See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The secret of life is to say yes all the time, because when you’re old, you don’t want to say, ‘I wish I’d done this, I wish I had done that.” – Francis Ford Coppola

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s been an up-and-down night and morning for equities. moving from negative to positive and back to negative levels. Barring any movement on the diplomatic front, it’s going to be hard for investors to take on much risk ahead of the President’s 8 PM deadline for Iran to reopen the Strait or face the wrath of the US military. At no time would a Taco Tuesday be more welcome than today, but the President has shown no signs of backing down. His latest Truth Social post comments from just a few minutes ago threaten that a “whole civilization will die tonight, never to be brought back again.” That is, unless “something revolutionary wonderful can happen”.

Besides the weakness in equity futures, Treasury yields are little changed, crude oil is up over 3%, gold is remarkably unchanged, and Bitcoin is down 2%.

Japanese stocks reopened from the long holiday weekend and finished the day effectively unchanged, while Hong Kong remained closed. Chinese stocks had marginal gains while South Korea and Australia were up close to 1% or more. With the Strait of Hormuz remaining closed, concerns have grown over the availability of not just energy, but also helium supplies for South Korea’s chip industry. Officials announced last night, though, that the country’s chip assemblers have secured supplies of at least four months.

In Europe, we’re seeing a modestly positive start to the week after the four-day weekend. Service sector PMIs for the continent declined slightly less than expected, while it was a mixed bag at the individual country level. France and Italy are leading in early trading with gains of about 0.5%, while Germany is unchanged.

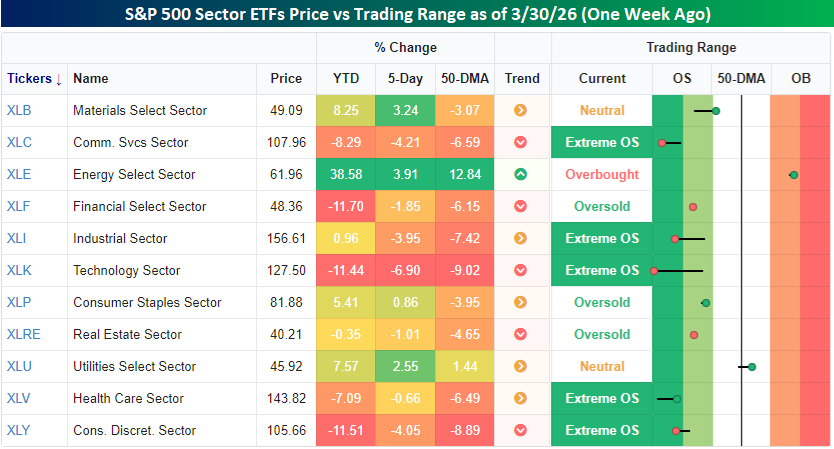

US stocks have made a nice comeback over the last year, moving from an environment where most sectors were either oversold or extremely oversold to one where most sectors are back to neutral. Starting with where things stood last week at this time, most sectors had declined over the prior week with several, like Technology, Communication Services, and Consumer Discretionary, experiencing declines of more than 4%. Those declines also put all three sectors into extreme oversold territory along with Industrials and Health Care. The only sectors above their 50-DMAs were Energy (which was overbought) and Utilities.

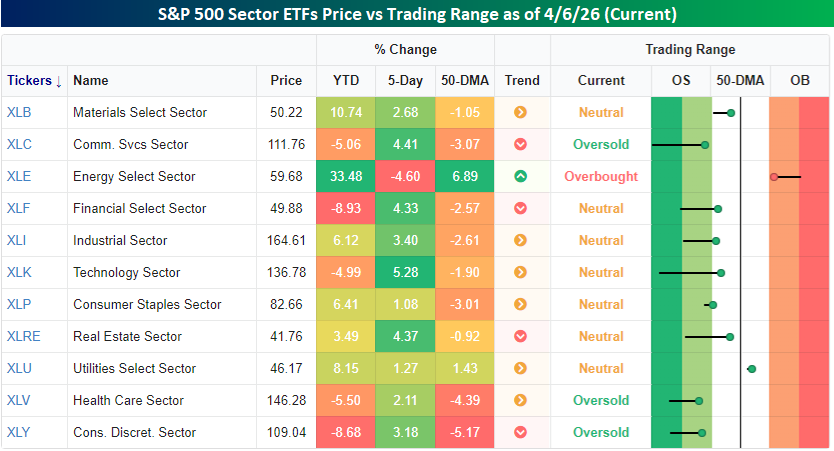

With the S&P 500 up four days in a row since the snapshot above was taken, we’ve seen a mass exodus out of oversold territory. The only sector down over the last week is Energy, while every other sector is up at least 1%, including four with gains of more than 4%. While three sectors – Communication Services, Health Care, and Consumer Discretionary – remain in oversold territory, they’re all close to moving out. That said, Energy and Utilities are still the only two sectors above their 50-DMAs, so there’s still plenty of room for improvement.

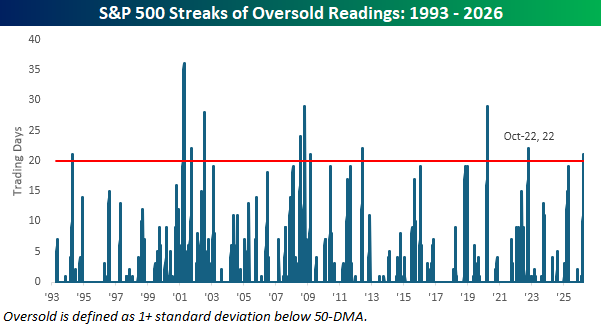

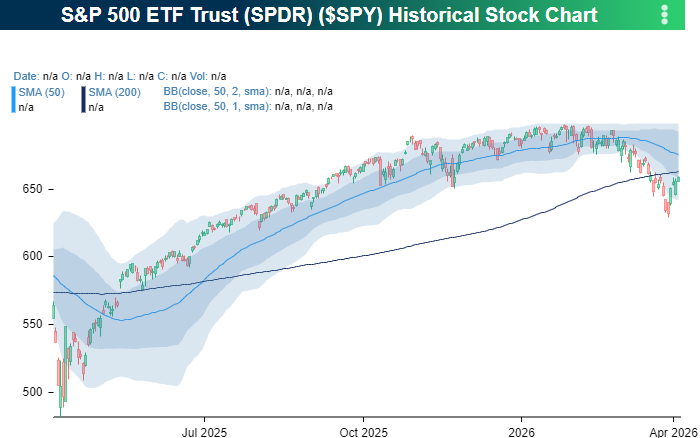

Like most sectors, the S&P 500 also managed to move out of oversold territory yesterday (light blue shaded region), an area it has been in since early March.

In fact, yesterday’s rally ended a streak of 21 trading days where SPY closed in oversold territory. That was the longest streak since the one that ended the bear market in October 2022, and it was only one of eleven streaks in SPY’s history since 1993 that lasted four weeks or more. The longest of these streaks was 36 trading days ending in April 2001, and eight lasted longer than 21 days.