See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“America’s health care system is neither healthy, caring, nor a system.” – Walter Cronkite

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a strangely subdued reaction to its earnings report after the close yesterday, shares of Palantir (PLTR) are down nearly 8% in the pre-market as investors had some time to sleep on it overnight. An 8% decline is nothing to dismiss, but it’s also important to remember that PLTR is a volatile stock. In its history as a public company, the average one-day reaction to earnings has been a gain or loss of over 15%, and based on where it’s trading now, shares of PLTR are back to where they were just last Tuesday.

The decline in PLTR comes as a cloud of concern envelops the market over how fast stocks have rallied and where valuations have gone. Right on cue, a Bloomberg article says as much with the headline below. While the headline sounds scary enough, the details read a lot less scary. Essentially, it quotes various Wall Street CEOs, among them Morgan Stanley CEO Ted Pick and Goldman Sachs CEO David Solomon, suggesting that the market could see a pullback of 10% to 20% at some point in the next 12 to 24 months. Solomon was quoted as saying, “Of course, it’s likely there will be a 10% to 20% drawdown in equity markets over the next 12 months,” but even he admitted that pullbacks like that can come at any time and from any level.

Concerns are concerns, though, and when investors worry, they sell. With that, futures on the S&P 500 and Nasdaq are both indicated to open down by more than 1%, following a down session in Asia and Europe, where stocks are also broadly lower by around 1% or more.

Even with the sharp decline in equities, bond yields are only modestly lower as the 10-year yield still hangs around 4.1%. Crude oil prices are also down more than 1%, which suggests that investors are also concerned about the health of the economy, given the ongoing shutdown. We’ll be watching the level of airport delays; the more they rise, the more likely it is that policymakers in DC reach an agreement to open the government back up. Thanksgiving is just three weeks away, and no one on either side of the aisle wants to face the wrath of Americans who can’t get home for the holiday.

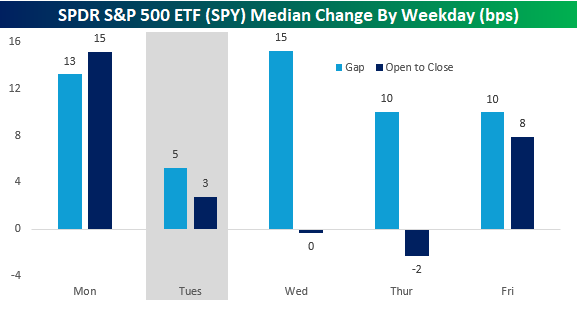

Given the scope of the pre-market declines, it must be Tuesday. As shown in the chart below, the S&P 500’s median opening gap on Tuesdays this year has been just five basis points (bps), which is less than half the next closest weekdays (Thursdays and Fridays), so the day has had a knack for weakness. From the open to close, Tuesday isn’t the weakest day of the week, but it’s still much weaker than the median gains of 15 bps on Monday and 8 bps on Friday.