See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“There’s nothing more dangerous than someone who wants to make the world a better place.” – Banksy

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s a banksy type of morning in the US as some of the largest financial institutions in the world start to release Q4 results. JP Morgan (JPM) missed on the top and bottom line, but there werecharges included in the results, and the stock is trading marginally higher. BNY Mellon (BK) reported better-than-expected EPS and sales, and its stock is fractionally lower. The only other major report of the morning was Delta (DAL), which also reported better-than-expected top and bottom-line results, but its stock is down over 3% in the pre-market. So, it’s not necessarily how you report versus expectations that matters.

Drama surrounding Fed Chair Powell and the subpoenas issued has subsided this morning as Jeanine Pirro softened her stance towards the issue, and the White House says they were not made aware of the actions beforehand. For now, it appears as though the story will be one more in a litany of ‘shocking’ headlines that don’t amount to anything.

The big news of the morning was the December CPI, and after questions surrounded the lower-than-expected November print, many were expecting a hot print for December as the integrity of the data that makes up the report improved. They were wrong. Headline CPI was right in line with forecasts while the core reading came in a tenth weaker than expected on both a m/m and y/y basis. In response to the report, futures experienced a modest bounce and are now firmly in positive territory, while Treasury yields are lower. Crude oil is up another 1% this morning as WTI trades back above $60, while gold is basically flat, as other precious metals trade modestly higher. Finally, bitcoin is higher again this morning and trading back above $92K. The gains also follow reports that a Strategy director purchased 5,000 shares of the company’s stock for just under $800K.

In Asia, it was a mixed session. While Japan returned from Monday’s holiday with a monster 3.1% rally, other indices in the region didn’t fare as well. It’s not often that South Korea is a laggard on an up day, but with a gain of ‘only’ 1.5%, it was up less than half as much as Japan. Hong Kong was up just under 1% while China’s Shanghai Composite fell 0.6%. Japanese PM Takaichi plans to hold snap elections next month to solidify her party’s position in parliament, but outside of that, it was a relatively quiet session for news.

In Europe, stocks are modestly lower across the board, with the STOXX 600 down 0.2%. France is leading the way lower but is still down less than 0.5%, while Germany hangs on to the flatline.

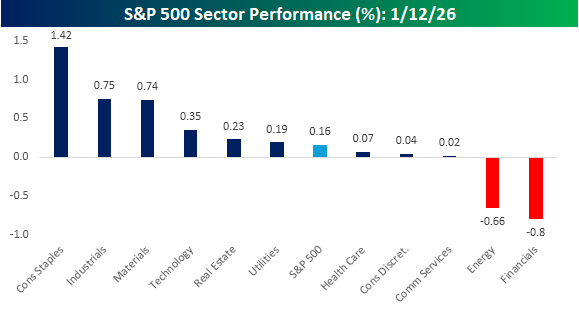

While the banks are the focus of the market’s attention this morning, the standout sector for the last few days has been Consumer Staples, even as the S&P 500 has rallied to new highs. As shown in the chart below, Consumer Staples rallied 1.42% yesterday, which was nearly twice the gain of the next two closest sectors – Industrials and Materials.

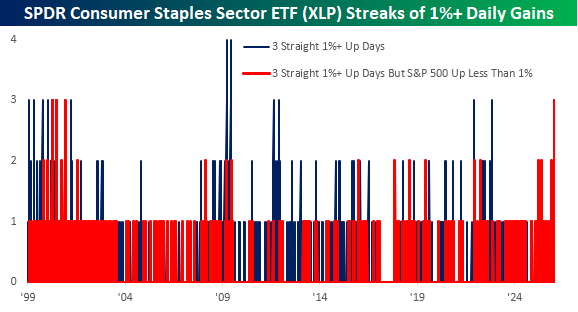

Yesterday’s rally for the sector was the third straight day that it has rallied more than 1% in a single session. The chart below shows prior streaks of 1%+ for the SPDR Consumer Staples sector ETF (XLP), and while there have been plenty of other periods where the ETF rallied at least 1% for three straight sessions, the only streaks that were longer occurred in March and June 2009, coming out of the Financial Crisis lows.

What makes the current streak unique, though, is that all three days of gains have occurred on days when the S&P 500 didn’t rally 1%+. It’s one thing to rally 1% when the broader market is also up at least 1%, but to rally that much when the market isn’t up that much is much more significant. As the red bars in the chart illustrate, the only other times that XLP rallied 1%+ for three days in a row when the S&P 500 wasn’t up 1%+ on any of those three days was back in early 2000, right around and after the dot-com peak. Gulp.