See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“You can fool some of the people some of the time — and that’s enough to make a decent living.” – W.C. Fields

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It was only a 0.01% decline, but the S&P 500’s drop yesterday ended a streak of five straight gains. The Nasdaq managed to finish up 0.17%, extending its winning streak to six. This morning, both indices are trading higher, so for the Nasdaq will today be lucky number seven? While Meta (META) and Tesla (TSLA) are doing their part to extend the Nasdaq’s streak, Microsoft (MSFT) is trading the other way after weak margin guidance has that hyperscaler trading down a not so lucky 7% this morning.

Outside of treasuries, the 10-year US Treasury yield is basically unchanged at 4.25%, while the dollar is little changed after a volatile few days to start the week. Precious metals continue to get more precious this morning, with gold up over 4% and breaking through $5,500 per ounce. Silver is up over 5%, platinum is up nearly 5%, and copper is also at a record, trading up close to 7%. For all three metals, their year-to-date gains are leaving equities in the dust.

In Asia overnight, the Nikkei was basically unchanged, but South Korea rallied another 1% as SK Hynix reported strong Q4 results. Hong Kong, China, and India were also higher on the session, while Australia had a marginal decline.

European stocks are mostly higher this morning as the STOXX 600 gains 0.5%, but Germany has been a major outlier with a decline of nearly 1% as earnings results from SAP weigh on the DAX. A January survey of Business and Consumer sentiment came in stronger than expected, showing an unexpected increase relative to December.

With the Federal Reserve behind us, investors will now turn back to earnings and economic data. Earnings this morning have been OK, with EPS and revenue beat rates for the morning coming in at about 67%. The economic calendar is also busy with Non-Farm Productivity, Unit Labor Costs, and jobless claims at 8:30, followed by Factor Orders and Wholesale Inventories at 10 AM.

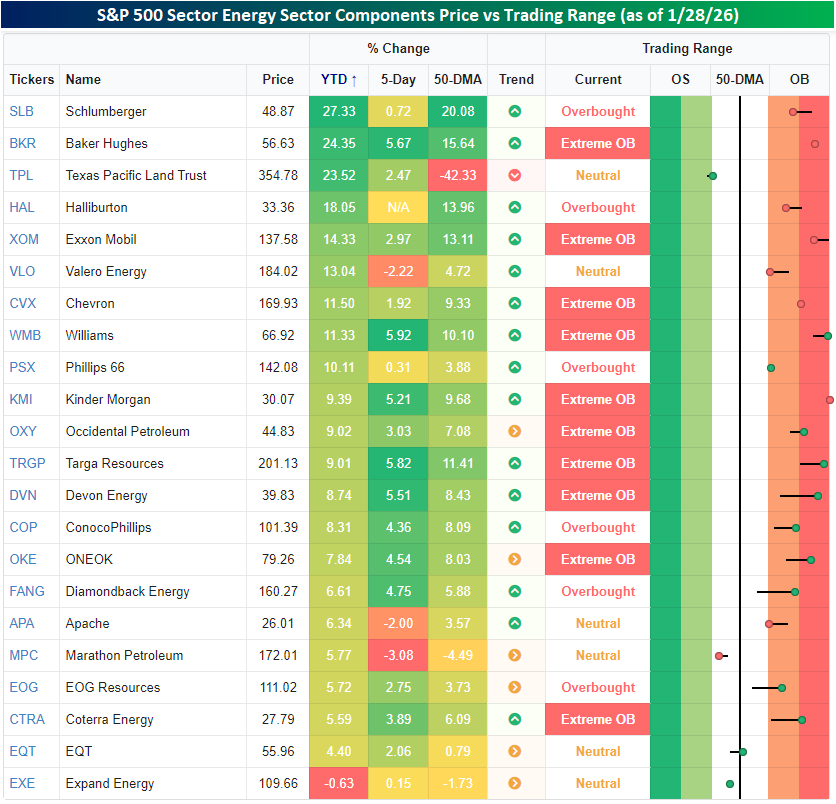

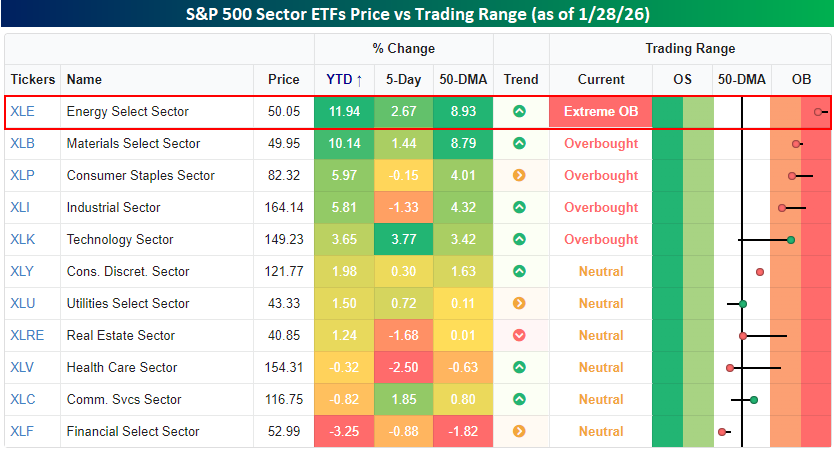

In yesterday’s note, we highlighted the strength in the Energy and Materials sectors and how they were leading all other sectors in terms of year-to-date returns. Through yesterday’s close, Energy and Materials were still leading the performance derby, but Energy is the only sector that remains in ‘extreme’ overbought territory (more than two standard deviations above its 50-DMA). Behind Technology, which has had a run this week, Energy is also the best-performing sector over the last five trading days.

Crude oil prices are up over 12% this year, and natural gas enjoyed a surge during the cold snap, although the contract roll has brought front-month futures prices back down to a three-handle this morning. You don’t have to look any further than these moves in the underlying commodities to understand why energy stocks are doing so well, but strength within the sector, while broad-based, hasn’t been uniform.

As shown in the snapshot below, all but one of the sector’s 20+ components are up YTD. The only outlier is Expand Energy (EXE), which is fractionally lower for the year. On the upside, the two leading stocks in the sector this year have been Schlumberger (SLB) and Baker Hughes (BKR), with gains of more than 20%. Both stocks gapped sharply higher following the early January arrest of Maduro in Venezuela and basically haven’t looked back since. Of the nine stocks in the sector up at least 10%, though, there’s been a smorgasbord of exploration companies, integrated oil companies, and even refiners.