The Closer – Triple Plays, Kids These Days – 11/12/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start with a review of the elevated rate of triple plays reported this earnings season (page 1). We then dive into generational differences in wealth, incomes, and employment (pages 2 – 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Short Interest Update

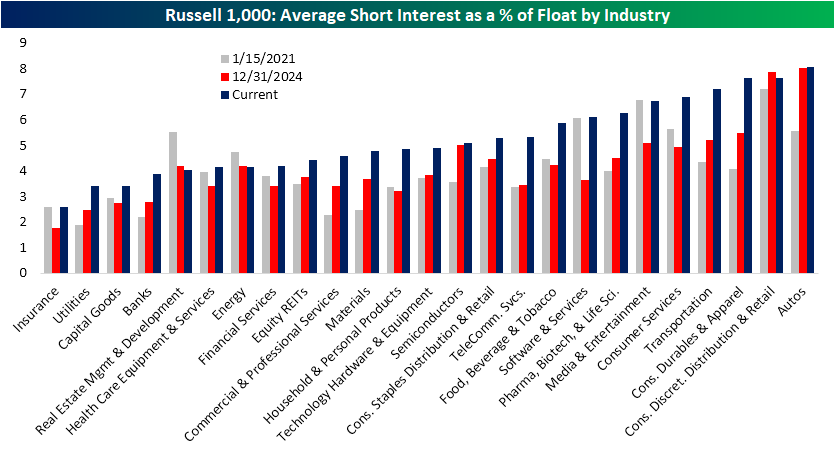

Short interest data through the end of October was published yesterday. For Russell 1,000 stocks, the average stock has 5% of float sold short (median: 3.5%). For the whole of the index, that is up a little over 1 percentage point from the start of the year. In the chart below, we show the average reading across all industries as of 10/31, at the end of last year, and in mid-January 2021, at the height of the meme-stock mania. Current readings are up versus both of those prior periods for Russell 1,000 members. With that said, we would note that for 2021 readings, the Russell 1,000 did not include some of the most heavily shorted and focused-on names like GameStop (GME) and AMC Entertainment (AMC), to name a few.

On an industry level, auto stocks continue to see elevated levels of short interest, largely due to the presence of EV-only names like Lucid (LCID). Behind that, many retailers and consumer-facing stocks make up the list of most shorted, while industries like Consumer Durables and Apparel, Transportation, and Consumer Services have seen some of the largest average increases. Another industry high up on the list of YTD increases has been out of the Tech sector, with Software and Service stocks going from 3.6% average short interest to 6.1% today. Conversely, the only declines in short interest since the start of the year have come out of the Energy and Real Estate Management and Development industries.

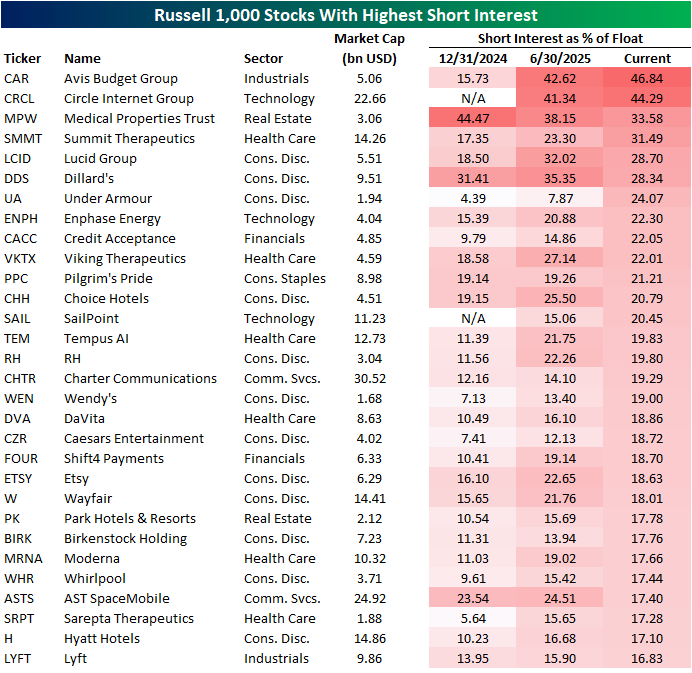

In the table below, we show the individual index members with the highest level of short interest per the latest update. Two stocks have readings above 40%: Avis Budget (CAR) and Circle (CRCL). The latter is a newer stock with an IPO in early June, while the former has seen short interest triple since the start of the year. The third-highest reading in short interest comes from Medical Properties Trust (MPW). While short interest remains high above 30%, it is down from 44.5% entering the year.

