See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We seek friendly relations with all nations. Any nation can be our friend without being any other nation’s enemy.” – Richard Nixon

Bespoke’s Paul Hickey will be appearing on Making Money With Charles Payne today at 2 PM on Fox Business. Check it out!

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

S&P 500 futures are slightly higher this morning while the Nasdaq is slightly stronger, pointing to a gain of 0.33% as investors await the June PPI, hoping for a positive encore to yesterday’s tame CPI report. Treasury yields are moving higher, though, as the 10-year yield remains above 4.6%. In the energy market, crude oil prices are only fractionally higher despite a new round of attacks by the US on Iran. Gold is fractionally lower as it continues to hold above $4,000 per ounce, while Bitcoin quietly rallies as it moves up to $65,000.

Asian markets were mostly higher overnight, with the Nikkei rallying 1.5% while South Korea surged 6.2%. China was the outlier, falling 0.3% following a round of sluggish economic data. In Europe, stocks are lower across the board, but the losses are only fractional in nature as no major benchmark is down more than 1%. Industrial Production for the Eurozone unexpectedly declined 0.2% in May, versus expectations for an increase of 0.3%.

The data train continues to accelerate today with a busy slate of earnings results coupled with Empire Manufacturing and PPI at 8:30. Empire Manufacturing exceeded forecasts, coming in at 15.6 vs 9.2, and PPI was weaker across the board, coming in well below expectations. Headline CPI fell 0.3% m/m versus forecasts for no change, and the y/y reading dropped to 5.5% versus the 6.2% forecasts. Stripping out Food and Energy, the core reading came in at 0.2% m/m and 4.7% y/y versus expectations for increases of 0.3% and 5.1%, respectively. In reaction to the reports, futures are building modestly on their pre-market gains.

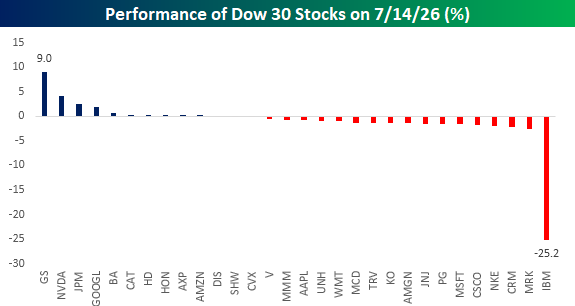

If ever there was an example of how earnings season can cause huge disparities in individual stock returns, yesterday’s performance of the Dow 30 components was Exhibit A. Fueled by better-than-expected EPS and revenue results, shares of Goldman Sachs (GS) topped the Dow performance chart yesterday with a rally of 9% and the best earnings reaction day for the stock since January 2019. While GS had one of its best earnings reaction days in years, IBM had its worst single-day performance ever with a decline of 25.2% after preannouncing weaker-than-expected results. Looking at the chart below, with yesterday’s disparate returns, the performance of the Dow 30 stocks looks more like a YTD chart than just one day.

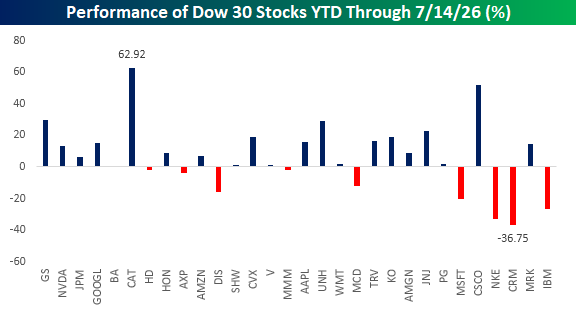

The YTD performance chart of Dow 30 stocks looks more like this. Even with yesterday’s big gains and losses, GS is not the best performing stock in the Dow YTD nor is IBM the worst performer. GS actually ranks third with a gain of just under 30%, trailing CAT and Cisco (CSCO). To the downside, IBM’s 26.7% YTD decline also ranks as the third worst performer in the index, ahead of only Salesforce (CRM), which is down 36.8% and Nike’s (NKE) decline of 32.7%.

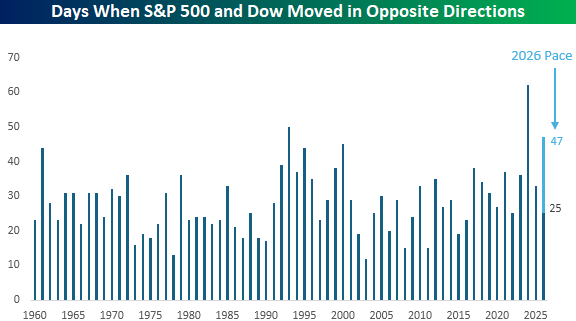

For a good part of yesterday’s session, it looked as though the S&P 500 would finish the day higher while the Dow would trade lower. The Dow managed to eke out a gain of 0.02% at the end of the day, avoiding a 26th session this year when the two indices moved in the opposite directions. The chart below shows the number of days by year when the Dow and S&P 500 moved in opposite directions. At 25 this year, 2027 is on pace for 47 diverging days between the two indices this year. If that pace keeps up, the year would finish in third for the most number of diverging days since 1960, trailing the peak of 62 in 2024 and 50 in 1993.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.