See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“It would be a mistake to think something is wonderful just because it looks great.” – Anna Wintour

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Last week may have been the peak week of earnings season in terms of the market cap of companies reporting, but we have another busy week in store for investors, and it’s picking up right where it left off last week. Of the companies reporting so far today, 89% have reported better than expected EPS forecasts, and 75% have topped sales forecasts, so you can’t ask for much more than that. Even in terms of guidance, 3 companies have raised forecasts while only one lowered.

In response to the better-than-expected reports, equity futures are also picking up right where they left off last week, as markets look to open the week higher with the Nasdaq leading the way. Today’s positive open for the Nasdaq will be the ninth straight positive start to a week for the index, which is only the longest streak since summer 2024, but still tied for the second longest in the index’s history.

In Asia, Japan was closed for the day, but other indices in the region were broadly higher even as South Korea’s manufacturing PMI moved into contraction territory. In Europe, most manufacturing PMIs were also in line with forecasts, and the STOXX 600 responded by rallying 0.5% while Germany rallied more than 1%.

Outside of equities, the 10-year yield is slightly lower at 4.09% ahead of a busy week for Fed speakers, who have mostly sounded more skeptical of a December rate cut, as concerns over inflation linger even as there are signs that the labor market is stabilizing.

Crude oil prices are essentially unchanged even as OPEC+ announced over the weekend that it would increase output by 137K barrels per day, but then pause those increases beginning in January. WTI is starting the month just over $60 per barrel after declining 2% in October, taking its monthly losing streak to three months.

Gold prices are starting off the month back above $4,000 per ounce as other metals also trade higher, but the troubles for digital gold continue as bitcoin prices trade down close to 2% and barely hangs on to $108K. Ethereum prices are down twice as much as they barely hang on to $3,700.

With just two months left in the year, over the weekend, we looked at asset class performance, country performance, and individual stock performance for October and various other time periods. Make sure to take a look at that rundown of where things stand heading into year-end. Even though the major averages may be looking good, not everything looks great.

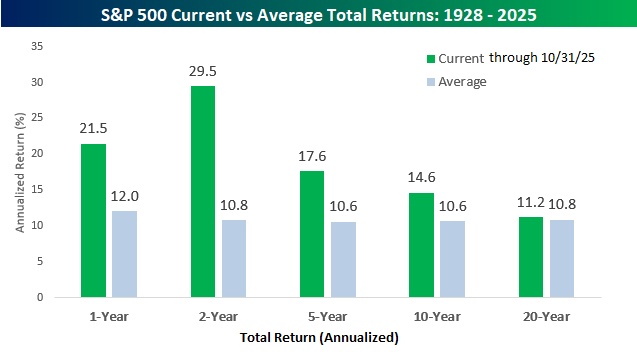

Taking a high-level look at equity market returns, whether you’re looking at the short-term or long-term, it has been a friendly environment. Over the last year, the S&P 500’s total return has been a gain of 21.5% which is nearly twice the historical average of 12.0%, but over the last two years, the 29.5% annualized gain has been nearly triple the long-term average. Looking out over longer-term time periods, though, over the last five, ten, and twenty years, returns aren’t as strong, but they’re still above the long-term average.

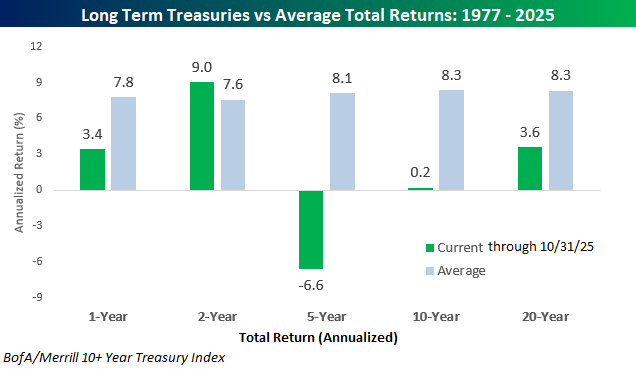

While equity market investors have been on a highway paved in green, the treasury market has been a world of pain. Over the last year, long-term treasuries, as measured by the BofA/Merrill 10+ Year Treasury Index, have posted positive returns, but at 3.4% it’s still less than half of the long-term average. Over the last two years, the annualized gain of 9.0% is actually slightly above average. Still, looking back further than that, it’s been a painful five, ten and twenty years for anyone who has loaned money to the US Treasury.