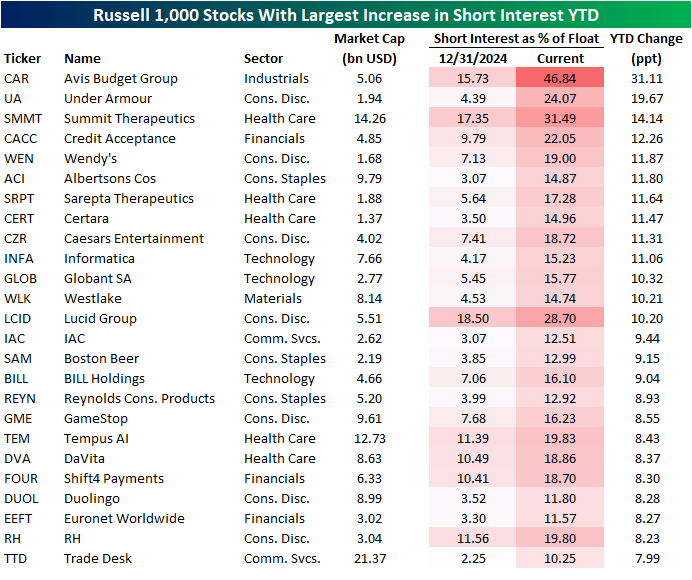

Again, CAR has seen short interest triple this year. That is by far the largest uptick of any current Russell 1,000 members. The next largest increase, Under Armour (UA) has seen an increase of less than 20 percentage points so far, although it started 2025 with a mid-single digit reading.

Chart of the Day: Biotech Rally Continues

Bespoke’s Morning Lineup – 11/12/25 – Broader

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Luck’s a revolving door, you just need to know when it’s your time to walk through.” – Stan Lee

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After two days of gains to start the week, futures are looking to make it a third as the S&P 500 trades up 0.4% while the Nasdaq jumps 0.6%. Treasury yields are lower after being closed for Veterans Day yesterday. Crude oil is down over 1% and back down to testing the $60 level, while gold and crypto trade higher with Bitcoin up over 2% and near $105K, while Ether surges 3.5% to just under $3,600.

Asian stocks were mostly higher overnight. South Korean stocks led the way as the ultimate high-beta country stock market rallied 1.1%, taking its week-to-date gain to 5%. It’s now less than 1.7% from its record closing high just over a week ago. The Nikkei was up 0.4% while China’s Shanghai Composite was down modestly (-0.1%) despite comments from the PBoC that it would maintain its appropriately loose monetary policy stance.

The rally in Asia made its way into Europe this morning, and the STOXX 600 is already up 0.7% in early trading. Most major benchmarks are more than 1% higher, while the UK’s modest decline sticks out like a sore thumb. German CPI rose 0.3% which was right in line with expectations and up from a rate of 0.2% in September, while the UK weakness has been driven by homebuilders after a warning from Taylor Wimpey.

Throughout the shutdown, there was a view that once Election Day passed, we would start to see some movement towards a resolution on the government shutdown. The idea was that Democrats wanted to use the shutdown as an election issue, so once the election passed, some members would cross the aisle. Sure enough, a week after Election Day, the Senate passed the resolution to fund the government, setting the stage for federal workers to get back to work.

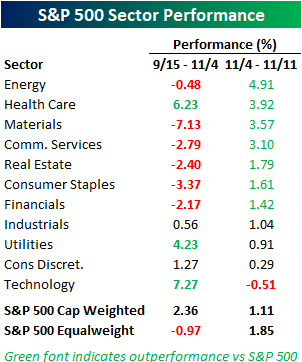

Election Day also served as a catalyst for the market to broaden out. The chart below shows sector performance from mid-September (when the odds of a shutdown on betting markets first exceeded 50%) through Election Day and then in the week since Election Day. During the shutdown period from 9/15 through 11/4, it was a narrow market rally as just three sectors outperformed the S&P 500, led higher by Technology, Health Care, and Utilities. Since Election Day, though, seven out of eleven sectors have outperformed the index as the market broadened out. As a result, the equal-weighted index has performed much better than the cap-weighted index, whereas it seriously lagged the cap-weighted index during the shutdown period.

