See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I don’t trust society to protect us, I have no intention of placing my fate in the hands of men whose only qualification is that they managed to con a block of people to vote for them.” – Mario Puzo, The Godfather

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be on Making Money With Charles Payne today on Fox Business between 2 PM and 3 PM to discuss markets and the latest events in Iran. Check it out if you can!

Equity futures have been ping-ponging between gains and losses since the close yesterday, and they’re now on the red side of the table. Futures on the S&P 500 and Nasdaq are both down 0.1%. The 10-year yield has moved back to 4.36%, gaining 3 basis points. Oil prices moved back above $90 as investors try to figure out how things will play out in Iran. Good luck with that! Gold and other precious metals have seen muted moves this morning, with gains or losses of 1%, while Bitcoin has a fractional gain of 0.5%, taking it back above $71K.

It’s a relatively busy day for data this morning with Non-Farm Productivity and Unit Labor Costs at 8:30, but both reports are stale given the war situation. Investors will probably focus more attention on flash PMIs for March from S&P at 9:45 and the Richmond Fed at 10 AM. All of these reports will take a backseat to whatever geopolitical headlines or “truths” hit the tape.

European stocks were still open for trading yesterday when President Trump made his comments regarding Iran. Therefore, they had the opportunity to adjust, but this morning they’re adding modestly to those gains with the STOXX 600 up 0.3%. Flash PMI readings for March were also released. While manufacturing indices were better than expected, service sector PMIs generally missed.

Asian stocks played catch-up and followed the US lead overnight with gains across the board. Japan was up 1.4% while China rallied nearly 2%, and the Kospi gained 2.7%. The gains weren’t steady, though. In South Korea, for example, the KOSPI started the day with a gain of more than 4% but gave back all those gains early in the session and briefly traded lower before rebounding in the second half of the session. Inflation data in the region was on the light side as Japanese CPI and South Korean PPI for February both rose less than expected. While the lower inflation data was welcome, flash PMIs for Australia and India were both lighter than expected.

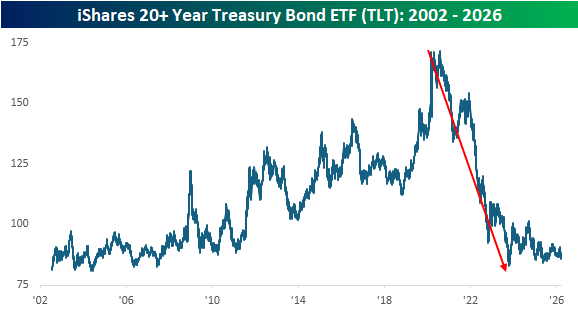

After falling more than 50% in price terms from its closing high in August 2020 to its low in October 2023, long-term US Treasuries, as proxied by the iShares 20+ Year US Treasury ETF (TLT), remain in the back half of a lost decade. As shown in the chart below, while prices remain near their multi-year lows, they have stopped going down, and with the long end of the curve yielding close to 5%, a flat market in price terms isn’t so bad.

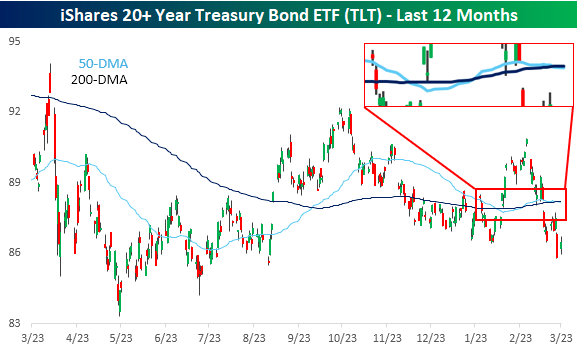

Looking at a one-year chart of TLT shows an interesting pattern. We’ve discussed the nowhere direction of the equity markets and some notable stocks like Nvidia (NVDA) extensively over the last several weeks, but the treasury market has also been comatose. Look at TLT’s 50 and 200-day moving averages (zoomed in on the inlay). Over the last several weeks, the two have moved in lockstep.

The two moving averages have been moving in such unison that yesterday was the 36th straight trading day the spread between the two was less than 25 basis points. Looking back at the ETF’s history over the last 20+ years, this current streak ranks as the longest in its history. It’s longer than the next closest one by more than two weeks! With the current spread between the two at less than 4 bps, it doesn’t appear likely to widen out to more than 25 bps any time soon!