The Closer – CPI, BLS, GLP-1s – 8/12/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a rundown of the CPI data (page 1) followed by some commentary regarding the inflation risk premium (page 2). Afterward, we turn over to commentary regarding the President’s choice of who will lead the BLS (page 3). We then dive into earnings results for restaurant brands (page 4) and next up is a review of breadth as the market hits new highs (page 5). We finish with a dive into the Health Care sector’s weakness with focus on GLP-1s and stocks affected by MAHA (pages 6 – 8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 8/12/25

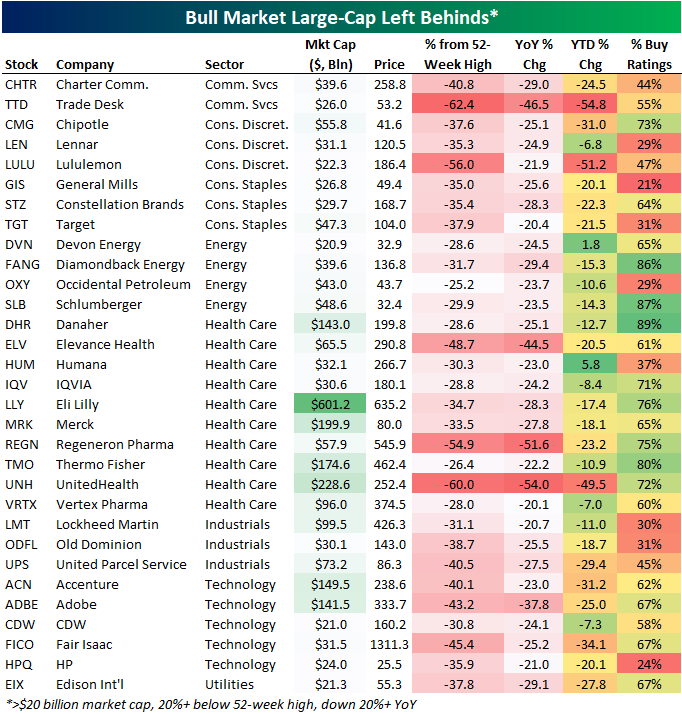

Large-Cap Left Behinds

While major US stock market indices are back to new highs and the bull market continues on, there are some well-known large-cap stocks that have been just plain bad recently. We screened the large-cap S&P 500 for stocks that have market caps greater than $20 billion that are more than 20% below their 52-week highs as well as down 20%+ over the last year. Within the S&P, there are 31 stocks that fit this criteria, which we’ve called the large-cap “left behinds” in the table below.

You can probably think of a few of these recent “dogs” off the top of your head. Some of the once-popular stocks that have been left behind include Trade Desk (TTD), Chipotle (CMG), Target (TGT), Schlumberger (SLB), UnitedHealth (UNH), Lockheed Martin (LMT), UPS, and Adobe (ADBE). This is a pretty diversified group of large-cap stocks covering communication services (TTD), the consumer (CMG, TGT), energy (SLB), health care (UNH), defense (LMT), transports (UPS), and tech (ADBE), but had you built an equally-weighted basket of these names starting a year ago, you’d be down 32%!

If you’re a chart-watcher and want to hold down your lunch, don’t look at the snapshot below which is another sampling of key names in the “Left Behind” table above. These down-on-your-luck stocks have been torched recently and most look like they’ll never find a bottom.

Of course, the name of the game is to buy low and sell high, right? We aren’t sure which ones will make comebacks, but there will likely be a few that you wished you’d bought when revisiting this list of left-behinds a year from now.

