See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When we have computers that can do more and more jobs, it’s going to change how we think about work. There’s no way around that. You can’t wish it away.” – Larry Page

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There’s no joy in Marketville this morning as investors step up to the place for the opening bell. Nasdaq futures are down nearly 1% while the S&P 500 faces a gap down of 0.75% at the open. Treasury yields are higher across the curve, WTO and Brent crude oil are both up over 4%, gold is down 2.5%, and Bitcoin is down over 2%. Fun morning for the bulls!

With the five-day deadline imposed by the President, Monday fast approaching, and no signs of a diplomatic breakthrough, investors have no incentive to make a stand, and that doesn’t even take into account the government shutdown snarling air traffic. Maybe the only good news is jobless claims. Initial claims came in right inline with expectations, while continuing claims were well below forecasts, falling to a nearly two-year low.

In Asia, stocks reflected the pessimism as the Nikkei fell 0.3%, China declined 1.1%, and South Korea dropped the most, falling 3.2%. European stocks are doing no better. The STOXX 600 is down 1.0% halfway into the session, led lower by Germany and the UK, which are both down over 1.25%. ECB council member and Bundesbank President Joachim Nagel even noted that a rate hike in April is “certainly an option”.

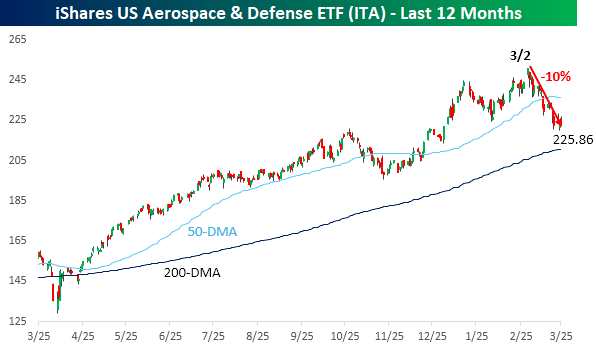

We’re now a month into the war in Iran, where every day’s news has shown images of precise strikes against the Iranian military. With all those weapons, it must be great for the defense contractors, right? Ironically, while aerospace and defense stocks performed well over the last year, they’ve seen a sell-the-news reaction since the war started. As shown in the chart of the iShares Aerospace & Defense ETF (ITA) below, the sector peaked on the first trading day after the first missiles were launched and has declined 10% since. That’s worse than the S&P 500!

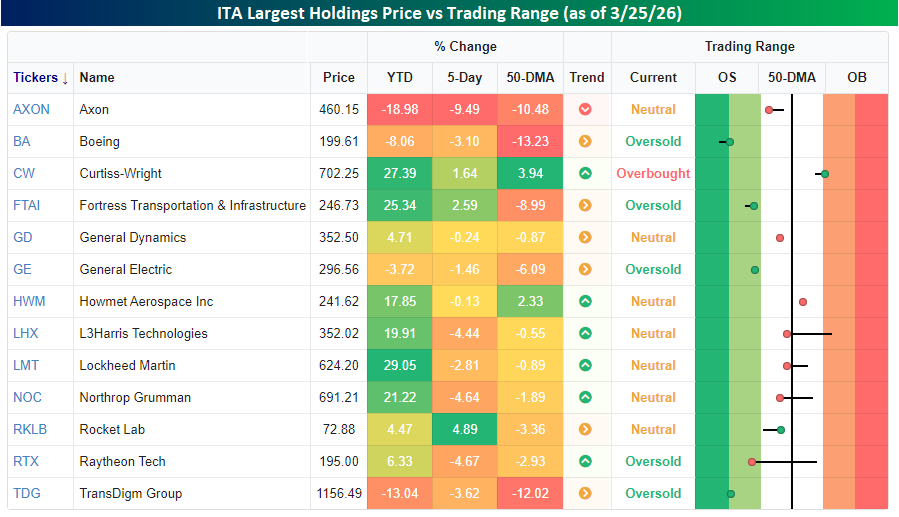

Looking through a list of ITA’s 13 largest holdings (all greater than 2% weighting), performance this year has mostly been positive. Nine of the thirteen stocks are up YTD, with an average YTD gain of just under 9%. Like the ETF, though, most of the largest holdings are below their 50-DMAs. In total, their average 50-DMA spread is -4.2%, and they’re down an average of 2% in the last five trading days.

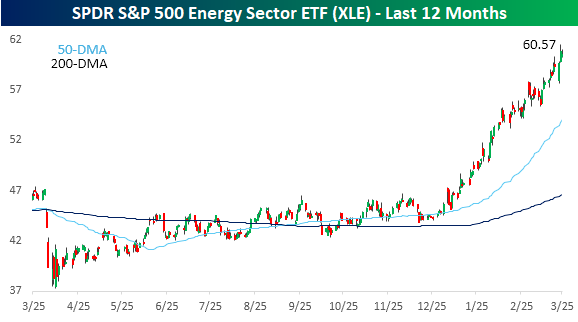

While defense stocks have struggled this month, Energy stocks have been on fire. The SPDR S&P 500 ETF (XLE) started to go parabolic at the turn of the calendar and hasn’t looked back since.

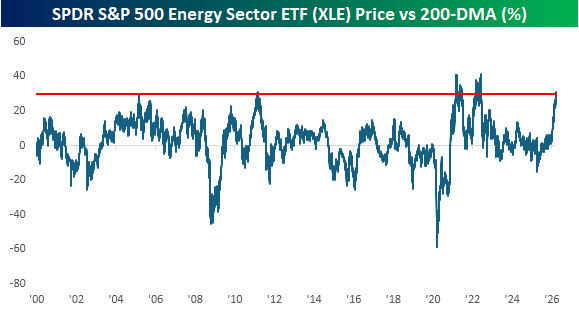

The rally in the sector has been so strong that the spread between XLE’s price and 200-DMA exceeded 30% this week. Since the ETF’s inception in 1999, there have only been a few other periods where the spread exceeded 30%. The most recent was early in the Russia-Ukraine war, and before that, the only other occurrences were in the first half of 2021 as the economy reopened from Covid and then briefly in early 2011 when oil prices spiked due to the Arab Spring and a civil war in Libya.