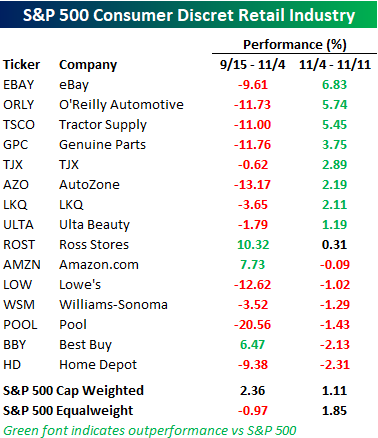

Stocks tied to the consumer have also rebounded. The table below shows the performance of stocks in the S&P 500 Consumer Discretionary and Retail Group during both the “shutdown period” and over the last week. During the shutdown period, just three of the 15 stocks in the group were up as investors avoided the group, as a large block of US consumers weren’t getting paid, and consumers overall retrenched given the uncertainty. On an average basis, they fell 5.7% compared to a gain of 2.36% for the S&P 500, which was driven higher by a handful of mega-cap names. Since Election Day, though, there has been a reversal in the performance of stocks tied to the consumer. 9 of the 15 stocks in the group have seen positive returns over the last week, and 8 of them have outperformed the S&P 500.

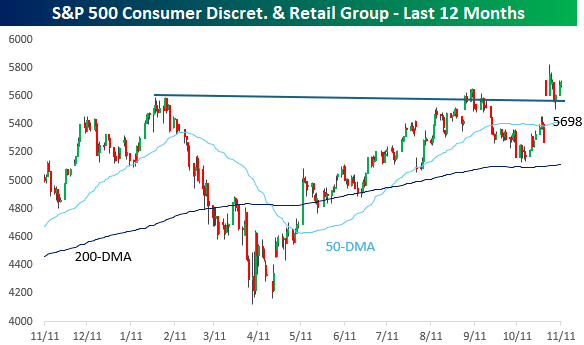

The group’s chart also looks positive. After hitting a marginal new high just before the shutdown, the group pulled back sharply towards its 200-DMA. After that successful test in mid-October, the group has erased all its initial shutdown declines and broken out to new highs and above resistance, forming what some technicians would describe as a positive cup and handle formation. We’ll drink to that!

The Closer – ADP, AI Returns, Sentiment – 11/11/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at weekly ADP employment figures and some news flow surrounding transportation names (page 1). Next, we look at profitability and return on investments and assets for hyper-scalers (page 2) before closing out with a look at various forms of investor sentiment (page 3).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Small Businesses Concerned Over Quality

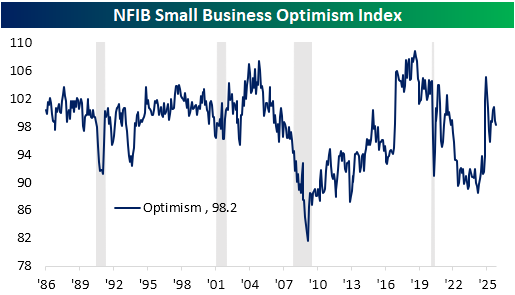

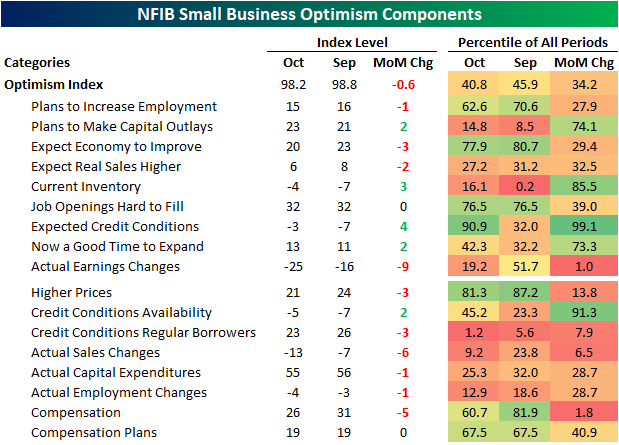

This morning’s only economic report was the NFIB’s Small Business Optimism Index. It came in weaker than expected, falling to 98.2 versus forecasts of 98.3. The index has now fallen in back-to-back months as it hovers in the 40th percentile of its historical range..

