See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you fail to prepare, you’re prepared to fail.” – Mark Spitz

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Equity futures are skewed to the upside as yields rise, but a weaker-than-expected ADP Employment report at 8:15 has put a modest damper on the tone in equities. The 8:30 batch of data showed that Unit Labor Costs were weaker than expected, while Non-Farm Productivity came in better than expected. Jobless claims were mixed, with initial claims rising slightly while continuing claims saw a modest decline.

In Asia, most equity indices in the region were higher, with Japan leading the way (+1.5%), but China bucked the trend and traded lower on reports that the government is considering restrictions on stock trading to reduce speculation. European equities are also higher this morning, with France being the exception, following a sharp decline in shares of Sanofi.

As concerns over an uptick in inflation continue to simmer (even as employment slows), raising questions about how much the Fed will realistically be able to cut rates, the yield on the 10-year US Treasury doesn’t seem overly worried. Since peaking early in the year at just over 4.8%, yields have been steadily trending lower with a series of lower highs since Spring. During this period, there has been a floor at the 4.20% level, but this morning that level is being tested again as the yield briefly moved below 4.2%.

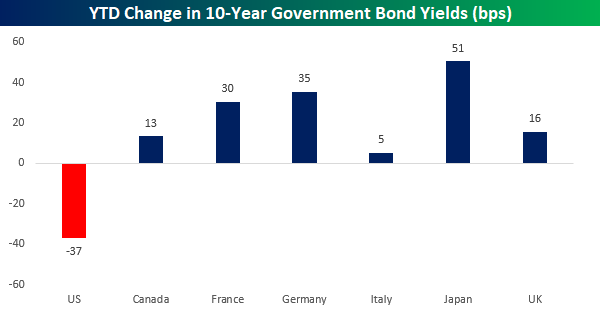

The drop in yields has also occurred against a backdrop of chatter over whether global investors were looking to exit US assets. In global fixed income markets, that doesn’t appear to be the case. While the 10-year yield has declined 37 basis points (bps) YTD, the sovereign 10-year yield of every other G7 country has increased anywhere from 5 bps in Italy to 51 bps in Japan.

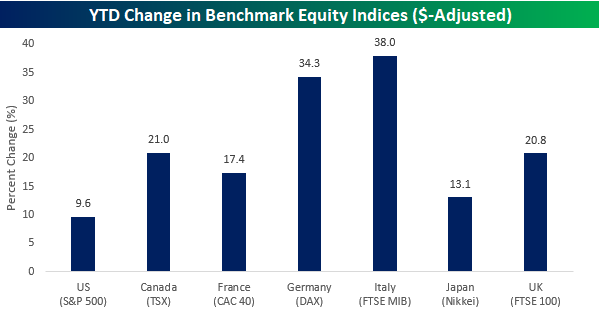

In global equity markets, US exceptionalism hasn’t been as evident. While the S&P 500 is up 9.6% YTD, the benchmark equity index of every other G7 country is up by a larger amount. Japan is the closest in terms of performance to the US (+13.1%) while Italy and Germany are both up over 30%!

While US equities entered September right near all-time highs with healthy gains for the year, investor sentiment remains skeptical. The latest sentiment survey from the American Association of Individual Investors (AAII) showed a decline in bullish sentiment to 32.7% while bearish sentiment increased to 43.4%. The results pushed the bull-bear spread further into negative territory, marking the fifth straight week that bears outnumbered bulls in what has been a relatively consistent trend of negative sentiment this year.

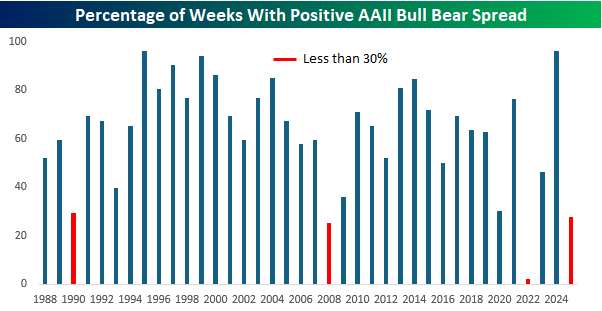

The chart below shows the percentage of weeks by year when the weekly AAII survey had a positive bull-bear spread. So far this year, the spread has been positive just 28% of the time, which stands in stark contrast to last year, when the bull-bear spread was positive 96% of the time, tied only with 1995 for the most ever in a year. If the current pace of negative readings continues, it will be just the fourth year that the bull-bear spread was positive less than 30% of the time, with the only other years being 1990, 2008, and 2022. It’s understandable to see negative sentiment in bear market/recessionary environments like 1990, 2008, and 2022, but what’s the excuse this year?