See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I have a theory that the truth is never told during the nine-to-five hours.” – Hunter Thompson

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Ahead of a busy economic data day and possibly an important Supreme Court ruling, equity futures are modestly lower across the board, with the S&P 500, Nasdaq, and Dow all indicated lower by about 0.20%. The 10-year yield is down close to two basis points to 4.06%, and crude oil is fractionally lower as comments from the President suggest that if there is going to be a strike against Iran, it won’t come this weekend, and even if there is, it’s likely to be targeted initially. Gold prices are up 1% and back about $5,000, and Bitcoin is also fractionally higher.

Japanese stocks traded 1.1% lower and closed out the week with a modest decline, and the Hang Seng traded down by the same amount. South Korean stocks bucked the trend, though, and rallied more than 2%, finishing the week up 5.5% in just two days of trading!

European stocks are finishing the week on a more positive note, with the STOXX 600 up 0.4% and taking its WTD gain to more than 1.5%. Every major index in the region is higher on the session, and except Germany, they’re all up over 1% for the week. Flash PMI for the manufacturing sector was better than expected, while the Services PMI was slightly weaker. On the inflation front, PPI in Germany showed an unexpected decline of 0.6% versus forecasts for an increase of 0.3%.

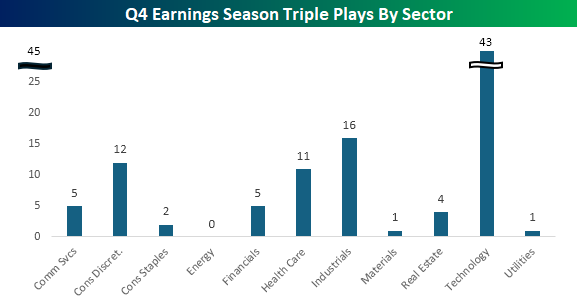

Yesterday marked the unofficial end of earnings season, with Walmart (WMT) reporting before the open. While the equity market had a muted to modestly negative performance this earnings season, there were plenty of earnings triple plays (companies that reported better than expected earnings and revenues and raised guidance). Since earnings season started in early January, 100 companies reported triple plays, and in the chart below, we break those names out by sector.

While it’s been one of the worst-performing sectors this year, the Technology sector has easily had the most earnings triple plays with 43. That’s more than double the next closest sector – Industrials, and is also more than the total of the other top four sectors combined! At the other end of the spectrum, not a single stock in the Energy sector reported a triple play, while the Materials and Utilities sectors each had one apiece.

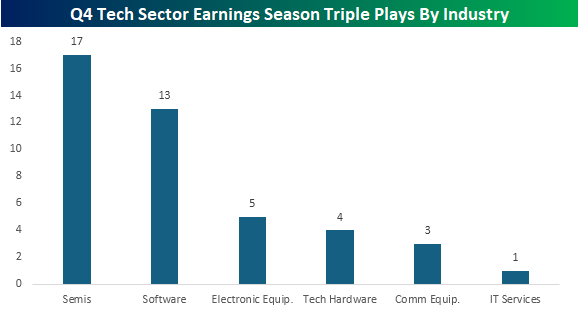

Within the Technology sector, it’s also interesting to look at where the Triple Plays have come from. Leading the way, 17 of the tech sector Triple Plays have come from semiconductor companies, which should come as no surprise, given the group’s performance this year. Next on the list, though, is software with 13 stocks. Even as the group has been slaughtered this year, there’s no shortage of companies in the group exceeding results and raising guidance. This illustrates again that while these companies may not yet be feeling the impact of AI on their businesses, it’s the long-term that investors are more worried about.