See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The work of today is the history of tomorrow and we are its makers” – Juliette Gordon Low

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view yesterday’s CNBC interview talking about market breadth, click on the image below.

The S&P 500 heads into today with just fractional gains for the week, but today’s trading should add to those gains with futures indicated 0.7% higher. Strong earnings from the mega-caps are to thank for the gains, as what has already been a positive earnings season continues. Outside of equities, treasury yields are slightly higher, while crude oil trades slightly lower but has hung on to $60 per barrel for now. Metals prices are mixed as gold hangs on to $4,000 while silver and copper are essentially unchanged. Crypto is showing some life as Bitcoin trades higher by 3% and Ethereum rallies closer to 5%.

In Asia overnight, markets were mixed. Japan, China, and South Korea all closed out the week higher and with solid gains for the week, but Hong Kong and India were both lower. The biggest economic datapoints of the session were PMI readings in China as the Manufacturing index slid further into contraction territory while the Services component barely stayed out of contraction (50.1).

In Europe, there’s another negative bias with the STOXX 600 down 0.4% as an index of inflation expectations showed a modest uptick from 2.0% to 2.1% for 2025. It wasn’t all bad news, though, as 2025 GDP growth forecasts also showed a modest uptick from 1.1% to a still anemic 1.2%. The higher inflation expectations were also accompanied by an uptick in headline CPI to 0.2% m/m from September’s rate of 0.1%.

Apple (AAPL) and Amazon.com (AMZN) rounded out the group of mega-caps reporting this week with earnings releases after the bell Thursday. Shares of Apple (AAPL) are poised to gap up over 2% at the open, but the real standout is Amazon.com (AMZN). While investors worried that the company’s layoff announcement earlier in the week was a precursor to a weak report, AMZN eased those fears with strong numbers across the board, and in response, shares spiked more than 10%.

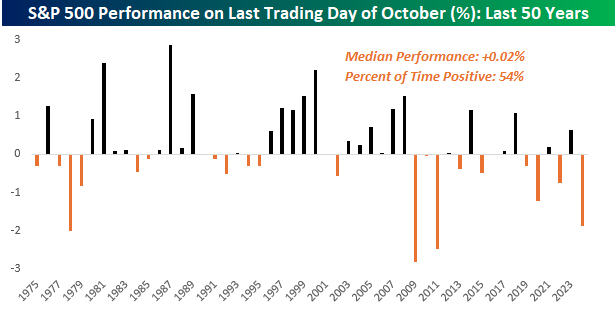

Today is Halloween and the last trading day of October, so can investors expect a trick or a treat? Over the last 50 years, it’s been a bit of a coin flip. As shown in the chart below, the S&P 500’s median performance on the last trading day of October has been a gain of 0.02% with positive returns 54% of the time. In terms of volatility, the median absolute daily change on these days has been 0.50%.

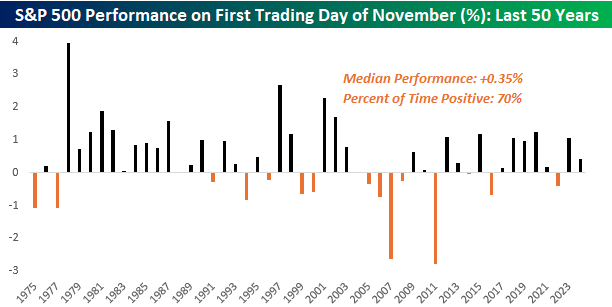

While the last day of October has been relatively uneventful in terms of returns, November typically starts on a more positive note. Over the last 50 years, the S&P 500’s median gain has been 0.35% with gains 70% of the time. And while October is a month known for its volatility, with a median absolute daily change of 0.77%, the first trading day of November has been more volatile than the last day of October.