See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You just have to find that thing that’s special about you that distinguishes you from all the others, and through true talent, hard work, and passion, anything can happen.” – Dr Dre

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equities are poised to open higher this morning, but futures are well off their overnight highs. As things stand, the S&P 500 is on pace for a 0.35% rally at the open while the Nasdaq is up 0.45%. The 10-year yield is up less than a basis point, but with the yield over 4.06%, it’s well off its intraday low of under 4.02% yesterday. Oil prices are up over 2.5% as markets remain on edge over the possibility of military action in Iran. That has also helped to push gold prices up over 1%, even as they remain under $5,000 per ounce.

While most of Asia remains closed for the Lunar New Year, Japanese markets were open for trading, and the Nikkei rallied 1% as export growth came in stronger than expected. The country’s trade minister also announced the first tranche of investments for US infrastructure projects, which was part of the trade deal.

In Europe, we’re also seeing broad-based strength with the STOXX 600 up just under 1%, led higher by Spain and Italy. There’s no real catalyst behind the gains, but UK and French CPI data were generally inline with expectations.

There’s a busy schedule of economic data today, kicking off with Durable Goods (better than expected), Building Permits (better than expected), and Housing Starts (better than expected) at 8:30, followed by Industrial Production and Capacity Utilization at 9:15 followed by Leading Indicators at 10:00. At 2 PM, we’ll also get the Minutes from the January FOMC meeting, and in between Fed Vice Chair Bowman will be speaking in DC at 1 PM Eastern.

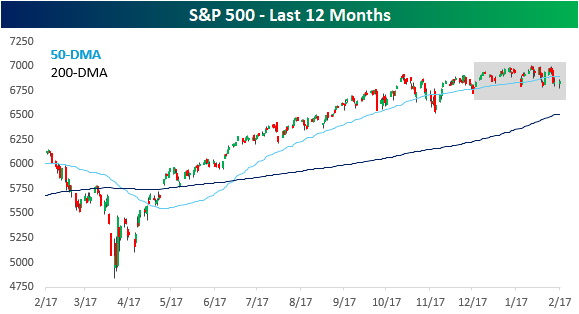

There have been 31 trading days so far in 2026, and for many, it’s been an exhausting year in the markets. For all the sound and fury, though, consider this. On 12/31, the S&P 500 closed at 6845.50. Yesterday, it closed at 6843.22. Just two points lower! For the year, the S&P 500 is down just 0.03%!

On the one hand, the S&P 500’s inability to make any headway this year (and over the last five months, for that matter) is enough to make you want to rip your hair out, but after the rally the market had off the April lows, some consolidation was in order, so you could say this is exactly what the market needed.

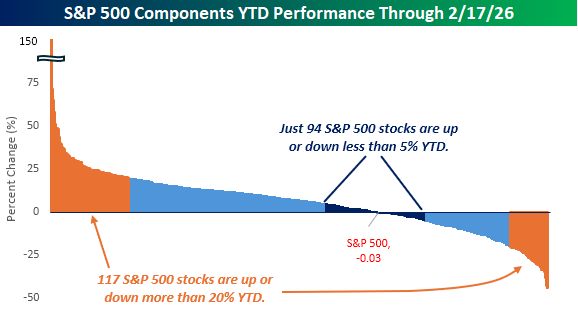

While there’s been nothing going on at the index level, underneath the surface, we’ve seen massive rotation. While the S&P 500 is flat on the year, just 94, or less than 20% of the index’s components, are up or down less than 5%. At the extremes, though, 117 stocks are up or down at least 20% YTD! It seems that Washington isn’t the only place where we’ve seen an increase in concentration at the extremes with nothing to show for it.

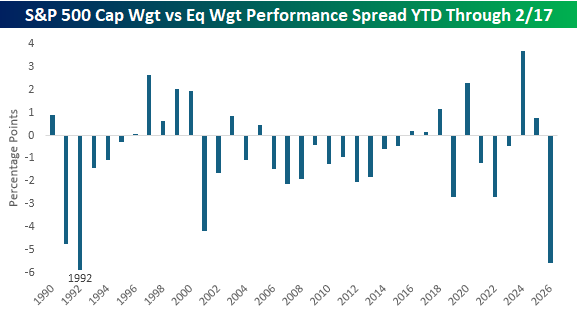

While the big moves in individual components of the S&P 500 haven’t shown up at the index level, on an equal-weighted basis, the S&P 500 has much more to show for it this year as it’s up 5.5% YTD. With that gain, the S&P 500 cap-weighted index is underperforming its equal-weighted peer by 5.53 percentage points YTD. Since 1990, the only other year when the cap-weighted index underperformed the equal-weighted index by a larger amount was in 1992. In that year, the outperformance of the equal-weighted index continued through the rest of the year, but both indices were up more than 5% from that point through year-end.