Of the inputs to the headline number, breadth was actually mixed with four declining categories, four rising, and the remainder going unchanged. As for the non-input categories, breadth was far weaker, with only two indices avoiding declines. As for those that did drop, there were a handful that saw bottom decile monthly declines.

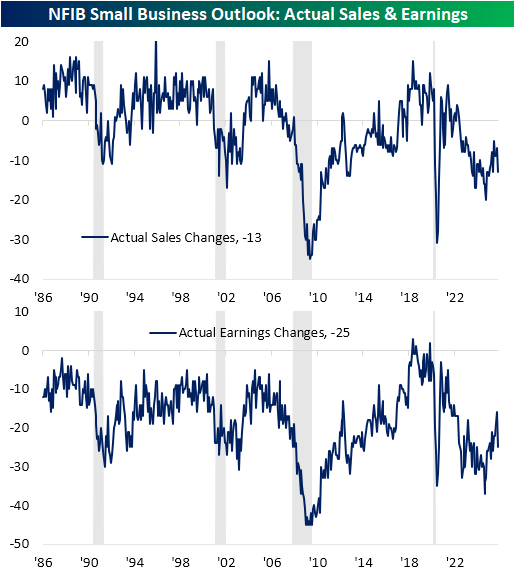

Of the inputs to the headline number, the most concerning decline was in actual earnings changes. That index fell 9 points MoM, which ranks as the sixth largest monthly decline in the index’s history (data going back to 1986). Given that those are bottom-line changes, the cause for weaker earnings could be weaker revenues, higher costs, or a mix of both. However, weaker revenues appear to be the culprit.

For starters, the index for higher prices remains in the top quintile of readings throughout the survey’s history, but there was a 3-point decline in October. Meanwhile, the index for actual sales changes (not an input into the overall optimism index) fell by a more significant 6 points in October to the lowest level since May. That six-point decline ranks in the 6th percentile of monthly moves, and the current level of the index is now in the bottom decile of historical readings. Interestingly, despite the moves in those indices, the share of respondents who reported poor sales as their biggest problem was unchanged at 10%.

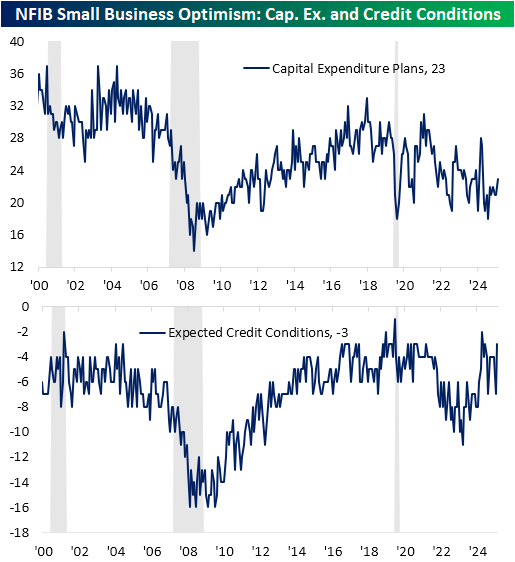

One bright spot of the October report concerned financing. As rates have continued to fall, there has been an uptick in capex plans and expected credit conditions. For the latter, the 4-point jump month-over-month was one of the largest one-month increases on record, and current levels are also at the high end of the past few decades’ range.

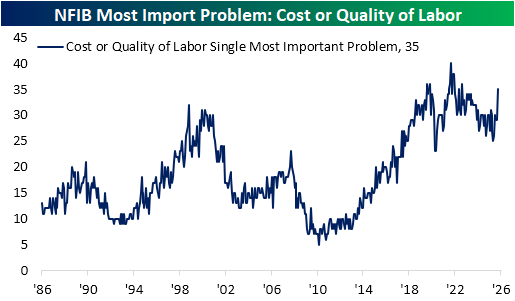

As noted earlier, for the topics labeled as small businesses’ biggest problems, poor sales didn’t move in October, and at 10% it ranks as the fourth-biggest issue of the 10 listed. Ahead of poor sales, inflation took a step back, falling 2 percentage points to 12% of responses, and taxes fell an identical amount to 16% of responses. The single most commonly reported problem in October was quality of labor. Of responding firms, 27% reported this as the biggest issue. In spite of other weak indicators concerning labor markets, that was the strongest reading since November 2021 and was up significantly from September. In fact, the 9 percentage point jump marked a record monthly gain. What’s more, the share reporting cost of labor as the biggest issue actually fell 3 percentage points to 8%.

Chart of the Day – Impressive Streaks on Both Sides of the Equator

Bespoke’s Morning Lineup – 11/11/25 – Defense Stocks Stand Out

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The test of success is not what you do when you are on top. Success is how high you bounce when you hit the bottom.” – George S. Patton

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are in hangover mode after yesterday’s big rally to start the week, which put a dent in a good chunk of last week’s decline. At this point, S&P 500 futures indicate just a modest decline of 0.2% at the open, while the Nasdaq is down twice that. The Treasury market is closed for Veterans Day, but both crude oil and gold are up about 0.8% while cryptocurrencies are lower. In Europe, the STOXX 600 is up another 0.8%, while Asian stocks were mixed.

Judging by the metrics of General Patton’s quote above, the bounce of last April’s low was one of the most successful of all time, and even the bounce off last week’s test of the 50-DMA has, initially at least, been successful. On this Veterans Day, we want to thank anyone who has served in the US Armed Forces for their service. Everyone in the country appreciates their service.

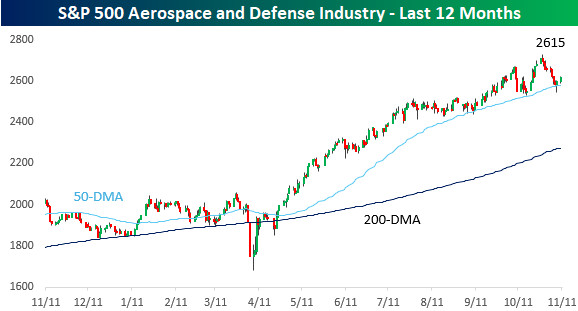

Given the Veterans Day holiday, we wanted to look at how aerospace and defense stocks have performed so far this year. From last November through early April, the group traded mostly sideways, so while it didn’t rally with the broader market to close out 2024, it didn’t feel much of the effects of the tariff-tantrum in March and April. Since those April lows, though, the sector has taken off and not looked back. Like the S&P 500, the group tested its 50-DMA last Friday but managed to bounce and stay above that level.

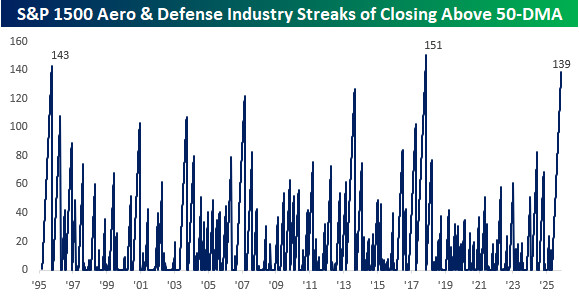

With the successful test of the 50-DMA, the Aerospace and Defense industry has closed above its 50-DMA for 139 trading days. That’s the longest streak since a record 151 trading days in 2017 and ranks as the third-longest in the last 30 years.

The Closer – AI Credit, Consumer Expectations, Mortgages – 11/10/25

Log-in here if you’re a member with access to the Closer.

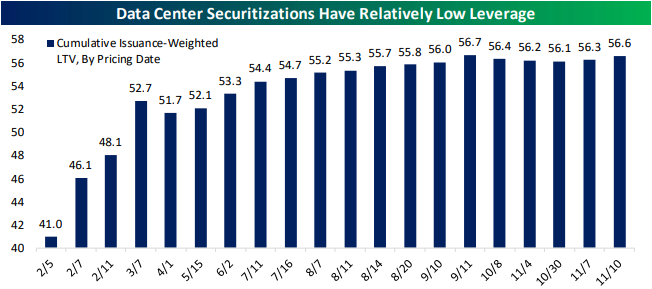

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a dive into debt related to datacenters and AI names (pages 1 and 2). We then pivot into the latest data from the New York Fed’s Survey of Consumer Expectations (pages 3 – 5) including some other housing data from ICE’s Mortgage Monitor report (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!