See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In wartime, truth is so precious that she should always be attended by a bodyguard of lies.” – Winston Churchill

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s been an up-and-down overnight session for US equity indices, and as we type this now, both the S&P 500 and Nasdaq futures are basically flat with moves of less than 10 bps to the upside. Treasury yields are slightly higher, crude oil is flat, and gold is up less than 1%. Pretty quiet day, huh?

Iran will have the potential to continue dominating market action for the day, but don’t forget about the ADP Employment report, ISM Services, and then Broadcom (AVGO) earnings after the close. Earlier this week, the ISM Manufacturing report had the highest Prices Paid reading since 2022, so that will be a key metric to watch in today’s report for the services sector.

The bottom fell out of Asian stocks overnight as the Nikkei fell 3.6%, and every other major benchmark index in the region fell at least 1%. The real damage, though, was in South Korea, where the KOSPI fell over 12% for its worst day on record. There have been major market panics over the last 40 to 50 years, but none of them featured a day when South Korean stocks had a worse one-day decline. Fallout from the war in Iran was the primary driver of the declines, but Chinese PMI data for the Manufacturing and Services sectors also came in weaker than expected.

European stocks are following a different path than Asia, as the STOXX 600 is up over 1%, and the only major country up by less than 1% is the UK. Spanish stocks have managed a gain of 1.4% despite threats from the Trump Administration to cut off trade with the country. Service sector PMIs for the Eurozone and individual countries were basically in line with or slightly better than expected.

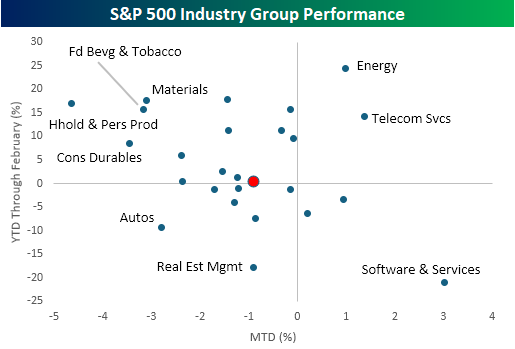

After two full sessions of trading since the war in Iran started, the overall market reaction has been subdued, but there have been some larger moves among individual industry groups. While the S&P 500 is down less than 1%, 16 out of 25 industry groups are up or down more than 1%.

This morning, we wanted to focus on some of the extremes. Starting with the winners that have continued winning, the only two groups that were up YTD heading into the conflict and have continued higher since are Energy and Telecom Services. Along with those two groups, the only others that are up this week are Software & Services (3.0%), which took the opposite path of South Korea by going from worst to first, Commercial Services (0.9%), and Banks (0.2%).

To the downside, some of the worst-performing sectors this week were some of the best YTD performers heading into the conflict. Household & Personal Products, Food Beverages & Tobacco, and Materials were all up over 15% YTD heading into the week, and they’re all down over 3% this week. As painful as the declines may feel this week, they’re coming off of a high base. It’s also worth noting that while Software stocks have bounced, Autos and Real Estate Management- the second and third worst performing groups YTD heading into the conflict have continued lower.

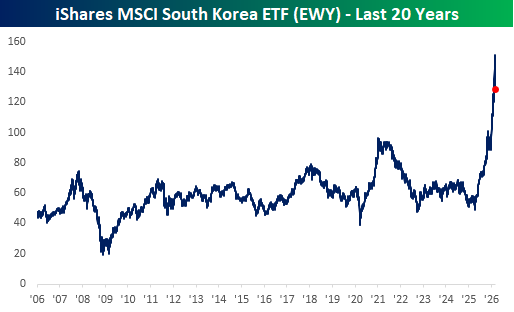

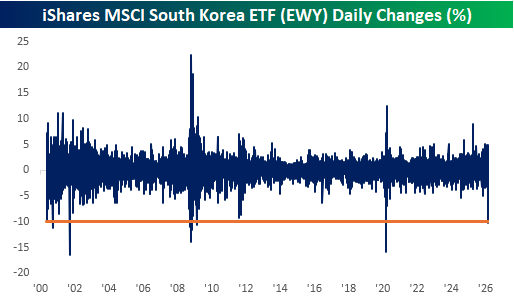

Outside of the US, we’ve also seen some major reversals this week. In yesterday’s Chart of the Day, we noted the outperformance of US stocks relative to the rest of the world. Nowhere has this reversal been more evident than in the performance of South Korean stocks. On Monday, the iShares MSCI South Korea ETF (EWY) fell more than 10% for its largest one-day decline since the Covid crash (South Korea’s KOSPI last night had its worst day on record). As shown in the chart below, declines of this magnitude have only been seen during periods of major crises like Covid, the Financial Crisis, and the dotcom bust.

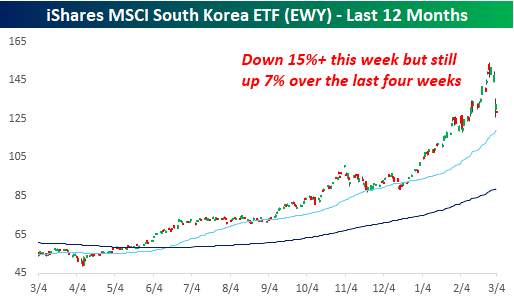

Besides Monday’s decline, EWY continued lower yesterday and is indicated down by another 3% this morning. That takes its decline this week to over 15%, and as sharp as that may sound, the ETF is still up over 7% in the last four weeks. It’s been a rocky few sessions, but if someone told you four weeks ago that you’d have a 7% gain in a month despite a major war in the Middle East, who wouldn’t have signed up for that?

From a longer-term perspective, EWY still looks extremely extended relative to its historical range. After breaking out above its 2021 highs late last year, it is still up over 32% YTD, making it the top-performing major country ETF, so it’s hardly oversold.