See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“A country, a style or an epoch are interesting only for the idea behind them.” – Christian Dior

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

The week started on a down note, and as we approach the opening bell for the second trading day of the week, futures aren’t indicating anything in the way of a turnaround, as a previously modestly higher picture has turned red. Treasury yields are basically flat, while crude oil is modestly higher. Investors continue to pile into gold, though, as futures are up another 2%+. Unlike other days when gold rallies, though, other precious metals are seeing much more modest gains. Bitcoin is also lower once again and firmly back below $90K.

Outside of the US, Asian markets were mixed. The Nikkei was down 0.4%, but Hong Kong, China, and South Korea bucked the trend with modest gains. In Europe, the picture is much more uniform as major equity markets are down across the board. The STOXX 600 is down 0.6% with Germany leading the way lower.

For US markets this morning, we’ll get Leading Indicators, Construction Spending, and Pending Home Sales at 10 AM, but the main focus will be on Davos, where President Trump is scheduled to speak right about now.

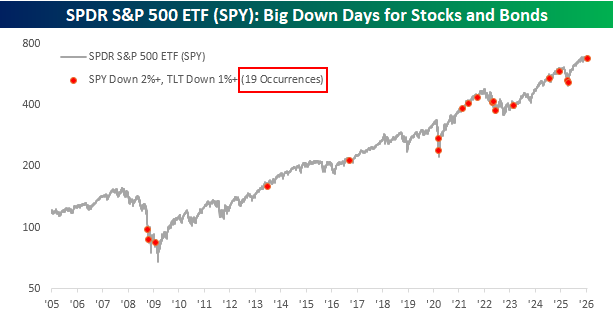

Yesterday was an interesting day in markets as the S&P 500 ETF (SPY) fell over 2% while long-term Treasuries, as proxied by the ETF TLT, also declined by over 1%. On their own, the weakness in both asset classes was hardly unprecedented. Since the start of 2005, there have been 212 other days when SPY fell more than 2%. For TLT, declines like yesterday are even more common, with 627 other one-day drops of at least 1%.

What made yesterday’s drops in both ETFs more notable was that they occurred in tandem with each other. Since the start of 2005, there have only been eighteen other days when SPY fell over 2%, and TLT dropped by more than 1% on the same day. The chart below shows the performance of SPY since the start of 2005, and the red dots indicate each of those other occurrences. There were multiple occurrences near the lows of the Financial Crisis in late 2008/early 2009. From mid-2009 up until the onset of Covid, there were only two other occurrences, but in the post-Covid era, the frequency of occurrences has been much more common as higher inflation has acted as a secular headwind for bonds and a tailwind for gold.

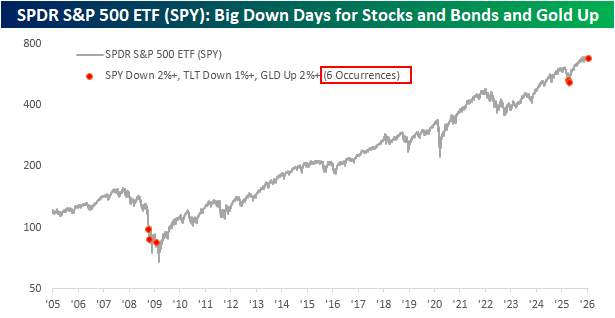

As uncommon as it is for the S&P 500 to drop at least 2% and long-term treasuries (TLT) to fall over 1% on the same day, what makes yesterday even more of an outlier is that Gold also surged more than 2%.

A 2%+ rally in Gold, on its own, isn’t all that uncommon. Yesterday was the 183rd occurrence since the start of 2005 and the 17th in just the last year, but this type of rally practically never happens on a day when the S&P 500 falls over 2% and long-term treasuries fall more than 1%. Since the start of 2005, it’s only happened five other times!

Following the President’s rhetoric towards Europe, and Greenland specifically, over the weekend, concerns over a pickup in the sell America trade started to resurface again yesterday, and the moves in US stocks, bonds, and gold yesterday could easily fit into that narrative. If global investors were looking to “sell America,” this is exactly the type of price action you would expect to see. But if investors were selling America, what were they buying?

Accounting for the losses on Monday when US markets were closed, there wasn’t a lot of buying in global stocks. Europe’s STOXX 600 was down about 2% from Friday’s close through Tuesday, and the Nikkei was down just as much. There wasn’t a lot of buying to be found in international bonds either, as yields in Europe also moved higher, and JGB yields surged to multi-decade highs.

For now, it probably makes more sense to write off yesterday’s moves as a one-off and potentially traders just trying to front-run any potential sell-America trade, but investors should keep a close eye on how the markets react in the days ahead. What makes yesterday’s drops in stocks and bonds while gold rallied stand out even more though, was in where it occurred in the market cycle. As shown in the chart below, of the five other times when SPY fell over 2%, TLT fell more than 1%, and GLD rallied at least 2%, three occurred deep into the Financial Crisis, and the other two occurred right near the lows of the tariff-tantrum. Yesterday’s occurrence came just after the S&P 500 closed the prior session within 1% of an all-time high.