See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Life’s under no obligation to give us what we expect.”- Margaret Mitchell, Gone With the Wind

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a rough end to last week, bulls are shaking the dirt off their shoulders and looking to make a stand as we head into the final half of the month. Both the S&P 500 and Nasdaq are down fractionally so far this month, but with the seasonally strong second half of the month now here, will the bulls show up?

So far, they’re coming out on the offensive. Futures on all three of the major averages are higher by roughly 0.5%. The 10-year yield is moving lower and picking up in pace to the downside following a weaker-than-expected Empire Manufacturing report. Crude oil is fractionally higher, while gold and Bitcoin move higher.

Asian stocks started the week with broad-based losses. The South Korean Kospi led the losses with a decline of 1.8%, but both the Nikkei and Hang Seng finished down 1.3%. China also finished lower, but the losses were more contained at 0.6%. Besides follow-through from Friday’s losses in the US, the declines in the region also followed weak economic data out of China, where Industrial Production (4.8% y/y) and Retail Sales (1.3% y/y) both missed expectations.

Unlike Asia, European stocks are higher across the board with the STOXX 600 trading up 0.8%, with the UK, France, Italy, and Spain all up over 1% while Germany lags as peace talks in Ukraine continue to drag on.

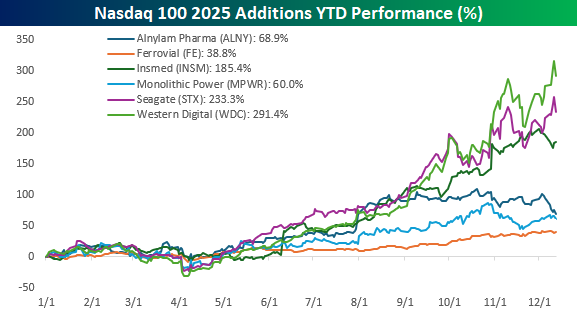

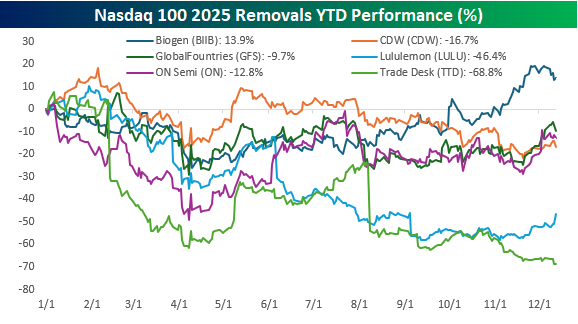

On Friday, Nasdaq announced the annual changes to the Nasdaq 100, and for this year’s shakeup, six stocks will be added and six removed. The new class of 2025 includes Alnylam Pharmaceuticals (ALNY), Ferrovial (FER), Insmed (INSM), Monolithic Power Systems (MPWR), Seagate Technology (STX), and Western Digital (WDC). The six stocks being removed to make room are Biogen (BIIB), CDW (CDW), GlobalFoundries (GFS), Lululemon Athletica (LULU), ON Semiconductor (ON), and The Trade Desk (TTD).

The two charts below show the performance of the six stocks being added and removed from the Nasdaq 100 on a YTD basis, and judging by their performance, one factor that appears to be part of the criteria is popularity. All six of the stocks being added this year have positive returns since the start of the year, and the median gain is 127.2%. Leading the way higher, Western Digital (WDC) and Seagate Technology (STX) have both rallied more than 200%. Even the worst performer of those stocks being added – Ferrovial (FE) – was 38.8%.

Turning to the six stocks being removed, they haven’t exactly shone this year. Five out of six of the stocks are down on the year, and the only winner – Biogen (BIIB) – is up only 13.9%. All totaled, the median performance of the six stocks is a decline of 14.8%.

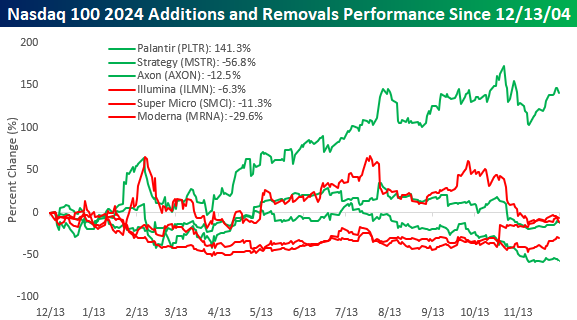

While six stocks are being added and removed this year, last year, there were only three. With one exception, the performance of both the stocks being added and removed from the Nasdaq 100 wasn’t particularly good. As shown in the chart below, shares of Palantir (PLTR) have rallied 141.3% since last year’s announcement that it was being added to the Nasdaq 100, but shares of Strategy (MSTR) and Axon (AXON) are both lower. Likewise, all three of the stocks removed last year are also lower, with declines in the range of 6.3% for Illumina (ILMN) to 29.6% for Moderna (MRNA).

Finally, since we’re talking about the Nasdaq 100, it’s worth pointing out that the index closed below its 50-day moving average again to close out last week as the latest rally off the November lows failed to make a higher high. With megacaps like Nvidia (NVDA), Microsoft (MSFT), and Oracle (ORCL) faltering recently, it’s showing up in the performance of indices they dominate, like the Nasdaq 100.