See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Power resides where men believe it resides. It’s a trick. A shadow on the wall.” — Lord Varys, Game of Thrones

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As if a 12-day rally wasn’t enough for bulls, Nasdaq futures are indicated higher again this morning, putting the index on pace for its 13th day in a row of gains. Both the Nasdaq and S&P 500 are on pace to rally 0.40% while futures on the Dow, which has underperformed recently, indicate a 0.54% gain at the open. The 10-year yield is slightly lower and holding below 4.3% while crude oil flirts with $90 to the downside, falling more than 4%. Gold prices are modestly higher with a gain of 0.34%, while Bitcoin rallies nearly 1% to its highest level since early February.

For much of this year, investors had to put up with weakness heading into the weekend, given all the uncertainty surrounding the war. For the last two weeks, though, investors haven’t been able to resist adding exposure heading into a 48-hour break.

International markets have been more mixed to close out the week, but are still higher for the week. The Nikkei fell 1.8% overnight while Hong Kong, China, and South Korea were all down less than 1%. In Europe, the STOXX 600 is marginally gaining 0.1%, with Italy leading the way (+0.6%) while the UK lags (-0.4%).

Just over two weeks ago, on March 30, the S&P 500 and the Nasdaq closed at their lowest levels since the summer, the Iran war was ongoing, and while Iran’s capabilities were severely damaged, the New York Times warned of a quagmire, saying that “Wounded Iran Is Still Biting: Attacks May Be Fewer But Have Deadly Effect”. Besides all that, it was a Monday too!

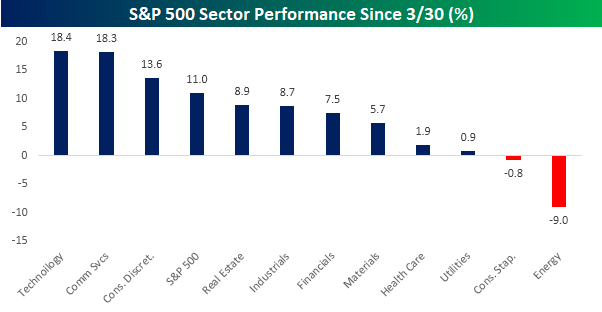

At the time, very few probably anticipated what was in store next for the market. Since that low, the Nasdaq hasn’t closed lower on a single day, and the S&P 500 has rallied in eleven of the last 12 days for a total gain of 11.0%. At the sector level, the rally hasn’t been especially broad, and gains have been concentrated in Technology and Communication Services, which both have surged more than 18%. The only sector that has outperformed the S&P 500 since that low is Consumer Discretionary (+13.6%).

To the downside, Energy has been the main loser with a decline of 9.0%, and the only other sector in the red has been Consumer Staples (-0.8%). As we noted earlier in the week, Consumer Staples is the only sector in the S&P 500 that declined both in the first month of the war from 2/27 to 3/30 and since the 3/30 low.

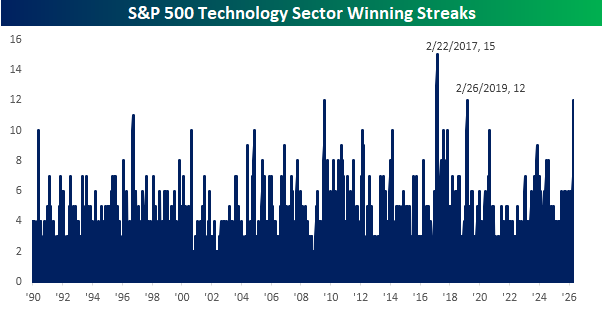

Technology has been the clear leader over the last 12 trading days, and relative to its own history, it’s been an impressive streak. The current streak for the sector is tied with the period ending 2/26/19 for the longest since February 2017. That 15-day winning streak was also the longest in the sector’s history since 1990.

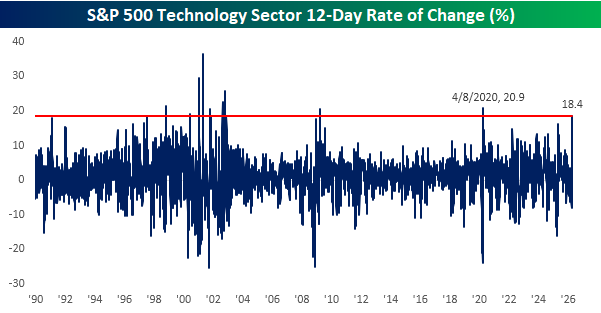

Not only has the sector’s winning streak been among the sector’s best, but the 18.4% rally over the last 12 trading days has been among the strongest since 1990 as well. You have to go back to April 2020, coming out of Covid to find a bigger 12-day rally (+20.9%), and before that, the only larger 12-day gain was in March 2009 coming out of the Financial Crisis. To be sure, not all big 12-day gains for the Technology sector were followed by gains going forward, but the sector’s median gain over the following six and twelve months was 13.8% and 28.1%, respectively.

Start a two-week trial to Bespoke Premium to continue reading today’s full Morning Lineup.