See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We’re moving from a world where we have to understand computers to a world where they will understand us.” – Jensen Huang

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

If you missed yesterday’s CNBC segment discussing recent market rotation, you can watch it by clicking on the image below.

It’s another quiet market morning with futures indicating just a modest gain at the open. Treasury yields are modestly higher across the curve, while crude oil is essentially flat at around $63 per barrel. In contrast, gold and other metals are slightly lower. There’s no economic data on the calendar this morning, and, outside of some earnings from retailers like Abercrombie & Fitch (ANF), Kohl’s (KSS), and Williams-Sonoma (WSM), the earnings calendar is light. Even the endless coverage of the Cook firing has subsided!

The quiet tone will change this afternoon when Nvidia (NVDA) reports after the close. Along with NVDA, we’ll also get reports from HP (HOQ), CrowdStrike (CRWD), NetApp (NTAP), and Urban Outfitters (URBN). The next two days will also be much busier on the economic calendar, so enjoy the calm while it lasts.

In Asia overnight, Japan was slightly higher while China traded lower as Industrial Profits for July fell 1.7% on a YTD basis. Australian stocks finished the session with fractional gains despite a CPI report which came in much higher than expected at 2.8% y/y versus forecasts for an increase of 2.3%.

European stocks are also trading much like US futures with little in the way of gains or losses. The STOXX 600 is up 0.15% with Germany trading slightly lower while France is bouncing back 0.45% from Tuesday’s 1.6% decline.

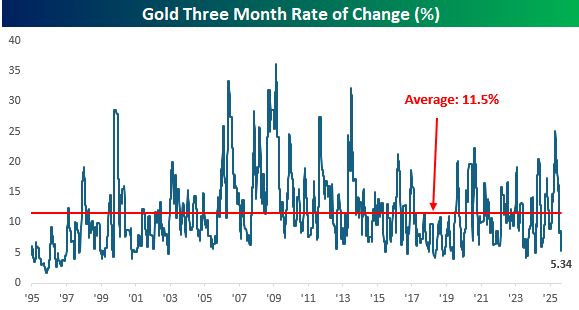

Gold prices are doing little this morning, and the last few months have been like watching paint dry for the yellow metal. After hitting an all-time high just above $3,500 per ounce in early April, gold has made multiple other attempts at breaking out above that level. While they have been unsuccessful, gold hasn’t sold off following those rejections, which has resulted in a relatively narrow range in recent months.

Over the last three months (63 trading days), in fact, the spread between gold’s intraday high and low has been just 5.34%, the narrowest three-day range since March 2024 and ranking in the bottom decile of three-month ranges over the last 30 years. This narrow range also marks a major shift from where this measure was four months ago in April, when the range topped 25% which was the widest since 2013.

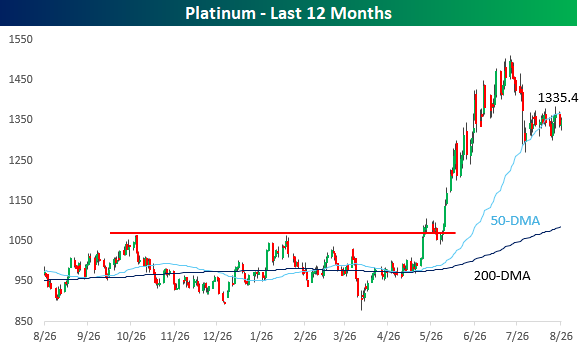

Like gold, platinum had been stuck in a range for several months from the second half of last year, with multiple run-ins with resistance just below $1,070. In late May/early June, though, it broke out of that range with vengeance surging as high as $1,500 before pulling back in July. Since that peak a little over a month ago, platinum has pulled back by about 11% and is now teetering on the 50-DMA, tenuously holding onto support. After such a large rally in such a short period, it’s only natural to see a pullback, so if these levels can hold, in the days ahead, platinum could start to look even more precious in the eyes of investors than it did even back in June.