See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It is the obvious which is so difficult to see most of the time.” ― Isaac Asimov

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After opening firmly lower last night, equity futures gained steam overnight on hopes of a ceasefire in the Iran war. After Iranian officials refuted those reports, though, we’re basically back to the unchanged line. It could be worse!

Following last Friday’s better-than-expected jobs report, treasury yields are modestly higher, with the 10-year yield at 4.36%. In commodity markets, crude oil is surprisingly contained at a decline of less than 1%, although that could change as reports surface that Israel launched strikes on Iran’s largest petrochemical facility. Gold prices are fractionally higher at just under $4,700 per ounce, and Bitcoin is up a healthy 3% and making a run back towards $70K.

It was a positive start to the week in Asia, even as China and Australia were closed. Japanese markets rallied 0.6%, while South Korea gained 1.4%. In Europe, markets are all closed, so there’s little economic or market data for investors to react to, leaving plenty of room for investors to focus their attention on Iran and the energy markets.

In the US today, the only report on the calendar is ISM Manufacturing at 10 AM. Economists expect the headline reading to pull back from 56.1 to 54.9.

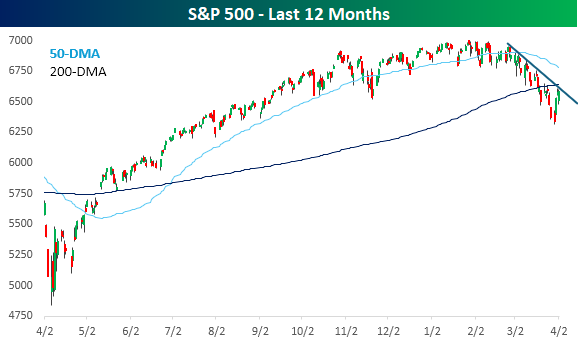

Even though it was a short one, last week’s gains were enough to make it the best weekly performance of the year. Bulls will take gains whenever and wherever they can, but the rally, at this point, has done little to break the overall trend that has been in place for the last several weeks. The S&P 500 remains below the 200-DMA, and the downtrend remains intact. Whether the rally is a dead cat bounce or the real thing, it has to start somewhere, and only time will tell. At this point, though, bulls will need to see more improvement before starting to feel more confident.

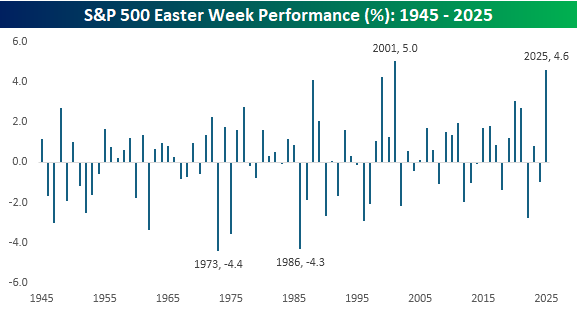

As mentioned above, many international markets are still closed for the Easter holiday, so we wanted to see what seasonal headwinds or tailwinds the Easter holiday has historically had on the market. The chart below shows the S&P 500’s performance in the week after Easter for every year since 1945. Overall, the S&P 500 has averaged a 0.2% gain during Easter week with positive returns 59% of the time, but most years have been anything but average. Look no further than last year when the S&P 500 rallied 4.6% for its second-best Easter week performance, trailing only the 5.0% gain in 2001.

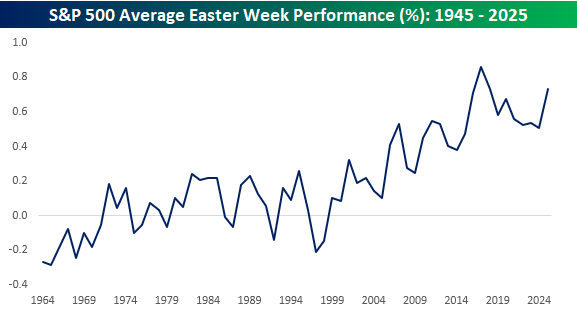

Looking at the chart above, you can see that performance around Easter week has been better more recently than in the years immediately after WWII, with fewer large declines during the Easter week. The chart below shows the 20-year average of the S&P 500’s Easter week performance since 1964, and clearly shows the improving trend. In 1964, the 20-year average performance was negative, but it has steadily increased over time, especially over the last 25 years. The 20-year average peaked in 2017 at 0.9%, but at 0.7% now, it’s the third-best reading of any since 1964, trailing only the readings in 2017 and 2018.

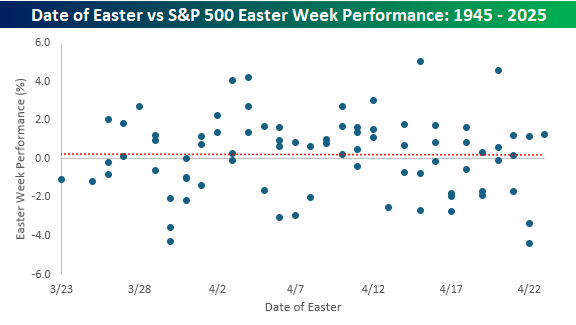

Unlike most other holidays, which fall on a specific date or particular point on the calendar, Easter can fall anywhere from late March to late April. Given Easter’s floating nature, we were curious to see if there was any correlation between the market’s performance during Easter week and when it falls on the calendar. The scatterplot below shows the date of every Easter since 1945 and the S&P 500’s performance during Easter. As shown, while Easter week performance has improved over time, there is zero correlation between performance and when Easter falls on the calendar. Nothing to see here.