Chart of the Day: AAII Bears Surge

The Bespoke 50 Growth Stocks — 2/27/25

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There were 17 changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 2/27/25 – What Happened?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I really try to put myself in uncomfortable situations. Complacency is my enemy.” – Trent Reznor

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Well, we made it through Nvidia (NVDA). The hype surrounding last night’s earnings report was as high as we can remember for any stock reporting earnings in the past and reminiscent of Cisco (CSCO), Intel (INTC), or Microsoft (MSFT) reports in the late 1990s, or Apple (AAPL) reports in more recent years. NVDA’s report wasn’t great, but it wasn’t bad either. The company managed to report better-than-expected EPS and sales, while slightly raising sales guidance. That was good enough for investors who had set the bar low in recent weeks. The stock is currently trading just about 2.5% higher in the pre-market, and Nasdaq and S&P 500 futures are riding its coattails trading higher by more than 0.5%.

Bulls will take it, but as the last few days have shown us, we’re in a market environment where what the market is doing right now is hardly indicative, no less a guarantee of where we’ll be an hour from now let alone the end of the day. Add to that a ton of economic data and several Fed speakers on the calendar, and it’s sure to be an eventful day!

What happened to sentiment? Everywhere you look, fear has set into the collective mood. Indices that measure economic uncertainty have shot up to record highs, even taking out their prior extremes from the early days of Covid. The latest measures of consumer sentiment from the University of Michigan and the Conference Board both also showed much larger than expected declines in their latest readings. But nowhere has the negative turn in sentiment been more pronounced than in the equity market.

The CNN Fear & Greed Index gauges stock market behavior by looking at momentum, breath, options activity, strength in the junk bond market, and demand for safe havens. As of this morning, the index was at 21, putting it in the “Extreme Fear” range.

Over the last year, the current level of the CNN Fear & Green Index is among the lowest. The only time it was lower was in early August when markets briefly sold off as the Japanese equity market crashed over 10% in a single day.

The Closer – Tariff Talk, NVDA Earnings, Gas Investment – 2/26/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with some commentary regarding another round of tariff headlines (page 1) followed by an update on the latest earnings including results from NVIDIA (NVDA) in addition to multiple other big names (page 2). Then then discuss the latest investments from gas companies (pages 3 and 4). We finish be looking at new home sales (page 5), the 7-year note auction (page 6), and the latest EIA data (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q4 2024 Earnings Conference Call Recaps: TJX (TJX)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers TJX’s (TJX) Q4 2025 earnings call.

![]()

TJX (TJX) is an off-price retailer of apparel and home goods, operating over 5,000 stores under brands like T.J. Maxx, Marshalls, HomeGoods, and Sierra in the US, Canada, Europe, and Australia. TJX posted a strong quarter, with 5% comp sales growth entirely driven by higher customer transactions, reinforcing its ability to attract shoppers across income levels. Shrink improvements added 70 basis points to margins. The company plans 130 new store openings in 2025, raising its long-term store target to 7,000 locations. While tariffs on China-sourced goods present a short-term headwind, TJX remains confident in its sourcing flexibility. E-commerce sales grew but remain a small part of the business. TJX shares were up roughly 2.5% on 2/26…

Continue reading our Conference Call Recap for TJX by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q4 2024 Earnings Conference Call Recaps: Axon (AXON)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Axon’s (AXON) Q4 2024 earnings call.

![]()

Axon (AXON) is best known for its TASER devices, body cameras, and evidence management software. The company’s Axon Cloud ecosystem integrates AI, drones, and real-time data to improve law enforcement and emergency response. AXON serves law enforcement agencies, federal and military clients, private security firms, and international markets. AXON closed 2024 with $2 billion in revenue, marking its third consecutive year of 30%+ growth. TASER 10 sales doubled TASER 7 adoption rates, and demand continues to outpace supply, and the company is investing to fix that imbalance. AI-driven solutions like Draft One (AI report-writing tool by analyzing body cam footage) and the AI Era Plan (premium subscription plan bundling AI tools) saw record adoption, with over 100,000 AI-generated reports completed. AXON’s international bookings grew 50% sequentially, while enterprise sales tripled. The Dedrone (counter-drone technology) acquisition and Skydio (autonomous drones) are helping the company respond to heightened border security and military demand. Meanwhile, political and legal hurdles in Arizona could force a headquarters relocation. AXON enters 2025 with over $10 billion in future contracted bookings, forecasting another 25% revenue growth year. The stock opened 18.2% higher on 2/26…

