See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“In today’s regulatory environment, it’s virtually impossible to violate rules.” – Bernard Madoff

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

17 years ago today, all hell was already breaking loose in financial markets as the banking sector had imploded three months earlier. Lehman’s bankruptcy accelerated a chain of failures and near-failures in some of the country’s most well-established banks. As if the market needed any more bombs hurled at it, along came the “Breaking News” interruptions on the news channels of a Ponzi scheme surrounding a man named Bernie Madoff. We’ve come a long way in the last 17 years, and after yesterday’s Fed meeting, the S&P 500 is back right near record highs and has rallied nearly 10-fold after accounting for dividends.

This morning, equity futures are taking a breather. Oracle (ORCL) earnings after the close last put renewed doubt on the AI trade, and the stock is down 13% as investors question whether the company can fund its ambitious capex plans. If that magnitude of decline, it would be the stock’s largest downside gap in reaction to earnings since at least 2001. Make sure to read our detailed discussion of ORCL earnings and investor concerns regarding the stock and the AI trade in the commentary section of today’s report.

After trading down close to 1% overnight, though, S&P 500 futures have rebounded and are now down just 0.3% while the Nasdaq is down 0.5%. Treasury yields are down another 3 basis points (bps) to 4.13%, and crude oil is down below $58 per barrel, falling over 1%. Gold is fractionally higher, but Bitcoin and other crypto assets have reversed all of their gains from the prior 24 hours.

In Asia, stocks traded mostly lower, with the Nikkei down 0.9% and South Korea down 0.6% as ORCL’s earnings dragged on the region. In Europe, though, we’re seeing modest gains across the board with the STOXX 600 trading 0.2% higher.

In the US, the only economic data release on the calendar this morning was jobless claims. Initial claims came in higher than expected at 236K (versus 220K), erasing all of last week’s surprising decline. Meanwhile, continuing claims showed a sharp decline, falling to 1.838 million, or 100K less than expected. The continuing claims number is lagged a week, so the sharp drop in initial claims last week was likely a holiday quirk.

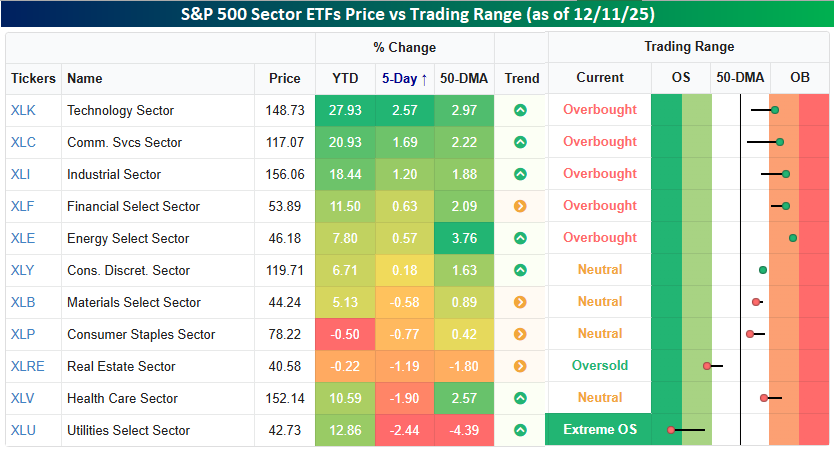

The S&P 500 closed within fractions of a new high yesterday, and the same sectors that have driven the market this year are the ones that have driven the rally over the last week. As shown in the snapshot below, Technology, Communication Services, and Industrials are the only two sectors up over 1% in the last five trading days, and they’re also the three best-performing sectors this year.

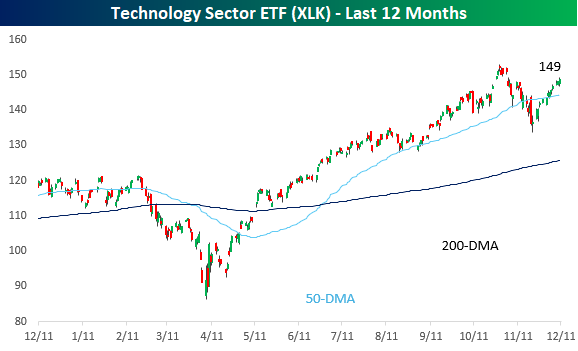

While the S&P 500 closed within whiskers of a new high and tech has led the rally, the Technology sector still has a ways to go before hitting a new high, as yesterday’s close was more than 2% below the late-October high. What stands out about the chart, though, is how much green there has been in the candles since the November low.

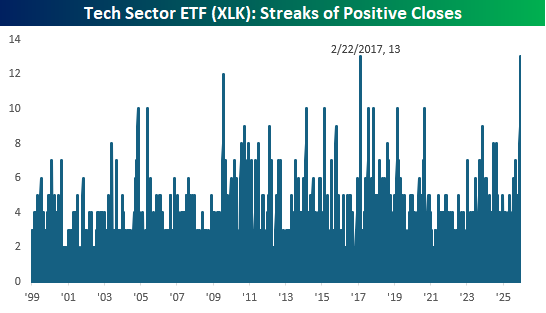

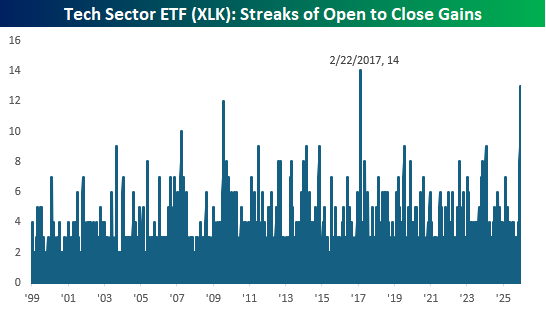

In fact, with 13 straight days of gains and 13 straight days of positive returns from the open to close, the Technology sector ETF (XLK) is knocking on the door of history. The 13 days in a row of daily gains are tied for the longest in the ETF’s history, dating back to 1999. The only other streak as long ended in February 2017. Similarly, the streak of open-to-close rallies is just one shy of the 14-day streak that also ended in February 2017.

What surprised us most about the Technology sector’s recent run is the stocks that have been driving the bus. Nine Technology sector stocks are up over 25% since the close on 11/20, and the majority are semiconductor stocks. One semi-stock not on the list of winners, though, is Nvidia (NVDA). While it’s not down since 11/20, NVDA’s 1.74% gain ranks as the eighth-worst performance in the sector. Also on the list of laggards is Microsoft (MSFT), which is barely higher since 11/20 (+0.03%). These two stocks collectively account for about 25% of the entire Technology sector, but as they have tread water over the last two weeks, the sector they dominate has still rallied over 9%. Is the baton being passed?