See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Happiness in intelligent people is the rarest thing I know.” – Ernest Hemingway

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Stocks are poised to open the week higher this morning as we gear up for a busy week of earnings. The only economic indicator on the calendar this morning is Leading Indicators at 10 AM. In terms of earnings, we’ve already gotten reports from Cleveland Cliffs (CLF), Domino’s Pizza (DPZ), Roper (ROP), and Verizon (VZ). The only one of the four that missed EPS forecasts was DPZ, while it was the only one to miss estimates (barely) on the top line. After the close, the most notable reports on the calendar are Crown (CCK), NXP Semiconductors (NXPI), Steel Dynamics (STLD), and WR Berkley (WRB).

Outside of the US, Asian markets were mostly higher, while Japan was closed. Japan’s ruling party lost its majority in the weekend elections. While Asia was mostly higher, Europe is sitting on some modest losses in early trading with the STOXX 600 down 0.2%. Trade and tariffs continue to dominate the headlines there as the August 1st deadline approaches, and President Trump is pushing for 15% to 20% tariffs on all European imports.

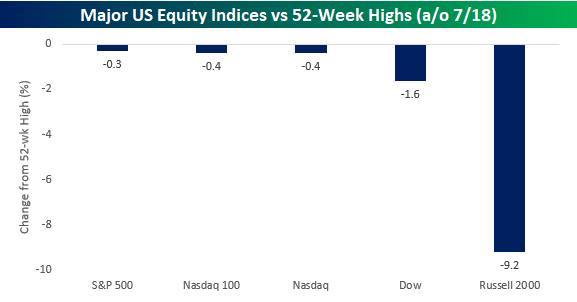

While the S&P 500, Nasdaq 100, and Nasdaq Composite all closed out the week within 1% of 52-week highs last Friday, the Dow Jones Industrial Average remains a little further off at 1.6%. The small-cap Russell 2000 remains in a league of its own, near correction territory at 9.2% below its 52-week high. Not all US equity indices are created equal.

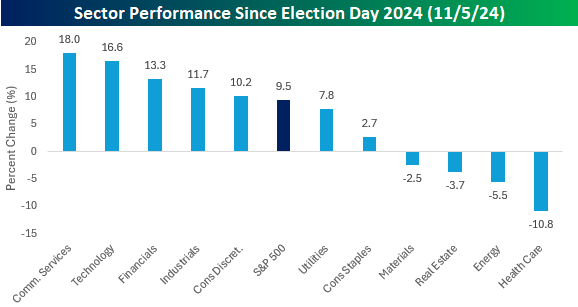

At the sector level, the haves vs have-nots is even more pronounced. Last Friday, just three sectors – Utilities, Technology, and Industrials – closed within 1% of their respective 52-week highs. After these three, Financials, Communication Services, and Consumer Staples closed out the week between 1% and 5% below their respective 52-week highs.

Nearly half of the S&P 500 sectors, however, remain more than 5% from their respective highs, including Energy (-11.7%) and Health Care (-16.3%), which are still deep in correction territory. While the Energy sector’s weight of 2.97% in the overall index is nearly inconsequential, the Health Care sector still has a respectable weighting of right around 9%.

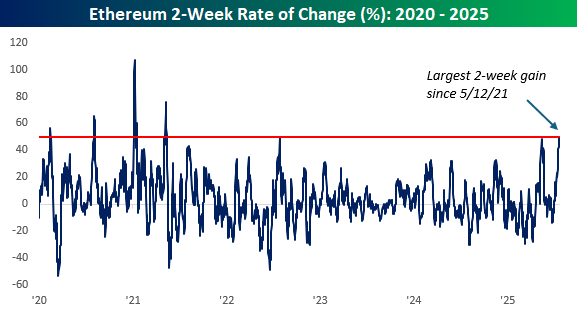

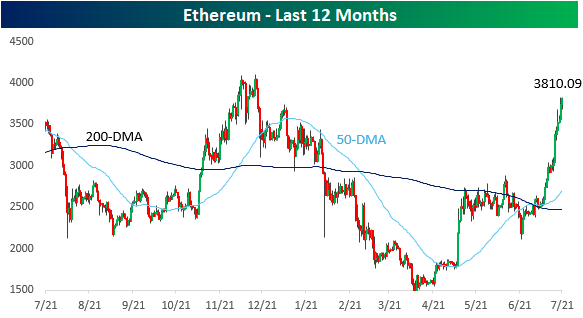

Outside of equities, the crypto space has been strong, and here, there’s been a relative rotation where the formerly overlooked Ethereum has been surging. After trading at $1,500 in April and below $2,500 as recently as July 4th, Ethereum is back up above $3,800 for the first time this year.

Based on where it’s trading this morning, Ethereum has rallied just over 50% in the last two weeks, which would put it on pace for the largest 14-day gain (crypto doesn’t take weekends off) in more than four years.