See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Shut your eyes and see.” – James Joyce

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a shaky end to the week and the month for US markets on Friday, things remain somewhat unsteady as we kick off the new month. S&P 500 futures indicate a 0.3% decline at the open, while the Nasdaq is priced to open down twice as much. For both indices, current levels are well off their lows so that it could have been a lot worse.

Treasury yields are slightly lower, with the 10-year yield starting the week at 4.23%. Crude oil is sharply lower, trading down close to 5% as President Trump suggested that the Iranians are looking to come to the bargaining table. In the metals space, it’s a mixed picture with gold up about 1% while silver bounces over 6%. Copper and Platinum, meanwhile, are both lower. After moves like we saw late last week in the space, though, we would expect more wild trading in the days ahead. These types of volatility spikes have a way of lasting more than a few days before things finally settle down.

It was a negative start to the week in Asia as the Nikkei fell over 1%, while Hong Kong and China both slumped by more than 2%. The big loser, though, was South Korea, where the KOSPI plunged over 5%, and trading briefly came to a halt because of circuit breakers. The weakness in that index stemmed from a weekend story in the WSJ where Nvidia CEO Jensen Huang said that the company’s investment in OpenAI will not be the $100 billion previously reported, and that has raised new concerns about the vitality of the AI trade.

Today is one of those rare days, it seems, where the lack of a vibrant technology sector in Europe is a plus. The STOXX 600 is up 0.4%, and the German DAX and Spain’s IBEX 35 each rally over 0.75%. Better-than-expected manufacturing PMIs for January have also acted as a positive catalyst.

In the US today, the only economic report on the calendar is the ISM Manufacturin,g which is projected to rebound slightly from December’s reading of 47.9. Given the surprise strength in the Chicago PMI last week, though, don’t be surprised if that report comes in hot. Outside of economic data, the first major tech report of the week will be Palantir (PLTR) after the close. As we detailed in today’s Chart of the Day, growth-oriented sectors of the market have been messy lately, so PLTR’s report could have big implications for the sector.

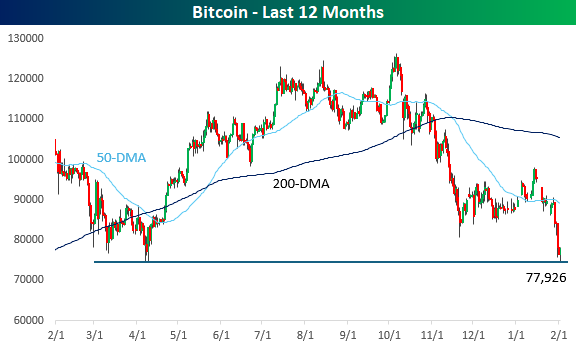

Along with growth-oriented stocks, crypto assets have been terrible performers for the last few months, and over the weekend, Bitcoin tested 52-week lows near $75K. Prices are rebounding slightly this morning along with equity futures, but the burden of proof is firmly on the back of the bulls now as Bitcoin’s price trades near the breakeven price for all of Strategy’s (MSTR) holdings.

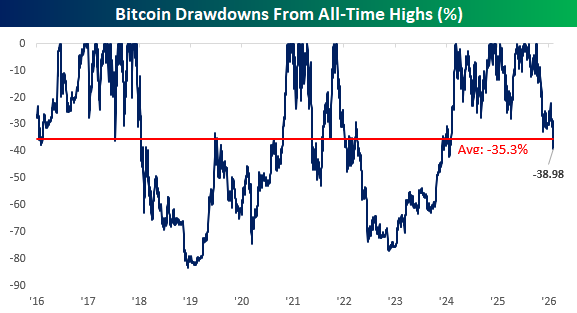

While it’s been a painful few months for crypto, it’s worth pointing out that this remains just a run-of-the-mill decline for Bitcoin. While it’s currently down about 39% from its all-time high, on any given day since 2016, its average drawdown from an all-time high has been over 35%.