Chart of the Day – Japan at New Highs But Little Changed Over the Last 35 Years

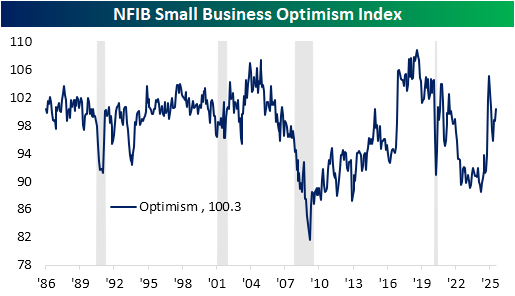

Economic Optimism Returns Among Small Businesses

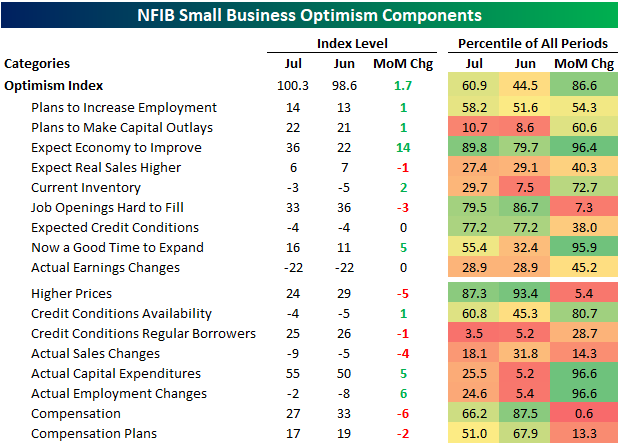

This morning’s release of the NFIB’s Small Business Optimism Index saw a return in positivity. After peaking post-election at 105.1 in December, the headline index went on to fall to a low of 95.8 in April and has since erased about half of that decline. At 100.3 in July, it is back above the historical median and at the highest level since February.

As shown in the table below, breadth throughout the sub-indices of this month’s report was solid, with five inputs to the optimism index rising versus two falling and the remaining two going unchanged month over month. Categories that were not inputs to that headline number saw weaker breadth. Of those, five of the eight were lower month over month, including a couple of bottom decile declines from categories like higher prices and compensation.

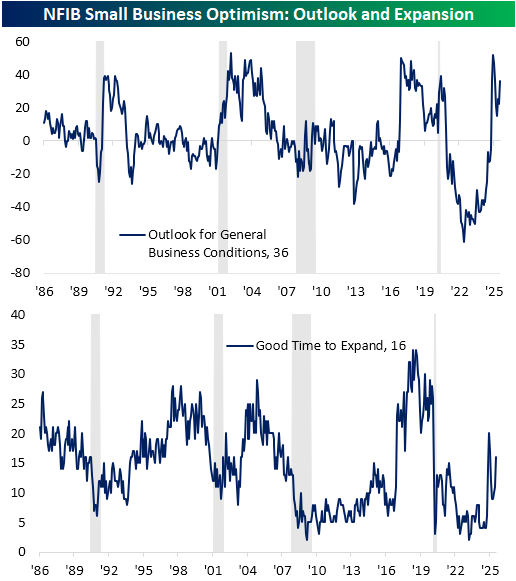

Of the rising categories, two of the most notable were for expectations for the economy to improve and evaluating now as a good time to expand. For the former, the index surged 14 points month over month to 36. While that is only the highest reading since February and the largest one-month gain since December, the monthly gain ranks in the 95th percentile of all monthly moves on record. Similarly, the 5-point jump in seeing now as a good time to expand also ranks highly in the 95th percentile of monthly changes for that index.

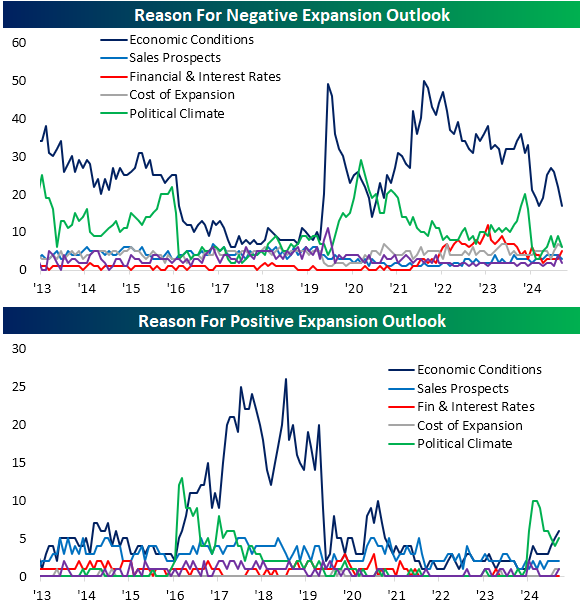

Those two indices appear to be correlated. In other words, when small businesses see the economy as healthier, they will, in turn, see it as a good time to expand. This comes up when looking at the given reasons for different expansion outlooks. For both positive and negative outlooks, economic conditions were the leading reason given as each one was at or tied with multi-year highs and lows. Additionally, as we often note, the NFIB survey has the downside of being politically sensitive. Typically, a Republican administration translates into stronger sentiment and vice versa. With regards to positive expansion outlooks, the political climate is the second most popular reason, and current levels—even though they are off recent highs—are around some of the most elevated readings since the first half of the first Trump administration.

