See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I always like to look on the optimistic side of life, but I am realistic enough to know that life is a complex matter.” – Walt Disney

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It may be Friday, but investors are in no mood to celebrate as equity futures are sharply lower. The Nasdaq is leading the losses, declining 1.28% while the S&P 500 is poised to open down by just under 1% (-0.90%). Treasury yields continue to march higher as they have all week, and in the commodity space, WTI crude oil is spiking 3% to just under $104 per barrel while gold is down over 2.5%. Bitcoin is also lower, falling by just 1%.

The weakness in US futures follows a lousy night in Asia. The Nikkei fell 2%, China was down over 1%, and South Korea plunged over 6%. Following these declines, all of Asia’s major indices finished the week lower. Higher yields contributed to the negative tone, and in South Korea, a potential labor strike at Samsung pressured that stock.

Weakness in Asia worked its way into Europe, and stocks are likewise lower across the board with declines of more than 1%. Here again, the primary culprit is higher yields, although CPI in Italy rose less than expected.

Getting back to the US, there’s not much in the way of earnings reports this morning, but at 8:30, we’ll get the release of the May Empire Manufacturing report, followed by Industrial Production and Capacity Utilization at 9:15.

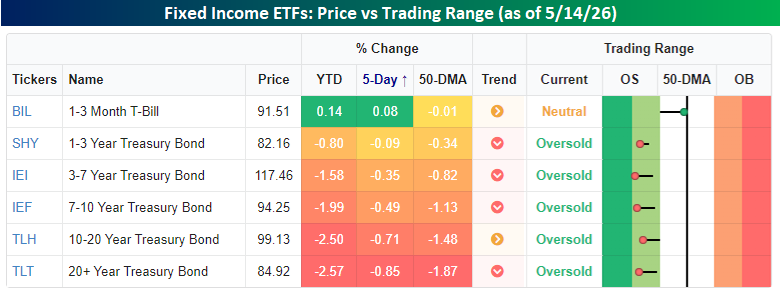

With inflation headlining the week’s economic data, and much of it surprising to the upside, yields have been an unavoidable and uncomfortable focus for investors. Almost across the entire yield curve, we’ve seen yields move higher this week, pushing the prices of the underlying bonds lower.

The snapshot of Treasury ETFs across the yield curve shows the story. Except for the shortest duration treasuries, prices have moved lower over the last five trading days (since last Thursday’s close), and the magnitude of the declines increases the further you go out on the curve. The magnitude of the declines hasn’t been extreme, but any treasury ETF with a duration of more than a year is currently oversold and will only get more oversold at the open today. YTD, it’s also been a year to forget, with declines nearly across the board.

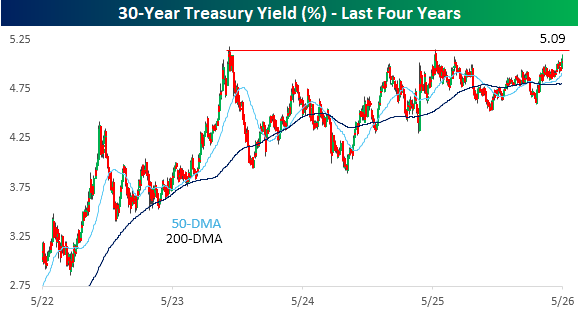

Of all the points on the yield curve, the 30-year is probably at the biggest crossroads. For nearly three years now, right above 5% has been a level the 30-year has flirted with multiple times, but each time it got there, the sellers didn’t have the firepower for a meaningful breakout. This week has been the third major test of that level as the yield pushes up towards 5.10% this morning. Will the third time be the charm or a strikeout?

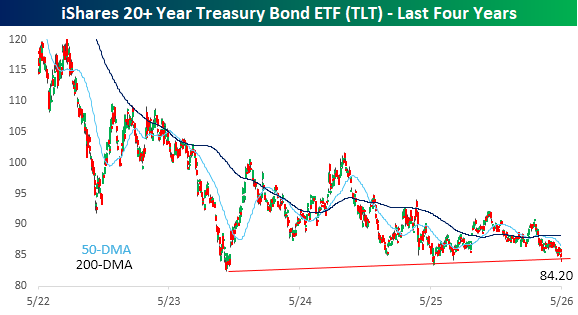

The iShares 20+ Year Treasury ETF (TLT) is the opposite of the 30-year yield. Prices plunged during 2022 and into early 2023 as the Fed hiked rates and inflation surged. As price pressures eased, yields and treasury prices stabilized, and while there was a rally off the 2023 lows into mid-2024, momentum quickly stalled out. Ever since then, prices have been stuck in the mid-80s, and this morning, TLT is trading down over 1% and testing support right around $84. It’s been a multi-year bear market for fixed income in the post-COVID era, and if these support levels don’t hold, the sector could be in store for a new leg lower.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.