See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It’s the rough side of the mountain that’s the easiest to climb; the smooth side doesn’t have anything for you to hang on to.” – Aretha Franklin

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on Fox Business yesterday. To view the segment, click on the image below.

Global equity markets are in rally mode this morning after reports of potential negotiations between the US and Iran to end the war. Asian markets surged overnight, and that flowed into the European open and US futures this morning. Some of the air has come out of the balloon as we type this, though, on reports that Iranian officials have rejected the US terms delivered via Pakistan. There’s really no way to know at this point what the facts are regarding the state of negotiations, as neither side has any real incentive to conduct talks via the press, so expect more whipsaw action as things continue to progress. The bottom line is that while Iran still holds some cards, the chips are stacked heavily against them.

Outside of equities, the 10-year yield is down 5 bps, crude oil is down 5%, gold is up nearly 4%, and Bitcoin is up 2.5% to more than $71K.

In economic data, the only report on the calendar was Import Prices, which came in at more than double expectations (1.3% m/m vs 0.6%). If you’re looking for lower rates or a dovish Fed, these are not pretty numbers.

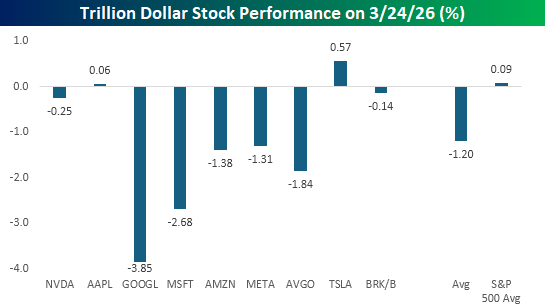

The S&P 500 finished down 0.37% yesterday, but most of the losses were focused in the trillion-dollar stock club, where the damage was much more concentrated. While the ‘average’ stock in the S&P 500 traded slightly higher yesterday, seven of the nine stocks in the trillion-dollar club traded lower, with an average of 1.2%. Stocks like Alphabet (GOOGL) and Microsoft (MSFT) were notably weak with declines of more than 2.5%, and both closed at multi-month lows. Other mega-caps like Broadcom (AVGO), Amazon.com (AMZN), and Meta Platforms (META) all fell more than 1%. The only mega-caps to buck the trillion-dollar market cap weight were Tesla (TSLA) and Apple (AAPL), which saw modest gains.

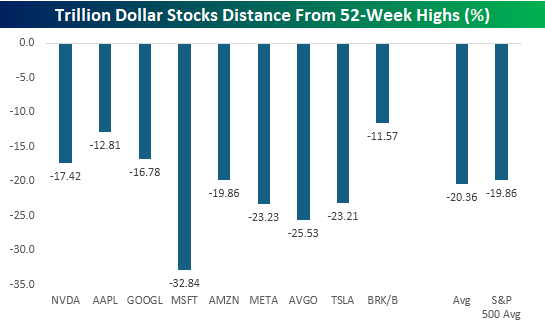

While the trillion-dollar stocks have been market leaders, they’re no longer the cool-kids table in the lunchroom. For months, they stood out above the rest of the market as the most popular in terms of where they were trading relative to 52-week highs, but now they no longer stand out. MSFT, AVGO, META, and TSLA are all down more than 20% from their respective 52-week highs, and the average drawdown from their peaks is just over 20%. That’s flirting with bear market territory and slightly more than the average 19.9% drawdown for all 500 stocks in the S&P 500.

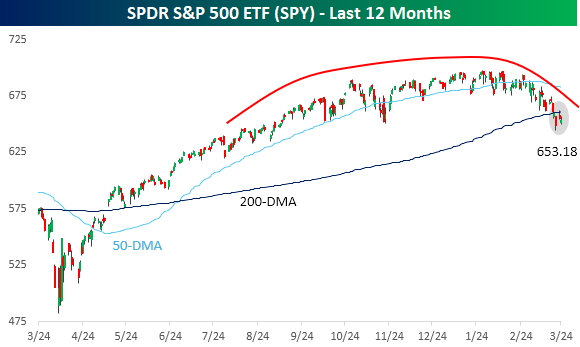

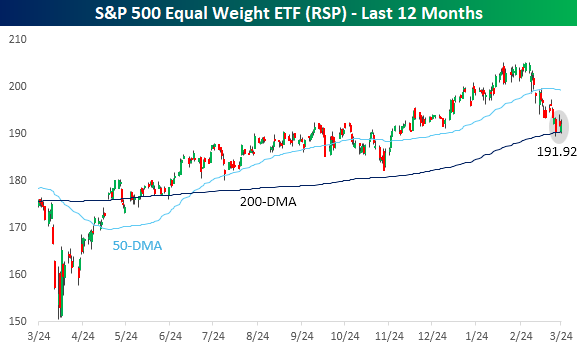

The cap-weighted S&P 500 (SPY) closed down just over 4% for the year yesterday, while the equal-weight version (RSP) is still slightly higher on the year (+0.2%), and their charts have two key differences.

First, as we’re all aware, the cap-weighted S&P 500 has been stuck in a sideways range for several months, forming a gradually curving, rounded top which accelerated when the war started at the turn of the month. The topping process for RSP was much sharper. From the start of the year right up until late February, RSP was steadily making new highs. Once the war broke out, though, the rally was stopped in its tracks, erasing two months’ worth of gains in less than a month.

Second, with RSP still holding on to gains for the year, it has also stayed above its 200-DMA. The same can’t be said for the S&P 500, which broke that level last Thursday. For now, bulls can rationalize SPY’s break of the 200-DMA by pointing to RSP still hanging on to that level. If both indices break that long-term average, though, bulls will have one less arrow in their quiver.