See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“When one tugs at a single thing in nature, he finds it attached to the rest of the world.” – John Muir

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Paul Hickey appeared on CNBC’s Squawk on the Street yesterday to discuss the market setup heading into the fourth quarter. To view the segment, click on the image below.

The government shut down at midnight, and futures are moderately lower this morning, with the S&P 500 and Nasdaq trading down 0.5%. All the market-related headlines, therefore, have attributed the weakness to the shutdown, and we can only imagine that somewhere out there, Eugene Fama is smashing his head against a wall. The prospect of a shutdown has been well known for weeks now, and betting markets were pricing in a near certainty of one yesterday, so if markets really were concerned and there was even a bit of truth to the Efficient Market Hypothesis, the S&P 500 wouldn’t have traded up 0.4% yesterday. So, why is the market lower? There could be multiple reasons, and the fact that it’s the first day of a new quarter, where investors rebalance their holdings, could be one of them.

Outside of equities, US Treasury yields are modestly lower, oil is down half a percent, and gold is up 1% and above $3,900 as it marches towards $4,000 per ounce. Crypto is catching a bid with Bitcoin up 2%, while Ethereum and Solana are both up 4%.

On the data calendar this morning, we got the ADP report at 8:15, which showed an unexpected decline, and ISM Manufacturing and Construction Spending will hit the tape at 10 AM. Despite the weaker ADP report, futures have seen little reaction.

In international markets, Japan finished the first day of the quarter with a decline of nearly 1% following a weaker-than-expected Manufacturing PMI reading, while India and South Korea traded up nearly 1%. Both Hong Kong and China were closed for holidays. European stocks are higher across the board, with the STOXX 600 up 0.7% despite a slightly weaker-than-expected Manufacturing PMI reading that remained in contraction territory.

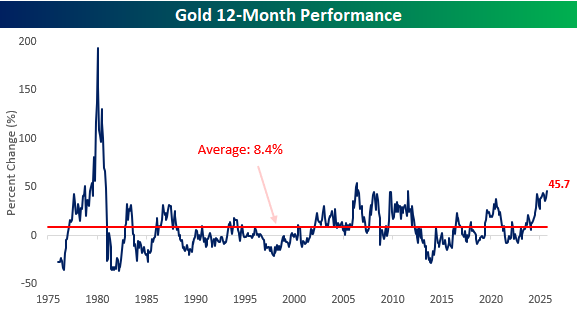

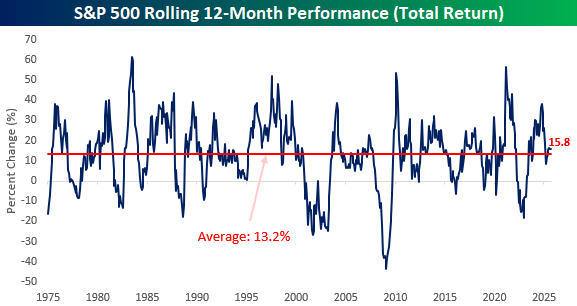

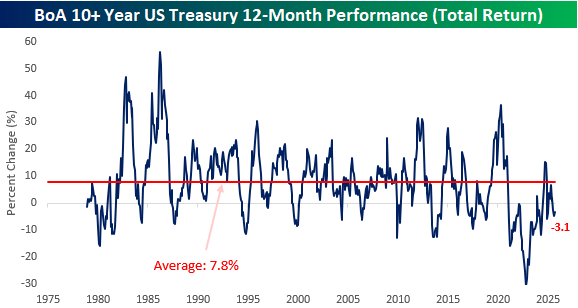

As we head into the final quarter of the year, we wanted to take a look at the 12-month moves of some major asset classes over the last five decades to see how the recent moves stack up relative to history.

Starting with equities, the S&P 500’s total return of 15.8% over the last year is surprisingly only modestly better than the long-term average of 13.2%, ranking in just the 53rd percentile relative to history. Last year at this time, the trailing 12-month return was over 35%!

Treasury yields remain stuck in their bear market. While a decline of 3% doesn’t really seem like a big deal, we’re talking about treasuries here – traditionally referred to as a risk-free asset. Not only that, but the average 12-month return has been closer to 8%, and there have only been two months in the last five years when the trailing 12-month return was better than the long-term average.

Gold is off to one of the hottest starts in decades this year, and over the last 12 months, its 45.7% gain ranks as the strongest since the mid-2000s, and the only period where there was a significantly larger 12-month gain was in the late 1970s/early 1980s.