll never forget wandering the aisles, looking at cover art, and finding a movie we would’ve never otherwise watched with our friends and family.

Markets & Investing

Gundlach Sees Private Credit As Top Candidate To Start Next Financial Crisis (Financial Advisor Magazine)

Jeffrey Gundlach warned that private credit could trigger the next financial crisis, calling it the top risk in today’s markets. He said competition among lenders has turned cutthroat and compared private credit ETFs to “square pegs in round holes.” Gundlach argued the industry’s marketing misleads investors about risk and volatility, drawing parallels to the pre-2008 buildup of toxic debt. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

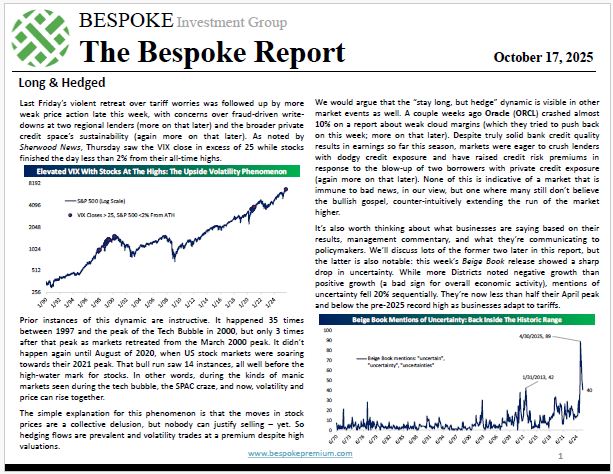

The Bespoke Report – Long and Hedged – 10/17/25

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium.

Bespoke’s Morning Lineup – 10/17/25

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The main purpose of the stock market is to make fools of as many men as possible.” – Bernard Baruch

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity markets have seen volatility tick up as we enter the second half of October, which is very typical for this time of year. US index futures were down more than 1% a few hours ago, but they’ve rallied back to the flat-line after President Trump made comments diffusing trade drama with China.

As shown below, key index ETFs remain within their long-term uptrends above their 50-day moving averages, with the exception of the S&P 500 Equal Weight.

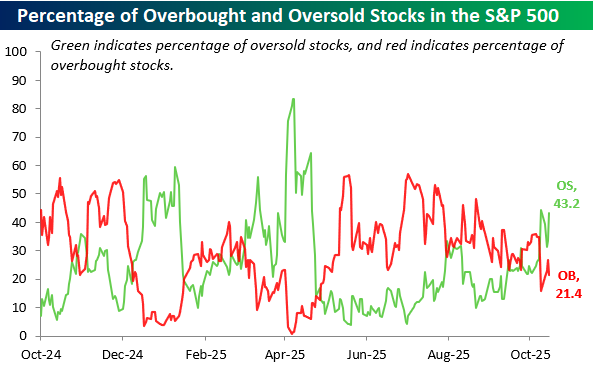

While cap-weighted large-cap indices remain strong on the surface, a much higher percentage of stocks in the S&P are now oversold (43.2%) than overbought (21.4%).

The Closer – Data Center Credit, Homebuilders, Margins – 10/16/25

Log-in here if you’re a member with access to the Closer.

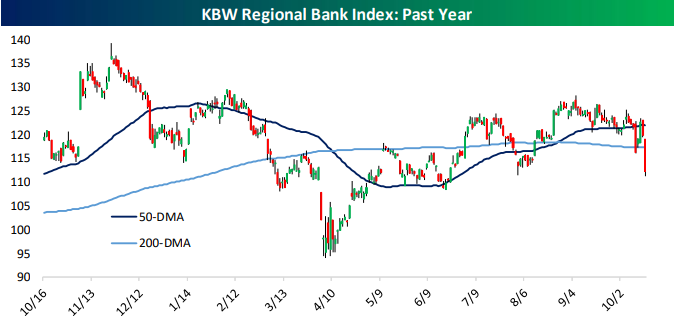

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a look at the pain in regional banks (page 1) in addition to the happenings in data center credit markets (page 2). After that, we check in on homebuilders (page 3) before switching over to macro data that includes an update of our Five Fed Composite (page 4), New York area service sector data (page 5), and the close out with commentary on some macro trends playing out in earnings (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q3 2025 Earnings Conference Call Recaps: Big Banks & Asset Managers

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap, available to Bespoke subscribers, covers Q2 2025 earnings calls from BlackRock (BLK), Citigroup (C), Goldman Sachs (GS), JPMorgan (JPM), Wells Fargo (WFC), Bank of America (BAC), and Morgan Stanley (MS).

