See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Wrong does not cease to be wrong because the majority share in it.” – Leo Tolstoy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After modest gains in US equities to start the week, futures have a positive bias this morning ahead of a relatively quiet day for economic data. The only report on the calendar is the NFIB Small Business Confidence report for August, which came in slightly better than forecasts, rising from 100.3 to 100.8.

An even bigger news story today will be the Preliminary Benchmark Payrolls Revision from the BLS. While the data is even more backward-looking than most other economic data, the headline number is expected to show a large downward revision to the number of jobs created between April 2024 and March 2025. Economists forecast the downward revision to anywhere between a loss of 450K to 900K, so you can guarantee that at the very least, both sides of the political aisle will seize on the headlines.

Finally, Apple (AAPL) will hold its ‘awe-dropping’ iPhone event at 1 PM eastern, where a new line of phones, along with updated iPads, watches, and AirPods, are expected. If you didn’t see it yesterday, make sure to check out yesterday’s Chart of the Day, where we looked at the stock’s performance around prior iPhone launch events.

Besides the modestly positive tone in equities, treasury yields are slightly higher, but the 10-year is still under 4.07%, and WTI, while higher by about 1%, is still below $63 per barrel. In the metals market, performance is mixed with modest gains in gold and platinum, while silver is slightly lower. Lastly, crypto is higher across the board with Bitcoin, Ethereum, and Solana all up by close to 1%.

Outside of the US, Asian equities were mixed overnight. The Nikkei broke a streak of three straight days of at least 1%+ gains with a decline of 0.4%, while China’s Shanghai Composite fell 0.5%. European stocks are hanging on to small gains (0.14%). Germany is the biggest outlier with a decline of 0.4% while other countries in the region are offsetting those losses.

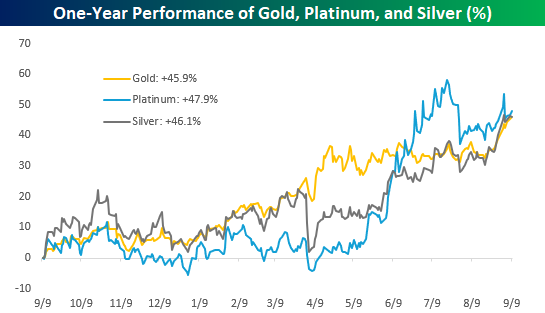

When it comes to precious metals and crypto, the first asset that immediately comes to mind for most people is gold, and given its recent performance, deservedly so. However, when you look at gold’s performance in comparison to other major precious metals like platinum and silver, their performances are nearly identical. Over the last year, gold has gained 45.9% while platinum and silver have rallied 47.9% and 46.1%, respectively. Their paths haven’t necessarily been identical, but they’ve ended up at the same place.

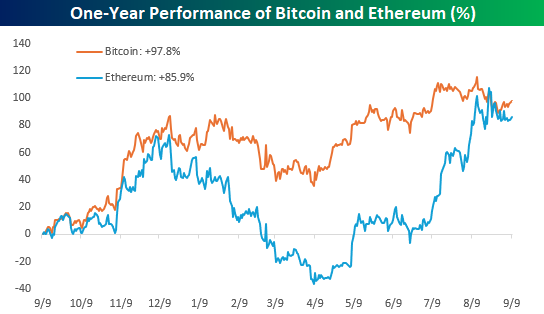

In the crypto space, Bitcoin is effectively the gold standard, and for most ‘investors’, it is the crypto market. Here again, Bitcoin’s performance hasn’t been much different than the ‘silver’ of that market – Ethereum. Here again, the paths of the two cryptos haven’t necessarily been the same, but they’ve essentially ended up at the same place. While Bitcoin is up 97.8% over the last year, Ethereum’s 85.9% gain isn’t far behind, especially for an asset class as volatile as crypto.

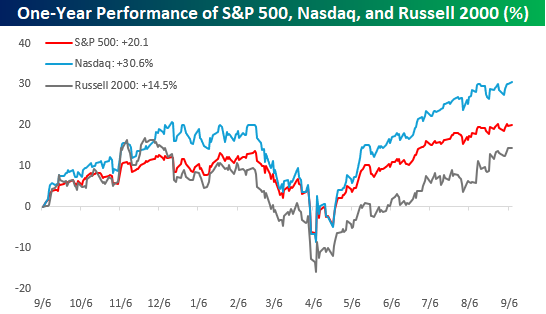

While the major metals and cryptos have had similar performances to each other over the last year, the same can’t be said for equities. While their trading patterns have been similar over the last year, the Russell 2000’s 14.5% gain comes up well short of the S&P 500’s 20.1% gain and pales in comparison to the Nasdaq’s gain of over 30%. While precious metals and, to a lesser degree, the leading cryptos have been almost interchangeable in their performance over the last year, equities, the most liquid of the three asset classes, have seen more varied returns.