See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Women who seek to be equal with men lack ambition” – Timothy Leary

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The post 10/8 range-bound slog looks set to continue for the S&P 500 today as it enters its eighth day in a row of trading within its intraday range from 10/10. S&P 500 futures are essentially unchanged, while Nasdaq futures point to a modest decline. Yesterday’s weakness in gold and other precious metals has continued this morning, with gold down more than 1%, and while the crypto markets had a positive reversal yesterday, they’re giving it all back today as volatility in that space continues.

Overnight in Asia, most indices saw modest declines, although South Korea managed to buck the trend as it seems nothing can keep the Kospi down. European shares are mixed. The STOXX 600 is trading modestly higher on the session, led higher by the FTSE 100 and Spain’s Ibex 35, while Italy is down 0.5%. This morning’s strength in the UK was catalyzed by a much weaker than expected September CPI report, which showed no change in consumer prices relative to forecasts for an increase of 0.2%.

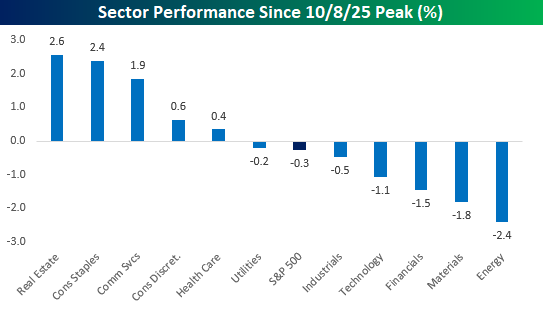

It’s now been two weeks since the S&P 500’s last record high, and while the S&P 500 has seen just marginal declines, some of the moves within sectors have been much larger. As shown in the chart below, Real Estate and Consumer Staples have both rallied over 2% and join Communication Services as the three sectors with gains of over 1%. To the downside, five sectors have declined since the 10/8 high, but four of them are down over 1%, including Energy (-2.4%) and Materials (-1.8%). Technology has also slumped 1.1%, which has acted as the main driver of the index’s decline.

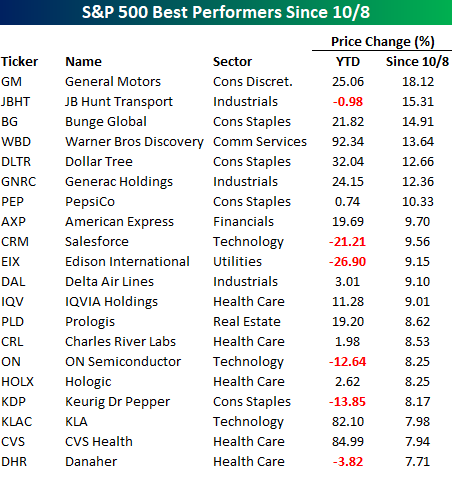

At the individual stock level, it’s been an eclectic mix of winners and losers. Starting with the winners, General Motors (GM) tops the list after yesterday’s post-earnings surge, and it’s one of seven stocks in the S&P 500 that have rallied over 10% since the 10/8 peak. While many of the 20 best-performing stocks in the S&P 500 are handily up YTD, they aren’t exactly the typical winners investors have been used to seeing throughout most of the year. The sector breakdown of these winners further illustrates that trend, as nearly half of the names listed are either from the Health Care (5) or Consumer Staples (4) sectors.

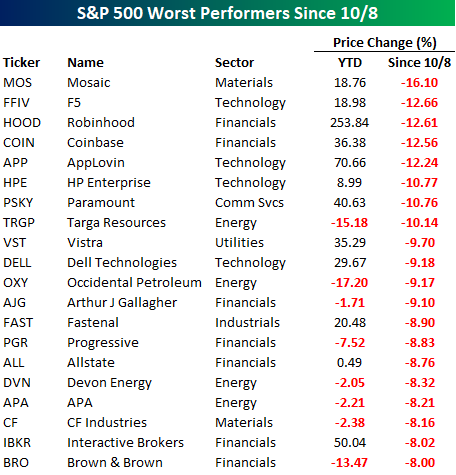

Shifting to the biggest losers, eight stocks in the S&P 500 have seen double-digit percentage declines since the 10/8 peak. Leading the way to the downside, Mosaic (MOS) has declined more than 16%. While many stocks listed have underperformed this year, for stocks like Robinhood (HOOD), Paramount (PSKY), Vistra (VST), Dell (DELL), and Interactive Brokers (IBKR), it has been a pause to potentially refresh.

At the sector level, Financials has been most heavily represented, with over a third of the names listed as concerns in the credit markets have hit some of the names in the sector hard. After Financials, the next most heavily represented sectors are Energy and Technology, with four each.