See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Stop worrying about the world ending today. It’s already tomorrow in Australia.” – Charles Schulz

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s only Wednesday, but today is the last full trading day of the week, so it feels like a Friday. Futures look poised to extend the rally from last Friday into a fourth day with S&P 500 and Nasdaq futures up 0.2% after reclaiming their 50-day moving averages yesterday. The Nasdaq’s gain comes despite another 1% decline for Nvidia (NVDA), which has hit a rough patch of news in the last few days. After yesterday’s reports that Meta (META) was looking to purchase some AI chips from Alphabet (GOOGL) to diversify from NVDA, this morning, The Information is reporting that China continues to move away from NVDA chips, with the latest example being a government order blocking ByteDance from using NVDA chips in its datacenters.

Since markets are closed tomorrow, weekly jobless claims came out early this week, so after weeks of delayed reports, now we’re getting an early report! The early news was also good as both initial and continuing claims came in lower than forecast. Durable Goods and Cap Goods orders were also released and came in better than expected. Along with these reports, the Chicago PMI report for November comes out at 9:45.

Outside of equities, treasury yields are basically flat, with the 10-year yield right at 4%. Crude oil is fractionally lower again, while gold trades marginally higher, and bitcoin is lower.

Asian markets finished the mid-week session mostly higher. The lone exception was China’s Shanghai Composite, which saw a modest decline. South Korea led the region higher with a gain of 2.7% while Japan finished up 1.9%. European markets are mostly higher, with the STOXX 600 up 0.4%, but Germany is underperforming after the IMF says that the economy is likely to undershoot growth expectations given its current trajectory.

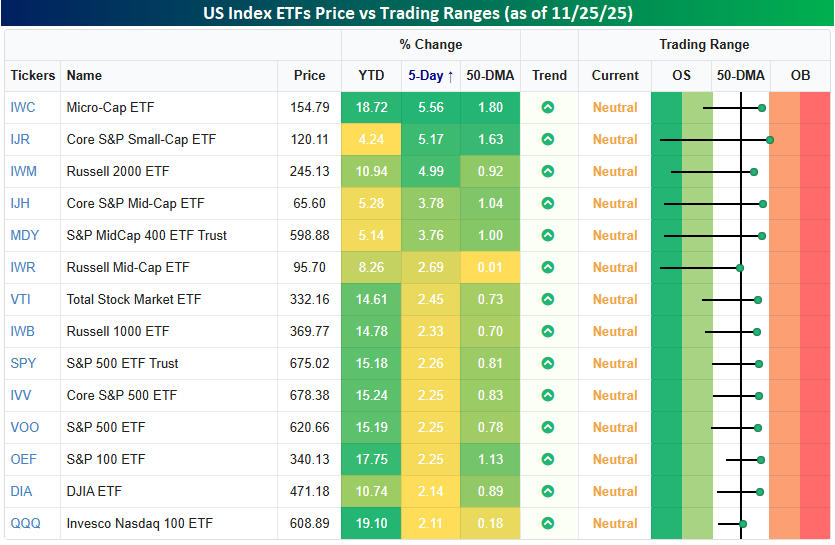

Whenever we hear the term “neutral,” we associate it with the word stuck giving it a negative connotation. There’s nothing negative about the neutral state of the major US equity indices, though, since it follows what were mostly oversold conditions last week at this time. As shown in the snapshot below, a week ago, all the index ETFs in our Trend Analyzer snapshot were below their 50-day moving averages, and most of them were oversold. As of yesterday’s close, none of them were oversold, and all of them were above their 50-DMAs. We’ll take neutral!

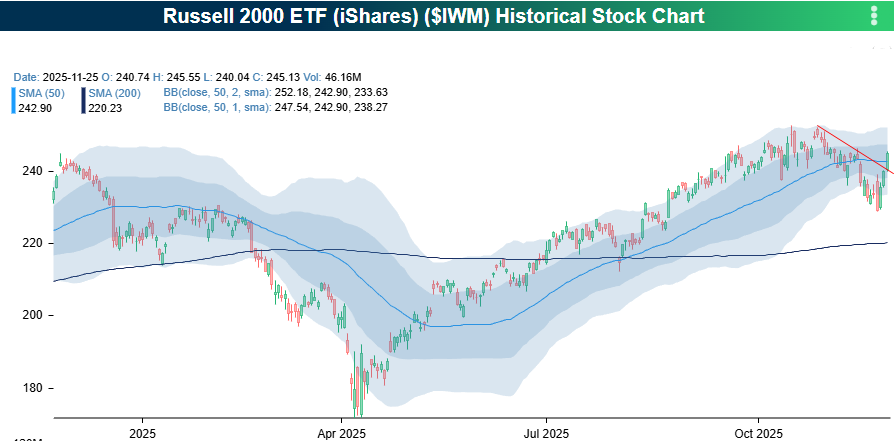

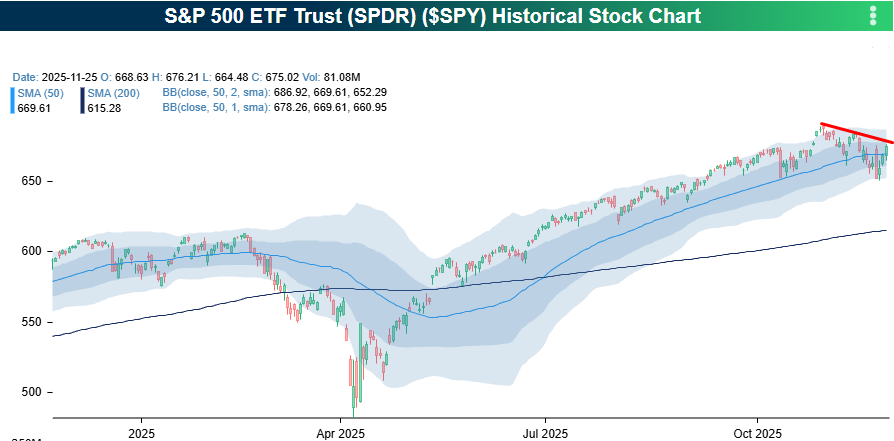

While bulls have welcomed the rebound in US equities, large-cap stocks still have more work to do before breaking the short-term downtrends that have been in place since the October highs. As shown in the two charts below, the S&P 500 ETF closed yesterday just below that downtrend line, while QQQ tested that downtrend yesterday and even peeked above it, depending on how hard you squint.

As the snapshot above illustrates, small-cap stocks have led the rally over the last five trading days with gains of about 5% compared to gains of about half that for their large-cap peers. With that outperformance, the Russell 2000 broke its downtrend from the October highs. Is this the long-awaited broadening we’ve all been waiting for?