Continue reading our Conference Call Recap for AXON by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: S&P 500 Dips From a High

Bespoke’s Morning Lineup – 2/26/25 – Separate Ways

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Greatness comes from character, and character is not formed out of smart people, it’s formed out of people who suffered.” – Jensen Huang

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After four days in a row of losses for the S&P 500 and Nasdaq, including three days in a row of 1%+ losses for the Nasdaq, bulls are getting a chance to catch their breath this morning as futures are higher across the board. The breather comes just in time as markets gear up for Nvidia’s (NVDA) earnings report after the close. How the market reacts to that report could give us a good idea of the market tone as we head into spring. Besides NVDA after the close, New Home Sales is the only economic report on today’s economic calendar, and we’ll also hear from Richmond Fed President Barkin at 8:30 and Atlanta Fed President Bostic at noon.

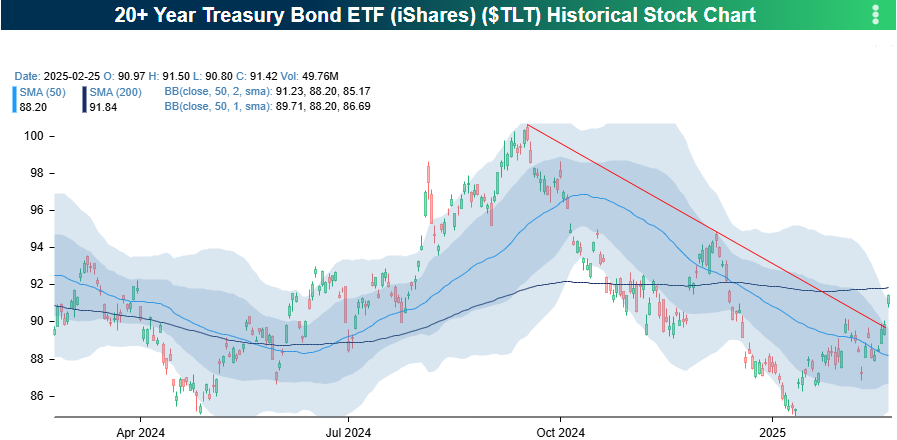

Everything has been turned upside down in the markets over the last week. While equities and bitcoin have pulled back sharply, fixed-income ETFs – especially treasuries – have surged. As shown in the snapshots from our Trend Analyzer, the US Aggregate Bond ETF (AGG) and every Treasury ETF with a maturity longer than a year has moved into extreme overbought territory (more than two standard deviations above their 50-day moving averages (DMA). On the equity side, the S&P 500 hasn’t quite reached oversold territory, but all the other major index ETFs along with Bitcoin have now moved at least into oversold territory. It seems like a while since we last saw a situation where fixed-income securities were moving to the right side of their ranges while equities were moving to the left.

The iShares 20+ year US Treasury ETF (TLT) had a notable move yesterday as it broke its downtrend that has been in place since the peak (trough in long-term yields) right as the Fed started cutting rates in September. It finished yesterday right below its 200-DMA, which could act as resistance going forward, but you have to start somewhere!

Get Invested: Time Heals

Our “Get Invested” series is a simple yet powerful resource designed to help anyone understand why investing in stocks for the long term is one of the best financial decisions they can make. The slide below from our Get Invested piece is titled “Time Heals.”

The stock market can be very forgiving if you give it time. The four worst times to buy equities over the last forty years were in September 1987 (before the 1987 crash), March 2000 (before the dot-com peak), October 2007 (before the Financial Crisis peak), and February 2020 (before the COVID crash). Since each of those four ill-fated buy points, US stocks have still returned at least 7.7% on an annualized basis and have outperformed bonds over all four spans.

If you have any questions about our Get Invested resource, please email us or give us a call at 914-315-1248. You can view the full piece by becoming a Bespoke client.

Click here to learn more about Bespoke’s wealth management services.

The Closer – Drawdowns, Staples vs. Cyclicals, Confidence – 2/25/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we cover a large range of topics including the Nasdaq’s rapid pullback (page 1) and its historic parallels (page 2). We also check in on the relative performance of Consumer Discretionary and Consumer Staples stocks (pages 2 and 3) in addition to the confirmations from other assets (page 4). Switching over to economic data, we review growth outlook concerns on account of the latest consumer confidence data (page 5). We then dip into the cratering of crypto prices (page 6) and Case-Shiller home prices (page 7). We finish with a review of the 5-year note auction (page 8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!