See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If my answers frighten you then you should cease asking scary questions.” – Quentin Tarantino

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s another one of those days where futures drift lower throughout the morning as traders follow the new daily routine of getting up, brushing their teeth, and clicking “Sell”. At 5 AM on the East Coast, when most of us were still asleep, futures were flat to marginally higher, but they have steadily lost steam all morning, and the S&P 500 is on pace to gap down 0.4%, while the Nasdaq is down 0.6%. Barring a major reversal during the trading day, the Nasdaq is poised for its 10th down week in the last 11. That consistency to the downside has only been seen in a handful of other periods throughout the index’s history.

Treasury yields are higher, with the 10-year yield up 4 bps to 4.46%, and WTI crude oil is up another 2.5% to just under $97 per barrel. That increase comes after President Trump said he would extend the deadline for Iran to open the Strait of Hormuz by 10-days because talks were “going very well”. While that looks bullish on the surface, it’s been taken as either a sign that the President is just buying more time to launch a ground invasion, or that talks are not going anywhere and the President is just stalling. The reality is that only a handful of people really do know, so investors are using the uncertainty as an excuse to sit things out.

On a more positive note, it looks like the government shutdown will end today, which should alleviate some of the pressure at US airports. Isn’t it ironic that after more than 40 days without paying TSA employees and subjecting people across the country to airport delays, Congress finally reached an agreement just in time for their two-week vacation? The idea that members of Congress are ‘public servants’ is starting to feel like the ultimate oxymoron; unless, of course, the public they’re serving is just each other.

In Asia overnight, most major equity benchmarks were lower on the session, although Hong Kong and China managed fractional gains. Outside of Australia, though, every other equity market was down for the week. In Europe, it’s much weaker with the STOXX 600 down 1.4%, putting it into the red for the week, and most individual country indices are down at least 1% on the day.

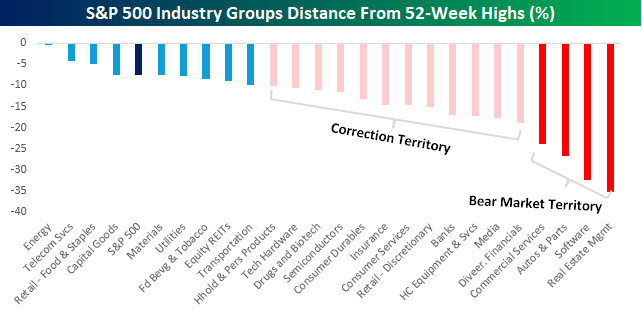

With yesterday’s decline, the S&P 500 is now down 7.5% from its intraday high earlier this year, putting it increasingly closer to correction territory. Of the 25 industry groups within the index, 16 closed at least 10% below their respective 52-week highs (on an intraday basis), and four of those are down at least 20%, putting them in bear market territory based on the 20% definition. Leading the way down, Real Estate Management has lost more than 35% of its value, but the most painful of the declines, given its weighting in the index, is Software, which is down by nearly a third.

On the positive, or less negative side, three groups closed within 5% of their respective highs yesterday, with the most obvious being Energy.

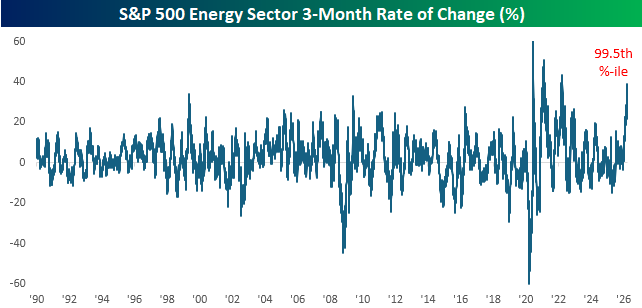

The rally in the Energy sector has reached historic proportions in the last few weeks. Over the last three months, the sector has rallied more than 38%, which ranks in the 99.5th percentile compared to all other periods since 1990. As shown in the chart below, the only times it experienced a larger rally were coming out of Covid and early in the Russia-Ukraine war.

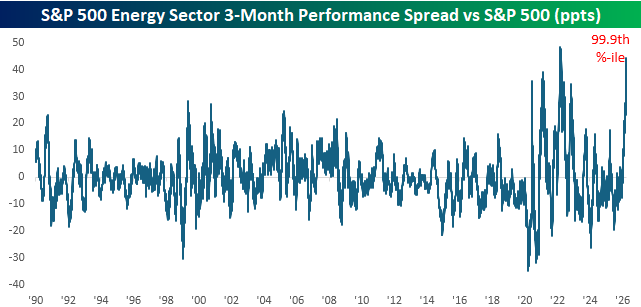

What’s even more impressive about the sector’s rally is that it came as the overall market declined. With the S&P 500 down over 6% in the last three months, the 44.4 percentage point performance spread between the two has only been wider for a brief period in March 2022. Outperformance of this magnitude on the part of the Energy sector is nearly unprecedented.