See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I’d say momentum is building around the world. So, ex-US has more momentum, healthy demand, lower vacancies.” – Chris Caton, Prologis

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After yesterday’s turnaround Tuesday on a Wednesday, we’re seeing a healthy amount of follow-through in futures this morning with the S&P 500 indicated to open 0.6% higher while the Nasdaq is up close to 1%. Investors continue to breathe a sigh of relief as an amicable agreement between the US and Europe over Greenland appears to have been reached. Realistically, though, there was never a chance of an armed conflict in the first place. Concerns over Greenland also showed up in the latest sentiment survey from AAII, where bullish sentiment declined sharply to 43.2% from 49.5%. The events of the last few days illustrate once again that investing based on front-page headlines is one of the worst investment strategies we can think of. If you’re going to do that, just save yourself the time and give your money away.

Asian stocks had a positive session following through on the rally in the US yesterday. The Nikkei rallied 1.7%, but no other major benchmark managed to gain more than 1%. The Kospi came close with a gain of 0.9%, and that was enough to close at another record high for the South Korean benchmark. In Australia, a stronger-than-expected unemployment report raised the odds of a rate hike next month. While economists expected the jobless rate to tick up to 4.4%, it dropped two-tenths of a percentage point to 4.1%.

European stocks are also rallying in their morning session as the STOXX 600 rallies almost 1%, and interest rates ease on what is a generally quiet session data-wise, outside of the steady stream of geo-political headlines coming out of Davos.

In terms of US data, it’s a busy morning with a slug of data at 8:30 and another round at 10. The 8:30 data was mostly better than expected with GDP coming in at 4.4% versus forecasts for 4.3%. Personal Consumption and the GDP Price Index were in line with estimates, and jobless claims were lower than expected. At 10 AM, we’ll get Personal Income and Spending and PCE.

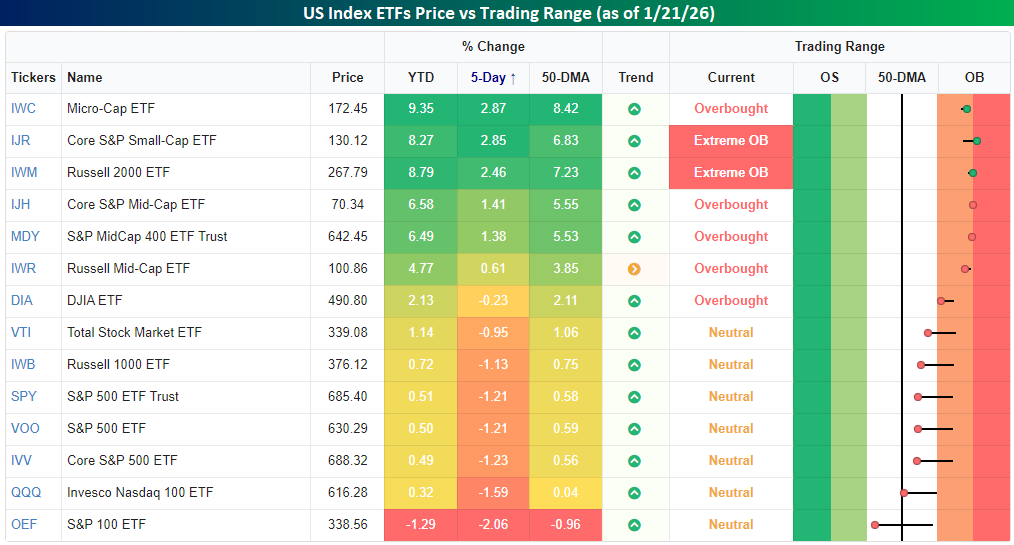

For years now, when you hear the phrase “tale of two markets,” you’ve been conditioned to think of small caps underperforming while large caps lead. You think that, because it’s usually what has happened. So far this year, the phrase a tale of two markets has meant the opposite. As shown in the snapshot from our Trend Analyzer below, small-cap indices are leading with YTD gains of over 5%, while mega-cap and large-cap indices are either in the red or barely hanging on to gains. The S&P 100 ETF (OEF), which essentially tracks the 100 largest stocks in the S&P 500, is down over 1% YTD after falling over 2% in the last week alone!

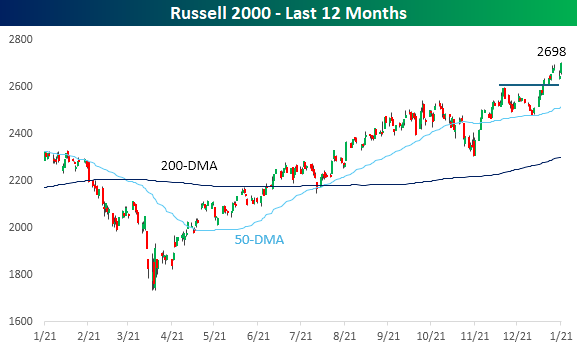

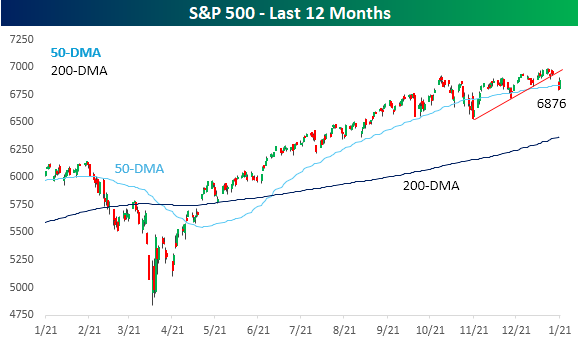

Looking at one-year price charts of the Russell 2000 and S&P 500 shows the disparity. The Russell 2000 closed at an all-time high yesterday and remains in a solid uptrend, but the S&P 500 is trading at the same levels it was at three months ago, barely hanging on to its 50-DMA after breaking a very short-term uptrend earlier in the week.

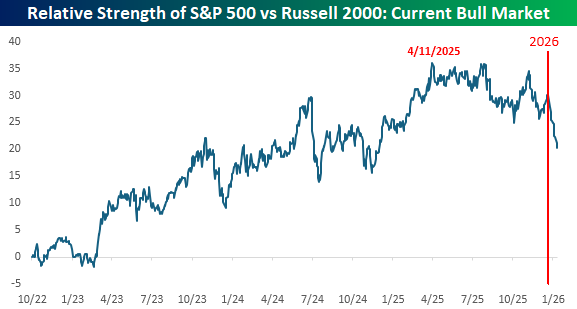

One misnomer about the recent outperformance of small-cap stocks is that it has been solely a 2026 phenomenon. Looking at the relative strength of the S&P 500 versus the Russell 2000 since the bull market started in October 2022 shows a different picture. While large caps started a new leg of underperformance with the turn of the calendar, their relative performance peaked back in April. From that peak through mid-summer, the two indices performed in line with each other for about three months, but ever since early August, large caps have steadily underperformed. If you’re just hopping on the small-cap/broadening bandwagon, where have you been for the last five months?