See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I wonder why progress looks so much like destruction.” – John Steinbeck

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey will be a guest on “Making Money with Charles Payne” today at 2 PM on Fox Business. Make sure to check it out!

Futures have been steadily losing steam all morning as the S&P 500 and Nasdaq both look to open down over 0.6%. Weakness has been focused on the usual suspects of software stocks, as Salesforce (CRM) drops 3% while Microsoft (MSFT) falls over 1%. A Disappointing earnings report from CoreWeave (CRWV) hasn’t helped either, as that stock is down over 10%. Nvidia (NVDA) is also adding to yesterday’s 5%+ decline with a drop of 1% in the pre-market.

With the weakness in equities, treasuries are rallying as the 10-year yield falls below 4% for the first time since before Thanksgiving. Oil prices are sharply higher with a gain of more than 3% heading into another weekend of uncertainty over whether the US will attack Iran. That uncertainty also has gold trading nearly 1% higher while other metals see even larger gains. Crypto, however, is down over 2% and back below $66K after trading above $69K two days ago.

Asian markets finished the week mixed but broadly higher for the week. South Korean stocks fell 1% but still gained 7.5% for the week and closed to 20% for February. Not bad for the shortest month of the year! Japan and China traded higher, adding to their gains for the week with Japan up 3.6% and China up 2.0%. Inflation data in Japan decelerated relative to January (1.8% y/y from 2.0%) but was higher than the 1.7% y/y consensus forecast. Japan’s economic minister took the glass-half-full view of the data and commented that inflation is slowing and expects real wages to turn positive in the coming months. In Europe, it’s been a modestly positive session in early trading with the STOXX 600 up 0.2%, putting it on pace for a 0.5% gain for the week. At the country level, markets are broadly higher on both the day and the week.

On the data front, January PPI just hit the tape and came in higher than expected for the second month in a row. Futures have dipped lower in reaction to the report, although the 10-year yield hasn’t moved much in reaction. The only other reports on the calendar between now and the weekend are the Chicago PMI at 9:45 and Construction Spending at 10 AM.

As mentioned above, with the 10-year yield below 4.0%, it is on pace for its first close below 4% since the day before Thanksgiving and the lowest close since late October. As shown in the chart below, if the current levels in the 10-year yield hold, today would be just the ninth time in the last 12 months that the yield closed below 4%. These levels come just over a month after yields were as high as 4.3%, as market fears over inflation outweighed any concerns over future employment losses due to AI. We also wouldn’t be surprised if, at some point in the coming weeks, the narrative shifts once again!

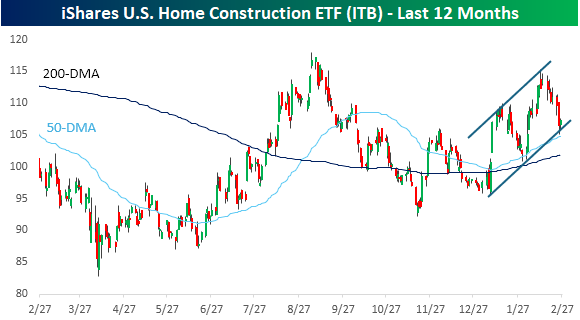

Prime beneficiaries of lower yields are the homebuilders, and up until this week, the group was performing very well, but on Wednesday, the iShares US Home Construction ETF (ITB) fell more than 3% following the President’s State of the Union (SOTU) speech. Usually, when a stock or sector falls after one of the President’s speeches, it’s because he said something combative about it. In this case, though, it was what the President didn’t say.

Despite being the longest SOTU speech of all time, the speech was noted for its lack of any meaningful comments regarding housing or increasing housing supply. In fact, the only real mention of housing was in protecting home prices, which can only be done by lowering demand or not meaningfully increasing supply.

While homebuilder stocks had their worst day in over six months the day after the President’s SOTU speech, ITB remains in a steady uptrend and bounced yesterday right at the bottom of that trend channel. If rates remain below 4%, a move back to the high end of that range wouldn’t be an unreasonable expectation.

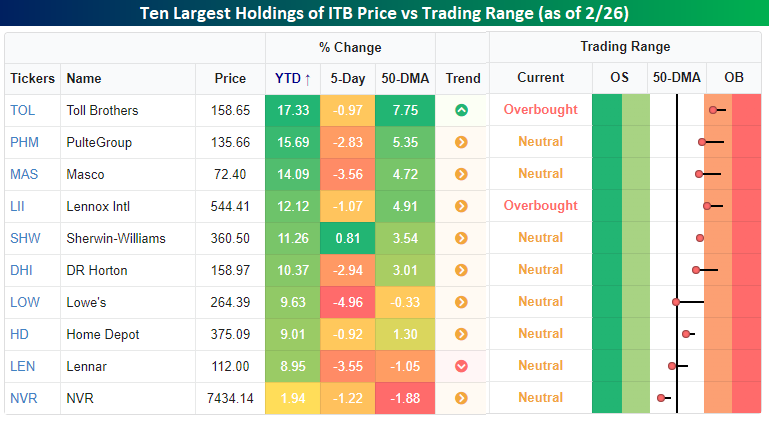

It’s been a good year all around for homebuilders and housing-related stocks. Of the ten largest holdings in ITB, all but one are up at least 8% YTD, even after this week’s declines. Pure-play homebuilders have led the ETF’s gains, with Toll Brothers (TOL) and PulteGroup (PHM) both rallying more than 15% YTD.