See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I don’t know what happened. It was just euphoria. I can’t even explain what I was feeling, just pure joy.” – Charlie McAvoy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After trading uniformly higher earlier, equity futures are mixed this morning, with the S&P 500 fractionally lower, while the Nasdaq is higher. Investors are still reeling from yesterday’s tech sell-off, as markets start to think that AI-disruption will negatively impact just about every business and sector. Treasury yields are little changed, but at 4.03%, the 10-year yield is near the low end of its range. Crude oil is modestly higher but still hovering around $66 per barrel, while gold is down over 1% and Bitcoin is down another 2% and barely hanging on to $63,000.

In Asia, Japan, South Korea, and China were all firmly higher as the latter returned from the Lunar New Year holiday, while India and Hong Kong were both down over 1%. In Europe, trading has been directionless in early trading with the STOXX up 0.2%, but at the country level, performance has varied between gains and losses.

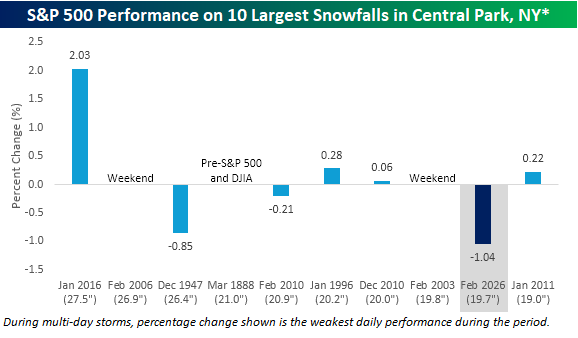

Let’s start with yesterday’s blizzard in the Northeast. With 19.7 inches of snow in New York’s Central Park, it was the ninth-largest snowfall in New York City history. While travel bans were in place around the New York tri-state area, the bears had no trouble getting to work. With the S&P 500 down 1.04%, it was the worst single-day performance for the S&P 500 during one of its ten-largest snowstorms on record. As shown in the chart below, during the prior top ten snowstorms for New York City, the weakest single-day performance during one of these snowstorms was a decline of 0.85% on 12/26/1947.

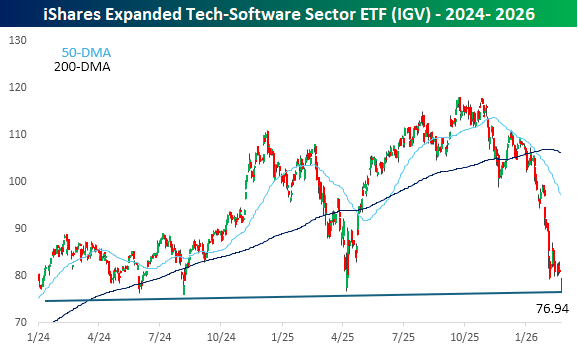

As it has been for some time, the software sector was responsible for much of yesterday’s weakness. The iShares Expanded Tech-Software Sector ETF (IGV) fell close to 5% and to its lowest level on an intraday basis since August 2024 as the lows from earlier this month broke like a hot knife through butter.

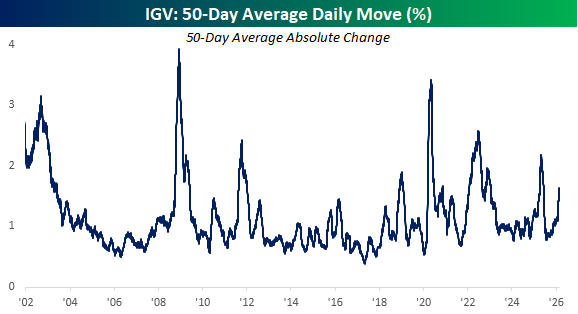

While software has been weak, it hasn’t necessarily been as volatile as you would expect. Over the last 50 trading days, IGV’s average daily change has been a gain or loss of 1.6%. While that’s elevated, it’s hardly anywhere near a historical extreme. Even in early 2025, the average daily change was much higher at over 2%.

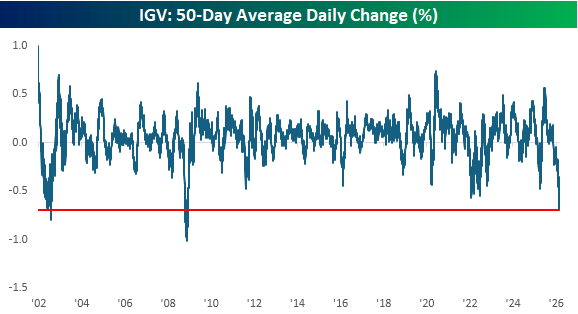

Where the moves in IGV have been extreme, though, is in terms of the average daily percentage change (not the absolute daily change but the average of the trailing 50-day changes). As of yesterday’s close, IGV’s average daily change was a decline of 0.69%, which ranks as one of the most negative readings in the ETF’s history. In fact, the only times that IGV was more of a one-way trade to the downside were during the Financial Crisis and at the end of the dot-com bust.