See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Tomorrow belongs to those who can hear it coming” – David Bowie

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It looks like a negative start to the Thursday session for equities, as the S&P 500 and Nasdaq both decline between 0.2% and 0.3%, while Treasury yields tick higher with the 10-year yield up to 4.16%. Oil prices bounced 1.5%, but WTI still trades below $57 per barrel. In the metals space, there’s broad-based weakness with gold down about 1%, copper down fractionally, while silver and platinum both fall 4%. After a rally to start the year that took its price over $90K, Bitcoin is back down below $90K. The only data on the economic calendar today are jobless claims at 8:30, along with Nonfarm Productivity and Unit Labor Costs at the same time.

The weakness in US futures follows a weak session in Asia, where Japan, Hong Kong, and India were all down 1%. Despite the declines, South Korea managed to outperform again, finishing unchanged on the session as Samsung Electronics reported better than expected results.

In Europe, stocks are also lower with the STOXX 600 trading down 0.4%, with Spain the only positive outlier. December Business and Consumer Confidence pulled back modestly more than expected as the headline index fell from 97.1 down to 96.7, versus forecasts for a level of 97.0.

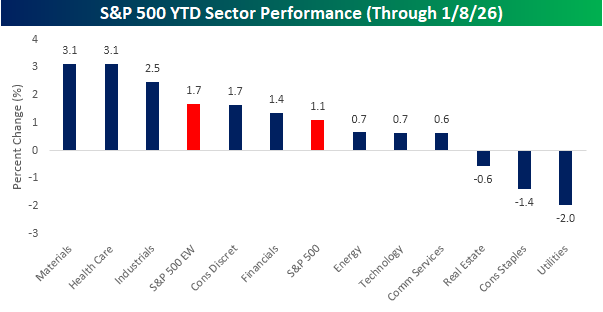

We’re four trading days into the year, and already there have been some big individual stock winners. Within the S&P 500, 22 stocks are already up over 10% YTD, while none are down 10%, and only 25 are down by 5% or more. In total, breadth in the market has been positive as 316 of the index’s 500 components are up YTD. The positive breadth is also illustrated by the fact that the equal-weight S&P 500 index is up 1.7% YTD compared to a gain of 1.1% for the cap-weighted index.

At the sector level, five are outperforming the index YTD, while six lag. Leading the way to the upside, Materials and Health Care are both up 3.1%, followed by Industrials with a gain of 2.5%. Technology’s 0.7% gain modestly trails the index, and three sectors – Utilities, Consumer Staples, and Real Estate are all down after four days of trading.

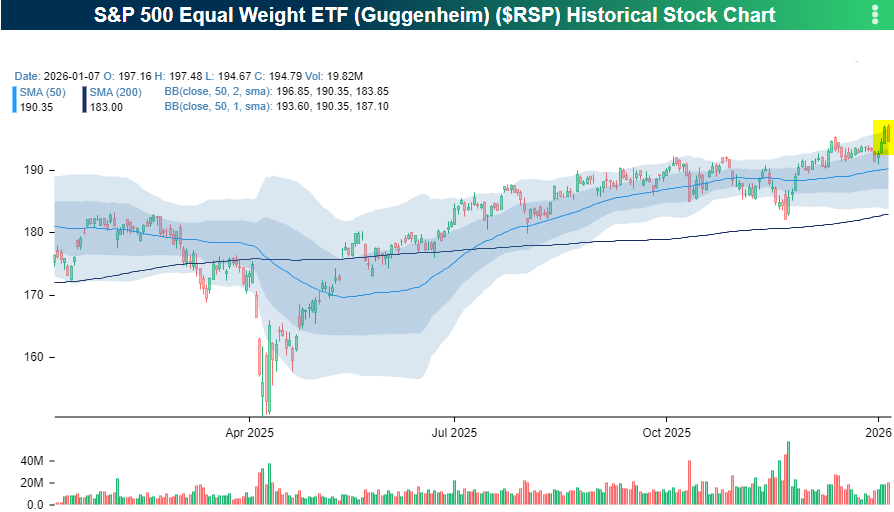

Before yesterday, breadth in the market was even stronger, but while the S&P 500 had a modest decline of 0.34%, the equal-weight index fell more than 1%. That decline also erased nearly all of what was looking like a breakout in the equal-weight index after a multi-month period of sideways trading. Every time it seems like the rally will broaden, Lucy goes in and swipes the football away.