See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you don’t understand what the professor is saying, don’t dismiss the possibility that he might be wrong.” – Paul Volcker

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

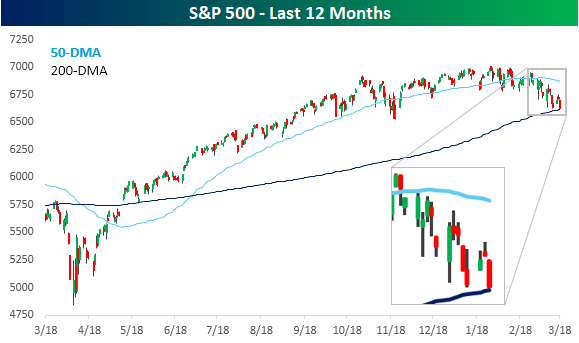

After a relatively strong start to the week, where it looked like the market would be able to look past the spike higher in energy prices, continued tensions in the Middle East and the stubbornly high level of crude oil prices have pushed the S&P 500 back into the red for the week, with further downside in store for today. S&P 500 futures are trading down 0.4%, which would put the S&P 500 below its 200-day moving average (DMA). The Nasdaq, which already closed below its 200-DMA yesterday, is expected to add to that breakdown with a decline of 0.5%.

International markets had a terrible night, with most major averages in the region down at least 2% and in most cases much more. That’s the same trend in Europe as well, with the STOXX 600 down over 2%, as is the case with most indices in the region.

As we’ve been pointing out all along, the declines are all about energy prices, and this morning, they’re not helping out as WTI trades up 2% to more than $98 per barrel, while Brent trades up by nearly 7% to $115 per barrel. The spread between Brent and WTI is now a monstrously high $16+ per barrel.

Treasury yields are moving higher as investors fear the inflationary impacts of rising energy prices, and the 10-year yield is now testing 4.3%. Gold prices are plunging more than 5% to under $4,700 per ounce, and Bitcoin is back below $70K.

The economic calendar is relatively busy this morning with jobless claims and Philly Fed at 8:30, while New Home Sales and Wholesale Inventories will hit the tape at 10 AM. Jobless claims came in lower than expected on an initial basis but slightly higher than expected on a continuing basis, while the Philly Fed was actually better than expected. With everything going on in the Middle East, though, the data is basically meaningless.

As the quote of the day notes, in many aspects of life, change has a way of happening slowly and then all at once. For months, the S&P 500 has been trading in a sideways range, consolidating the gains from the April lows. Then, all of the sudden we have a day like yesterday where the S&P 500 sells off a not necessarily dramatic 1.4%, but then all of the sudden, we’re looking at an S&P 500 whose 50-day moving average (DMA) has just started to slope downward just as the index is on the verge of trading below its 200-DMA for the first time since last spring. Steady uptrend to sideways range and now a potential downtrend? Change happens slowly until it doesn’t.

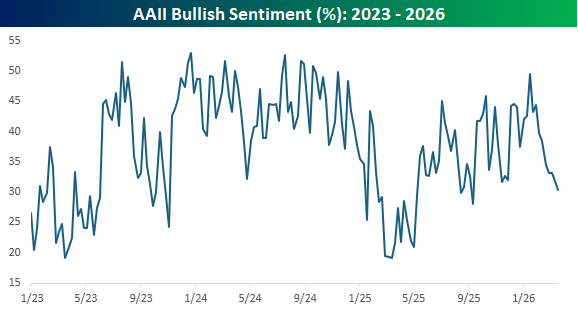

With the S&P 500 slowly (and now more suddenly) trending lower, investor sentiment has also been on the decline. In the latest survey from the American Association of Individual Investors (AAII), bullish sentiment declined from an already low level of 31.9% to 30.4%, which is the lowest level since last September, as the uptrend in sentiment since the lows early last year has been firmly broken.

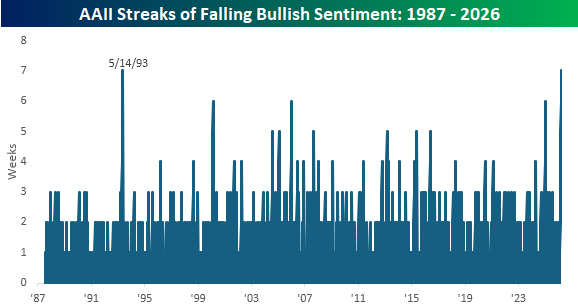

With this week’s decline, bullish sentiment has now declined for a record seven straight weeks. That’s now tied with the seven-week streak from May 1993 for the longest weekly losing streak in the survey’s history. Behind these two streaks, there were three others (Feb 2000, Jan 06, and Jan 2025) that lasted six weeks. Based on how the market traded yesterday, if we don’t see an improvement in the next couple of days, we would expect that this current streak could move into first place all on its own.