See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The way we do things is to begin.” – Horace Greeley

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Make sure to check out Paul Hickey on CNBC’s Squawk on the Street today at 10 AM!

Futures on the S&P 500 and Nasdaq are slightly higher this morning, as the Dow trades slightly lower. Nasdaq futures are leading the gains following a positive earnings report from Palantir (PLTR), which has the stock trading up over 10%. Treasury yields are moving higher again as the 10-year yield sits just under 4.29%, and crude oil is slightly higher. Precious metals are really in rally mode as Gold trades up over 6% and Silver is up more than twice that in percentage terms. If you were looking for things to calm down in that space, don’t hold your breath.

The only economic report on the calendar this morning is JOLTS at 10 AM, but right before that, at 9:40, Fed Governor Bowman will be speaking at a WSJ conference. On the earnings front, some of the key companies reporting after the close will be AMD, Amgen (AMGN), and Mondelez (MDLZ)

So much for that sell-off in Asian stocks to start the week. Overnight, the Nikkei surged nearly 4% to a new all-time high. Not to be outdone, the KOSPI spiked nearly 7% briefly causing another halt to trading, after Monday’s downside halt. Both Palantir’s (PLTR) positive reaction to earnings and the US India trade deal have acted as catalysts for the gains. India’s Sensex also rose over 2.5% in the wake of the trade deal, which would cut tariffs on Indian imports to 18%, and India would agree to stop buying Russian oil. All of this news overshadowed a rate hike in Australia from the RBA, which was widely expected, but the central bank did suggest tighter policy could continue as inflation accelerates.

Yesterday, it was Europe benefiting from its lack of technology exposure, but this morning, that isn’t the case. While stocks in the region are generally positive on the session, the gains are much more muted relative to Asia. The STOXX 600 is barely holding on to gains while the UK and France are both in the red.

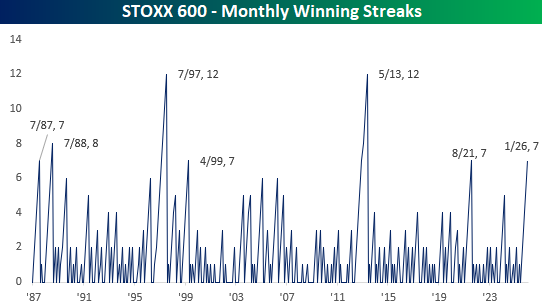

After two weeks of sideways trading, European stocks went into lift-off mode yesterday as the STOXX 600 surged more than 1% to a new all-time high. This morning, the European benchmark index added to those gains before pulling back modestly, although it’s still up for the day. YTD, the STOXX is already up over 4%, or more than twice the 1.9% gain for the S&P 500.

Like the Dow Jones, which has had nine months in a row of gains, the STOXX 600 has been up for seven straight months. That ranks as tied for the longest streak since May 2013 and tied for the fourth-longest on record.

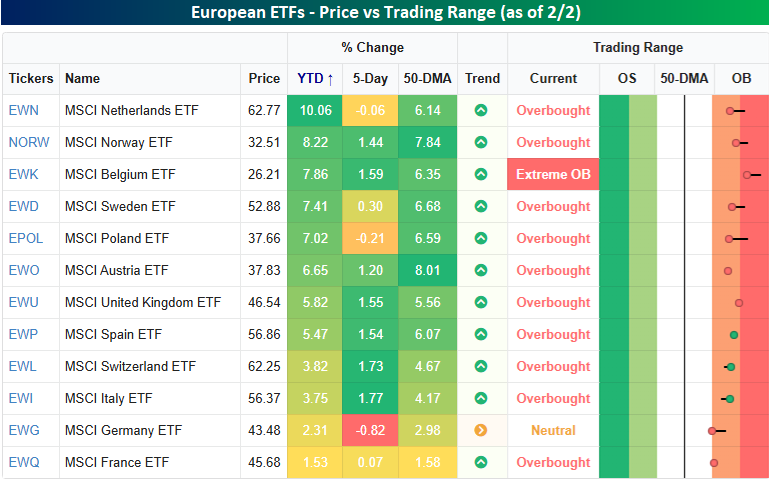

Looking at individual country performances within Europe, the snapshot below from our Trend Analyzer shows the performance of country ETFs on the continent. Of the 12 ETFs shown, all of them are up YTD, and France is the only one underperforming the S&P 500. Most of the countries have outperformed the US by a wide margin. The Netherlands (EWN) ETF is up over 10% already this year, and seven other countries have gained at least 5%. Most of the countries are also comfortably above their respective 50-day moving averages and well into short-term overbought territory. The only exception is Germany (EWG), which is also down the most over the last week (-0.82%).

It’s also interesting to note that most of the strength in European stocks this year hasn’t been coming from major economies like Germany, France, Italy, and Spain. They’re all at or near the bottom of the performance list. Instead, it’s the less talked about countries like the Netherlands, Norway, Belgium, and Sweden leading the way.