See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Beware of geeks bearing formulas.” – Warren Buffett

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Can we shut down the government again, already? After President Trump signed legislation into law on Wednesday night to reopen the government, stocks have done nothing but trade lower. On Thursday, the S&P 500 traded more than 1.5% lower, and this morning, futures are indicated to open down another 1% with the Nasdaq down even more (-1.6%). Oil prices are higher this morning following reports of a Ukrainian attack on a Russian port, but gold is lower, falling 2% to just over $4,100 per ounce. The most pain, however, is being felt in the crypto space, where Bitcoin is down another 3% to $95,000 and Ethereum is down 1.6% to $3,120. There’s no economic data on the calendar this morning, but we’ll hear from several Fed speakers who will likely shed further light on the direction of policy at the December meeting.

It was a bloodbath in Asian equity markets to close out the week as most major averages were down well over 1%, including South Korea, where, despite finalizing its trade deal with the US, the KOSPI fell 3.8% but still finished 1.5% higher on the week. Besides following through from yesterday’s weakness in the US, weak investment and industrial production data in China helped to drive the region’s decline.

European stocks are also closing out the week on a down note, but are still on pace to finish the week higher. The STOXX 600 is down over 1.5%, and every major country’s benchmark is down at least 1.5%. Eurozone GDP came in slightly higher than expected, while employment was in line with expectations.

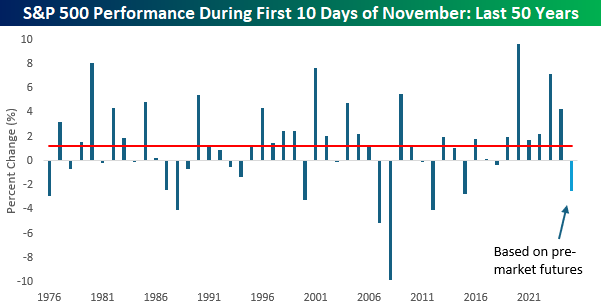

With S&P 500 futures trading down 1% in the pre-market, the S&P 500’s month-to-date decline will be right around 2.5% at the open today, and if that decline holds, it will be the weakest first 10 trading day start to November since 2017 (-2.7%), and after that, the worst was 4% in 2012. If there’s any consolation to the weakness, a weak start to November doesn’t necessarily mean bad things for the rest of the year. In the eight prior years over the last 50 that the S&P 500 traded down 2%+ in the first ten trading days of November, the median rest of year change was a gain of 2.2% with positive returns 75% of the time. For all other years, the median gain was 1.9% with positive returns 78% of the time.

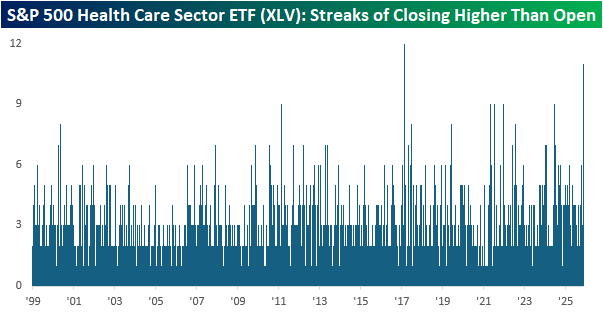

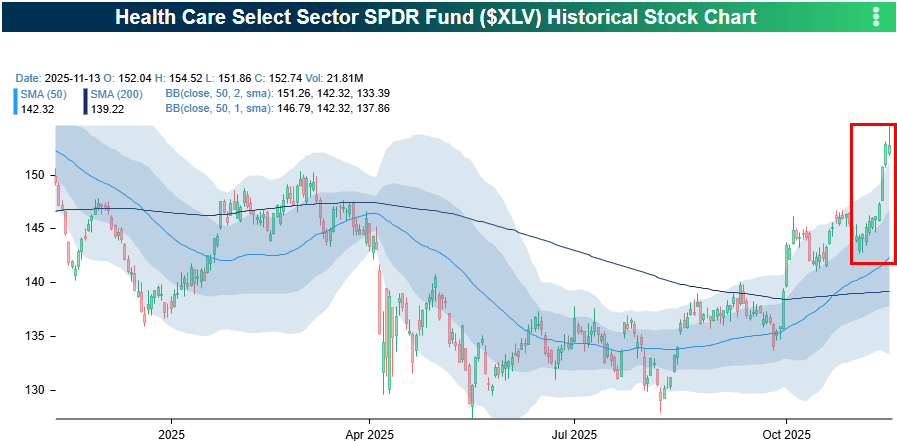

While the S&P 500 is down this week, one sector bucking the trend is Health Care. Through Thursday’s close, the sector was up 4.5%, which was more than twice the gain of the next closest sector (Materials). It’s been an impressive run lately for Health Care. After underperforming for most of the year, XLV has broken out to 52-week highs this week in what has been a buying frenzy. As shown on the right side of the chart, the sector has closed higher than it opened for 11 straight trading days!

Over the past 11 days, the current streak of closes higher than the opening price in XLV ranks as the second longest in the ETF’s history. While there have been five other streaks of 9 days, the only streak longer than the current 11-day streak was a 12-day streak that ended in February 2017.