See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I skate to where the puck is going to be, not where it has been.” – Wayne Gretzky

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As much of the country digs and/or scrapes out from the snow and ice over the weekend, it’s a very lackluster morning for US equity futures. The S&P 500 looks to open 6 bps lower, while the Nasdaq is down slightly more at 19 bps. It’s worth noting, though, that both indices are well off their overnight lows. Treasury yields have a downward bias, with the 10-year yield trading down to 4.22%. Crude oil is slightly lower at just under $61 per barrel, but natural gas is surging more than 10% as it has nearly doubled in price over the last ten days as the US continues to fall into the grip of a severe cold snap. Everything is hot in the metals space, though, as gold now trades above $5,000 per ounce, while silver rallies 8% and platinum gains another 4%. Crypto continues to sit this rally out, though. While it’s higher this morning, those gains follow weakness over the weekend.

Although the Hang Seng managed a slight gain, most other Asian benchmarks were lower to start the week, although Australia and India were closed for a holiday. The Nikkei declined 1.8%, and even South Korea declined 0.8%. The declines in Japanese stocks came as the Yen followed through from Friday’s rally and rallied another 1% on speculation of a possible intervention on the horizon to halt the long-term slide in the currency (more on that below). Chinese stocks were only down fractionally, but there were some reports of possible disagreements between President Xi and one of his top generals, resulting in the removal of the general and other military members.

There’s not a lot going on in European markets as the STOXX 600 is basically unchanged, but most major individual indices are slightly higher.

On the US calendar, it’s a light day with Durable Goods at 8:30, and there’s no Fedspeak as the Federal Reserve is in its blackout period ahead of Wednesday’s meeting.

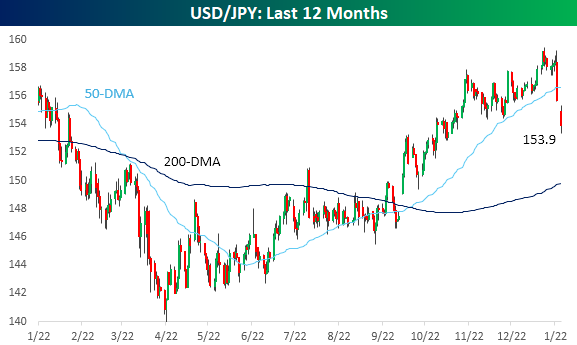

The rally in the yen on Friday took the dollar cross below its 50-day moving average for the first time since early October, and today’s rally has extended those gains to take the currency to its best levels versus the dollar since early November.

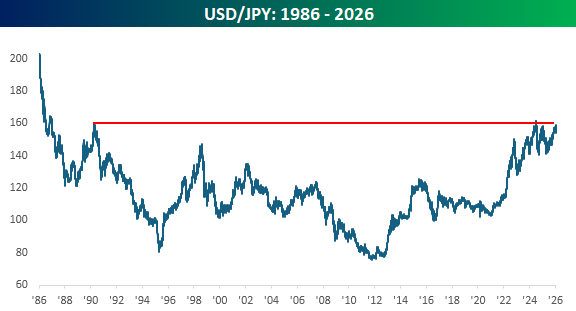

From a longer-term perspective, the rally in the yen has occurred at what is turning into a significant support/resistance level. In more recent history, levels around 160 have acted as support for the yen, and that level also coincides with a peak in the cross (low in the yen) from early 1990. And if you want to get creative, you could even make out what looks like an inverse head and shoulders.

We’ve seen a lot of huge moves in commodities over the last several months, and natural gas has started to get into the act over the last two weeks. Ten calendar days ago, on 1/16, natural gas closed at 3.10 MMBtu. This morning, prices are nearly twice as high, and earlier in the morning, they were double the level of the 1/16 close! Looking at the chart of natural gas and its history in terms of how the commodity has performed following prior short-term spikes, buying natural gas today feels a lot like skating to where the puck is rather than where it’s going. And happy 65th birthday to Wayne Gretzky!