See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I don’t know what happened. It was just euphoria. I can’t even explain what I was feeling, just pure joy.” – Charlie McAvoy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Confusion regarding the state of global trade following Friday’s Supreme Court decision striking down the President’s reciprocal tariffs has futures lower to kick off the week. The fact that some form of armed conflict with Iran looks increasingly likely also hasn’t helped. As if that weren’t enough, while the blizzard in the northeast doesn’t have any direct market impact right now, it has effectively paralyzed a central area of economic activity for the day, and air traffic, so it will have some economic impact as well. Crude oil is fractionally higher at close to $67 per barrel; gold is up 2% and looks to be making a new run at its January highs; and silver is up over 5%. Bitcoin, however, is down 2% as some investors are starting to question whether it’s even an effective store of value anymore.

Overnight in Asia, China remains closed for the Lunar New Year, and Japan is also closed, but South Korean stocks traded up nearly 1%, which nowadays doesn’t even register as an impressive move. In Europe, the STOXX 600 is down modestly in a mixed session where Italy and Spain are both up roughly 1% while Germany dips about 0.5%. The disparate performances stem from strength in banks and weakness in industrials (more German-focused).

Datawise, there’s not a lot on the calendar today. At 8:30, we got the Chicago Fed National Activity Index. That will be followed by Factory Orders at 10, and the Dallas Fed at 10:30. Fed Governor Waller is also speaking this morning, and he’s on the wires saying that a March rate cut will depend on the state of the labor market, which he sees as likely remaining weak going forward, citing potential pressures from AI.

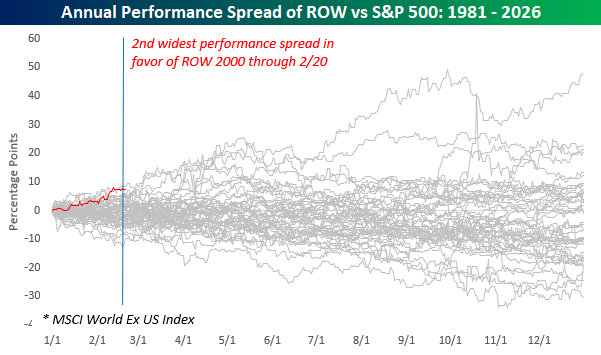

The US is on top of the hockey world this morning after Sunday’s dramatic OT win, and investors are hoping some of those gold-medal vibes rub off on the stock market. As we highlighted in Friday’s Bespoke Report, through the first several weeks of 2026, US stocks have underperformed stocks from the rest of the world to a near-historic degree. As shown in the chart below, the only year since 1980 when the S&P 500 underperformed the rest of the world by a wider margin was in 1984, and barely at that.

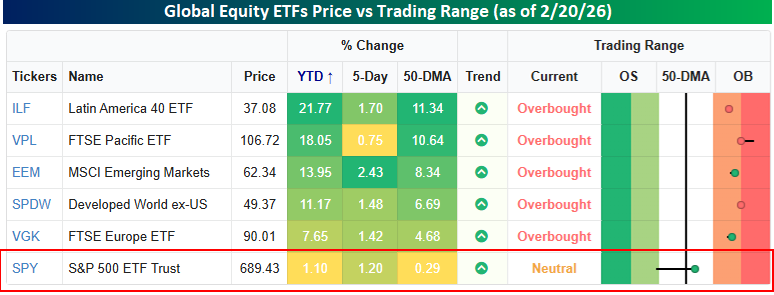

The graphic below puts the short-term US underperformance into even better perspective. Major international regional equity ETFs headed into the weekend on power plays at overbought levels (1+ standard deviation above their 50-DMAs), while the US was short-handed in penalty-killing mode and scrapping to get back above its 50-day moving average. YTD, European equities, as measured by the FTSE Europe ETF (VGK) were outperforming the S&P 500 by more than six full percentage points, but the other four regional ETFs shown were all outperforming by at least 10 full percentage points, with Latin America (ILF) outperforming by 20 percentage points – in less than two months! How the lines have shifted!

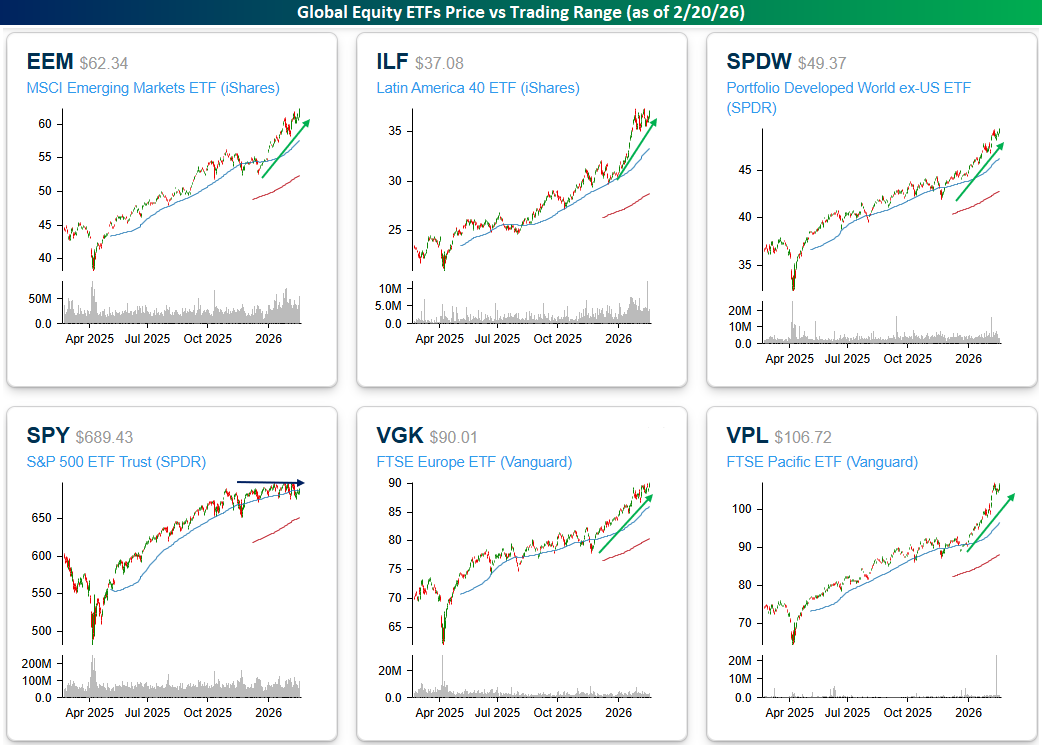

A look at the six price charts also shows the disparity between US and international stocks. Five of the charts shown are in clear, well-defined uptrends, while the US has been stuck in neutral between the blue lines, unable to push the puck into the zone, but also successfully fighting off any bearish attacks into their defensive zone.