See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Many people are busy trying to find better ways of doing things that should not have to be done at all. There is no progress in merely finding a better way to do a useless thing.” – Henry Ford

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a zero-gravity rally on Friday that pushed the S&P 500 into positive territory for the month and extended the S&P 500’s monthly winning streak to seven, equities are rediscovering gravity to start December as futures on the major averages all trade lower. The Nasdaq is poised to open down nearly 1% while the S&P 500 faces a 0.7% decline. Even with equities falling, treasury yields are also higher as the 10-year ticks up 3 bps to 4.05%. Crude oil is up just over 1% as OPEC+ announced plans to maintain output levels rather than raise them, and gold is back near $4,300, gaining about 0.8%. The big loser on the day, though, is Bitcoin. With a decline of over 6%, the largest crypto is on pace for its worst day since March, and part of the weakness could be related to reports that Strategy (MSTR) could potentially be forced to sell some of its holdings to fund its dividend.

The weakness started in Asia as the Nikkei fell close to 2% as JGB yields continue hitting levels not seen since before the Financial Crisis, as expectations for a rate hike later this month solidify. In China, stocks went the other way with the Shanghai Composite rallying 0.7%, even as November Manufacturing and Non-Manufacturing PMIs remained in contraction territory.

In Europe, the losses have been more uniform as the STOXX 600 falls 0.5% as Manufacturing PMIs for the economic bloc and individual countries missed expectations. The biggest loser on a country basis is Germany, as the DAX declines more than 1.5% as defense contractors have been especially weak on reports of progress in the Russia-Ukraine war talks.

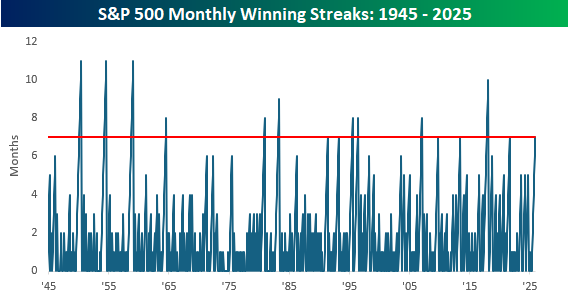

As mentioned above, the S&P 500’s winning streak extended to seven in November, and that’s the longest streak of gains for the index in more than four years (August 2021). Since the end of WWII, there have been 15 other seven-month winning streaks, with the longest being eleven. Believe it or not, that happened three times, all of which were all in the 1950s. So, while history always talks about the roaring twenties, don’t forget about the fantastic fifties.

Outside of those three eleven-month winning streaks in the 1950s, the only other streak that extended into the double-digits was the 10-month streak that kicked off President Trump’s first term in office, ending in January 2018 (seventh month was October 2017). Getting back to the most recent streak, the seven months ending in August 2021 were followed by a sharp decline of 4.8% the following month, and weak returns thereafter.

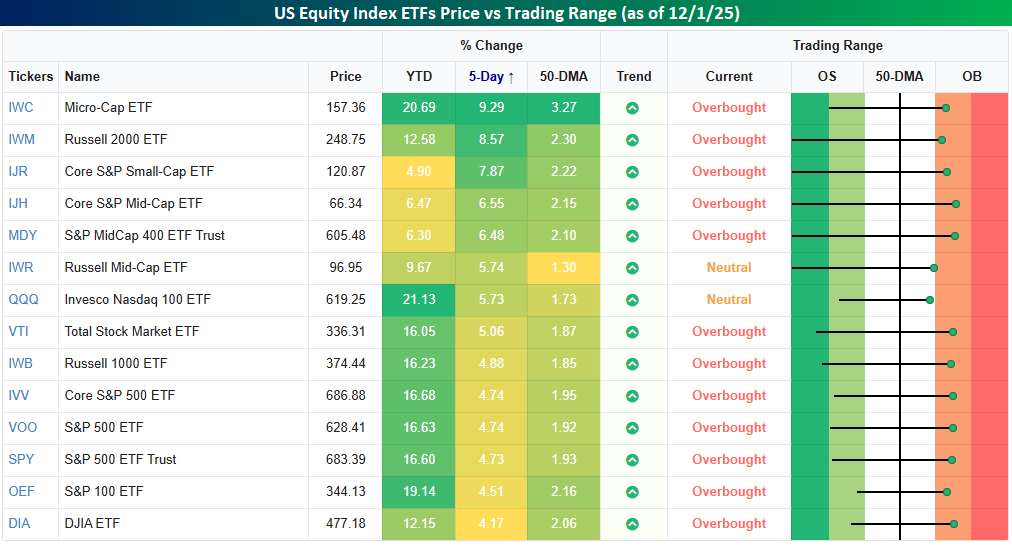

Last week, right before Thanksgiving, we pointed out that the S&P 500 and other major US equity indices had quickly gone from oversold to neutral. In the two trading days since then, the rally kicked into another gear with little selling resistance (as evidenced by Friday’s rally), and all but two of the major equity index ETFs in our Trend Analyzer snapshot have moved into overbought territory. The only exceptions are the Russell Mic-Cap ETF (IWR) and the Nasdaq 100 (QQQ), and while they may not be overbought, they still rallied over 5% in the five trading days through last Friday’s close (from close on 11/20).

Of all the ETFs shown, every one of them was up at least 4% in the trailing five trading days. While large-cap ETFs lagged with gains of less than 5%, small caps had a day in the sun with the Russell Micro Cap ETF (IWC) surging 9% while the Russell 2000 ETF rallied over 8.5%. While usually not the case in recent months, this rally has been one where big gains came in small packages.