See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“People generally see what they look for, and hear what they listen for.” – Harper Lee

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Sentiment surrounding AI is really something these days. On one day, you can have stocks surging on the idea that companies can’t get their hands on enough compute, and then the next day, they sell off sharply because there’s not enough demand. It’s like the line from The Rime of the Ancient Mariner, “Water, water, everywhere/Nor any drop to drink”. This morning, the Nasdaq is leading futures lower on a report in the Wall Street Journal that OpenAI missed year-end user and revenue targets, raising questions over whether all of the investments in the sector will eventually pay off. These are legitimate questions to ask, but if the article is based on year-end 2025 targets, a lot has changed between now and then regarding OpenAI’s growth (Codex) and the sector.

Nasdaq futures are currently down more than 1% while the S&P 500 is indicated 0.65% lower, while oil prices have surged more than 5%, taking WTI back above $100 per barrel. The impact of that increase in oil prices can’t be overstated either. While oil prices surge, gold prices are sharply lower (-2.6%), while Bitcoin is down less than 1%.

In Asia, stocks were mostly lower, with South Korea being the only exception (+0.4%). Japan and Hong Kong were both down 1% while China declined only 0.2%. The BoJ left its policy rate unchanged, but it was a fractured vote with three of nine voters pushing for a rate hike.

In Europe, it’s a mixed picture. With much less tech exposure than the US, the STOXX 600 is unchanged on the session while Italy leads the way higher (+0.9%) and Germany lags (-0.2%).

In the US today, it’s a relatively quiet day for data with the FHFA House Price Index at 9:00, and the Richmond Fed and Consumer Confidence reports for April hitting the tape at 10 AM.

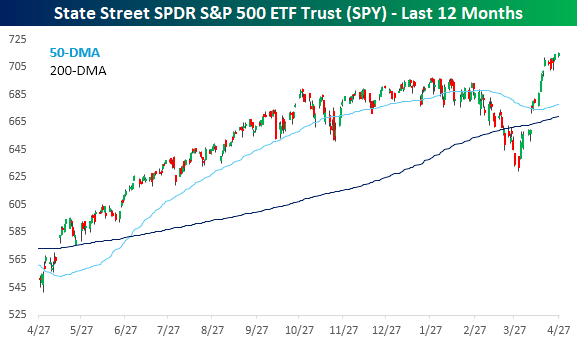

The S&P 500 hit both a new intraday and a closing high yesterday as the bull market continues to reconfirm itself with six closing record highs since 4/15. The index has had a parabolic run this month, and while a pullback or consolidation wouldn’t surprise anyone, the index should find decent support at the prior highs from late last year/early this year.

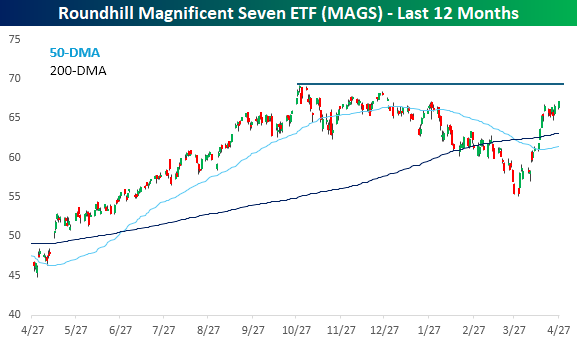

Over the last several years, whenever the market hits new highs, we look to see what’s driving the move higher. Is it the mega-caps or the rest of the index? Starting with the mega-caps, it’s been a strong month for the group, and while the group rallied nearly 1% yesterday to provide some positive momentum, it remains well below its prior all-time highs from last fall. At yesterday’s close of $67.08, the MAG7 ETF (MAGS) is still nearly 3% below its prior peak.

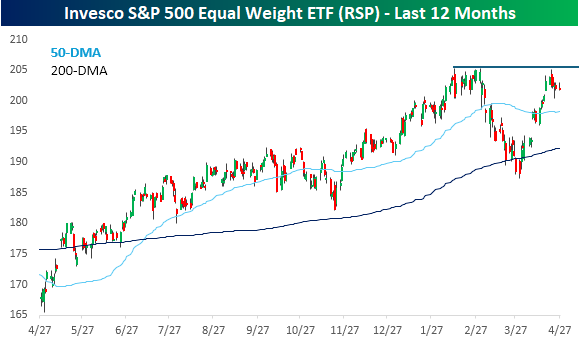

The equal-weight S&P 500, which more accurately reflects the performance of the “S&P 493”, traded down fractionally yesterday, so while it didn’t contribute at all to yesterday’s rally, it is actually much closer to all-time highs than the MAG7 ETF. In any event, though, it’s interesting to see that both the S&P 500 Equalweight and the MAG7 ETF closed more than 1% below all-time highs yesterday, even as the index itself hit a new one.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.