The third quarter of 2025 showed steady, broad-based strength across Wall Street as capital markets regained momentum and consumer strength held firm. Goldman Sachs (GS) reported a 42% jump in investment banking fees, while JPMorgan Chase (JPM) and Bank of America (BAC) each saw double-digit growth as corporate confidence returned amid policy clarity on tariffs and taxes. Wells Fargo (WFC) gained 120 bps of US market share in investment banking and advised on the year’s largest deal, Union Pacific’s $85B acquisition of Norfolk Southern. AI adoption became a central theme. Citi (C) reported 7 million internal AI tool uses and BlackRock (BLK) projected $1.5 trillion in data-center investment needs over the next five years, signaling technology’s accelerating impact on efficiency and infrastructure demand. Credit quality remained healthy, deposit flows stable, and interest-rate sensitivity manageable despite expectations for further rate cuts in 2026. Regulatory recalibration, including anticipated Basel III and G-SIB relief, was seen as a tailwind. Overall, banks entered the final quarter with revived deal pipelines, strong household balance sheets, and a clear focus on turning AI enthusiasm into tangible productivity gains…

Continue reading our Conference Call Recap for BLK, C, GS, JPM, WFC, BAC, and MS by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 10/16/25 – Sentiment Weakens

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“‘That didn’t work’ is cool, but ‘that won’t work’ is not a way to go through life.” – John Mayer

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

A triple play from Taiwan Semiconductor (TSM)—beating on earnings, revenue, and guidance—is lifting US equity futures, with technology stocks at the forefront. This rally is notably happening despite the President stating yesterday after the close that, “We are in one now,” in reference to a trade war with China. There are also signs that China’s aggressive stance on rare earth exports could be backfiring, as it has started to cause a more unified front between the US and other international partners.

Today was supposed to be a busy one for economic data, but the government shutdown put the kibosh on that, and the only report released was the Philly Fed Manufacturing report, which came in weaker than expected. The pace of earnings, however, remains active, and once again this morning, we’re seeing generally strong results.

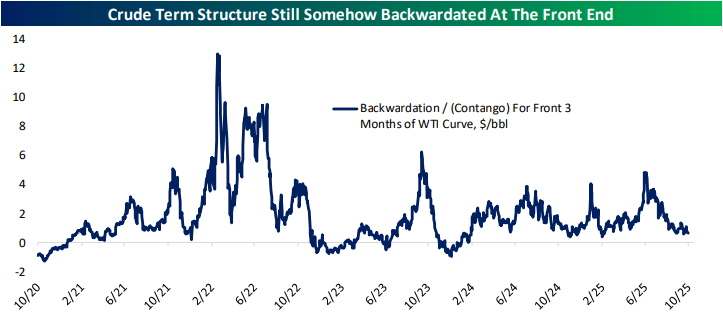

Outside of equities, crude oil is fractionally higher but still well below $59 per barrel, the 10-year yield is trying to hang on to 4%, gold and other precious metals are rallying (what else is new), and crypto is also rallying after what has been a rough week for the sector.

It’s been a somewhat rocky week for US equities, although by the standards of October, it’s hard to get too worked up. After trading at an all-time high intraday last Thursday, the S&P 500 closed modestly lower on the day. That modest decline was followed on Friday by a sharp 2.7% decline in the S&P 500 as trade issues with China and concerns over corporate credit in the auto sector nudged investors to take some risk off the table. This week started on a positive note as the S&P 500 erased half of the losses from last Thursday and Friday, but intraday trading has been more volatile, and there’s been more of a tendency to sell rips than buy dips.

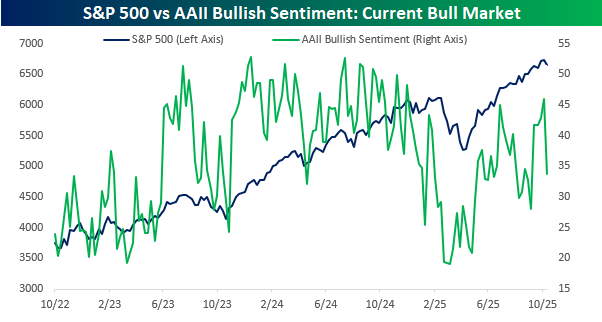

The skittishness showed up in investor sentiment this week as the weekly American Association of Individual Investors (AAII) survey showed that bullish sentiment dropped from 45.9% to 33.7% for the lowest reading in a month. The decline in bullish sentiment comes even as the S&P 500 closed within 2% of a record high yesterday. While bullish sentiment was routinely near 50% throughout 2024 as the market rallied, in the bounce off the April lows, investors have been much less willing to hop on the bandwagon.

Along with the modest weakness in US stocks over the past five trading sessions, global equities have also been under pressure. Of the US-traded ETFs tracking the stock markets of the seven G7 countries, all but France (EWQ) traded lower in the five trading days ended yesterday, and the US was stuck right in the middle with a decline of 1.2%. The biggest laggards have been Italy (EWI) and Germany (EWG) as their the only two below their 50-DMAs. Markets have certainly been on a tear this year as six of the seven ETFs listed have rallied at least 20% this year, but in the short run, they’ve mostly worked off their overbought conditions as France is the only country still in extended territory.

Chart of the Day: Wall Street Winning

The Closer – La Cucaracha, Beige Book, Credit Cards – 10/15/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a note on the two significant credit blow ups in September and a quantitative look at the Beige Book (page 1). Next, we review the latest credit card delinquency rates (page 2) and wrap up with a recap of the latest transport earnings (page 3).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Wealth Management Report – October 2025

Please click here or on the link below to read our latest quarterly Wealth Management Report. You can learn more about Bespoke’s wealth management services available to investors here or by calling our office at 914-315-1248.

Below are links to prior quarterly Wealth Management Reports: