The Closer – Cruising to New Highs, Jobs, Inventories – 2/4/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a look into the massive recovery in cruise stocks (page 1). We then look at the latest job openings data through Indeed (page 2) and JOLTS data sets (page 3). Next, we review the latest Fedspeak and earnings (page 4) before switching over to a look at housing inventories (pages 5 and 6) and delinquency data (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Chart of the Day – Strange Bedfellows

Bespoke’s Paul Hickey on CNBC’s Squawk Box (2/4/25)

Bespoke’s Paul Hickey was invited on CNBC’s Squawk Box on 2/4/25 to discuss markets. You can watch the segment by clicking here or on the image below:

Bespoke’s Morning Lineup — 2/4/25

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I think that people just have this core desire to express who they are. And I think that’s always existed.” – Mark Zuckerberg

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures are flat this morning after a wild Monday that saw the major indices gap down 1%+ but recover about half of that during the trading day. While Mexico and the US came to an agreement to delay tariffs by 30 days around lunch time, Canada and the US didn’t agree to their short-term truce until just after the close.

Today is the 21st birthday of Facebook, which was launched by Mark Zuckerberg in his Harvard dorm on 2/4/2004. Below is a snapshot of one of the first versions of the Facebook profile, which was entirely used on desktops and laptops at that point because the iPhone was still a few years away.

It took eight years from launch for Facebook (now META) to IPO. Below is a look at the growth of a $10,000 investment in META at its IPO price back in May 2012. $10k at the IPO held through yesterday’s close would now be worth roughly $184,200, but it certainly didn’t get there in a straight line.

Recall that META went “all-in” on the metaverse in the early 2020s, which, combined with a nasty bear market for growth stocks, resulted in a 76% drawdown from September 2021 to November 2022.

At its lows in late 2022, a $10k investment at META’s IPO in 2004 had fallen from more than $100k at its 2021 peak all the way down to just $23,400.

Zuckerberg reversed course on the metaverse to try and stop the bleeding, and he dubbed 2023 the “year of efficiency” for the company. Around the same time, ChatGPT came along to start the AI Boom. Since its lows in 2022, META has rallied nearly 700% and currently sits at all-time highs.

The Closer – Tariff Turmoil, ISM Expands, Home Improvement – 2/3/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look at the S&P 500’s impressive intraday reversal and country ETF performance (page 1). We then look at the latest construction spending data (page 2) and the snapped streak of contractionary readings for the ISM manufacturing index (page 3). We finish with a weekly rundown of positioning data (pages 4 – 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Chart of the Day: DOGE Dogs

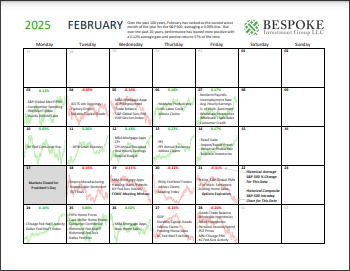

Bespoke Market Calendar — February 2025

Please click the image below to view our February 2025 market calendar. This calendar includes the S&P 500’s historical average percentage change and average intraday chart pattern for each trading day during the upcoming month. It also includes market holidays and options expiration dates plus the dates of key economic indicator releases. Click here to view Bespoke’s premium membership options.

Bespoke’s Morning Lineup — 2/3/25

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“As has been often noted but seldom heeded, selling during a selling panic is rarely an effective strategy.” – Bill Miller

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Last Monday it was DeepSeek, this Monday it’s tariffs that have US equity futures trading down 1-2% ahead of the open. With President Trump ordering tariffs on imports from China, Mexico, and Canada over the weekend, below are price charts of ETFs covering these three countries plus the US (SPY). We include where each ETF is currently trading in the pre-market so you can see how big this morning’s declines are relative to the last six months of action. Yes, all four are set to open quite a bit lower, but all four will also still be above their lows seen over the last month or so. Mexico (EWW) is the only ETF of the group that will be near six-month lows if it opens at current levels.

Brunch Reads – 2/2/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Shadow or No Shadow?: On February 2nd, 1887, the town of Punxsutawney, Pennsylvania, held the first official Groundhog Day celebration, an event that would grow into one of America’s quirkiest and most enduring traditions. This was the first time a groundhog named Punxsutawney Phil was formally recognized as the nation’s premier meteorological marmot.

The roots of Groundhog Day trace back to European traditions, particularly Candlemas, a Christian festival marking the midpoint between winter and spring. If the weather was clear on Candlemas, more winter was ahead; if cloudy, an early spring was on the way. German immigrants in Pennsylvania brought their own spin to the superstition, swapping out European hedgehogs for the more abundant groundhog.

Over the decades, the spectacle has grown, incorporating top hats, formal proclamations, and a touch of theatricality. Whether or not Phil’s predictions hold up scientifically (spoiler: his accuracy is questionable), Groundhog Day remains a beloved tradition in the US.

AI & Technology

OpenAI says it has evidence China’s DeepSeek used its model to train competitor (Financial Times)

OpenAI suspects Chinese AI startup DeepSeek of using its proprietary models to train a rival AI through a technique called distillation, which extracts knowledge from a larger model to boost a smaller one. DeepSeek’s shockingly low-cost approach has already produced models that rival top US AI, sparking fears that unauthorized training on OpenAI outputs gave it an unfair advantage. OpenAI itself faces legal challenges over alleged copyright violations, so it’s a messy battle over AI training data and intellectual property. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

Bespoke Report – 1/31/25 – Disruption

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. In this week’s report, we cover DeepSeek, the Fed, earnings, the economy, and some of the market’s wild moves.