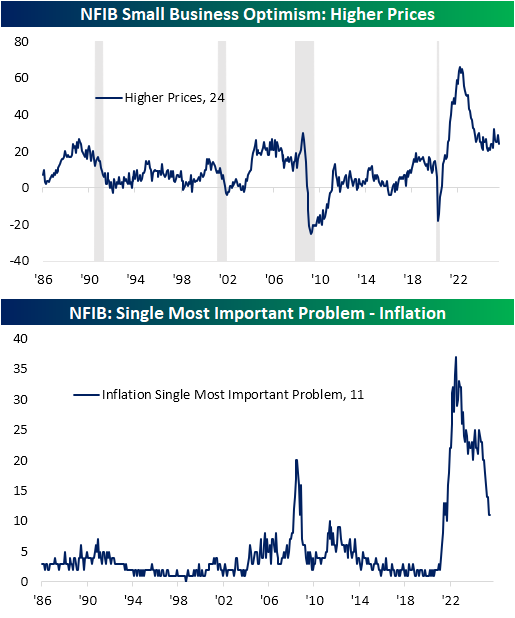

As for indices that declined, one of the bigger drops was for higher prices. While it may not jump out in looking at the chart of the index, that five-point decline ranks as a 5th percentile monthly move for its history, and current levels remain in the middle of the past couple of years’ range since the peak inflation readings in 2021-2023. The reading that points to more substantial progress is with regard to the percentage of firms reporting inflation as their biggest problem. That reading is down to 11%, unchanged month over month, following a number of steep drops in the past year.

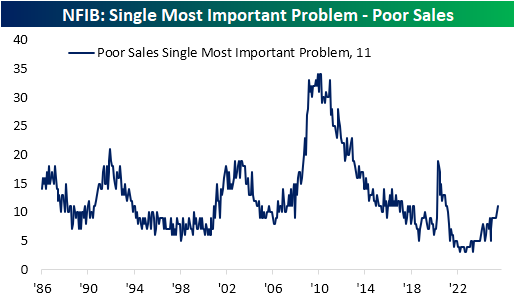

Looking across other most commonly reported problems, an equal share of respondents highlighted poor sales. That is the highest reading since February 2021, when that reading was declining off of pandemic highs. While that may sound concerning, we would note it is not far off the average reading (10.5%) observed in the five years from 2014 through 2019.

Bespoke’s Morning Lineup – 8/12/25 – Micro Caps Have Their Day

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Reading the record, it is striking how many calamities that I anticipated did not in fact materialise.” – George Soros

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

After a quiet day yesterday, futures aren’t doing much this morning either as investors await the release of July CPI. European markets started the day higher but have been selling off throughout the day (sound familiar?), and Asia had a mixed session, although Japan rallied more than 2% after being closed for trading on Monday. While Japanese stocks traded higher, there was literally no trading in Japan’s 10-year JGBs. That was the first time that had happened since March 2023.

July CPI came in right in line with expectations as the headline reading increased 0.2% and core rose 0.3%. On a y/y basis, headline CPI was a tenth weaker than expected at 2.7% while the core reading was a tenth higher than expected (3.1%). The initial reaction to the move was slightly lower yields and higher stock prices.

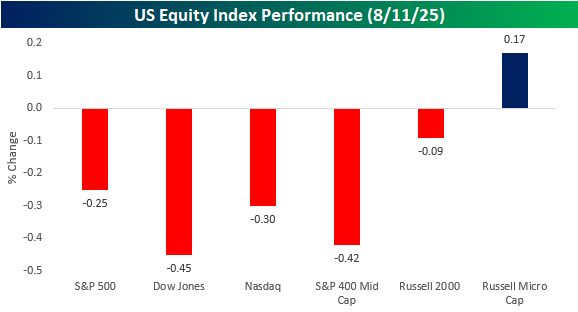

It’s hard to read too much into market activity on a quiet day in August, but the trend of intraday weakness continued to start the week as the S&P 500, as measured by SPY, closed lower than it opened for the tenth time in the last fifteen trading days. When the bell finally rang, the S&P 500 finished down 0.25%, the Dow was down 0.45%, while the Nasdaq fell 0.30%. Besides those major large-cap indices, mid-caps slumped 0.42% while small caps held up relatively well with a decline of 0.09%. The only small ray of sunshine yesterday was in the Russell Microcap Index, which finished the day 0.17% higher. When we say small, we mean it, though. The combined market cap of the companies in the index is just $426 billion, which is smaller than Netflix (NFLX), and the average market cap of companies in the index is under $400 million, with an M!

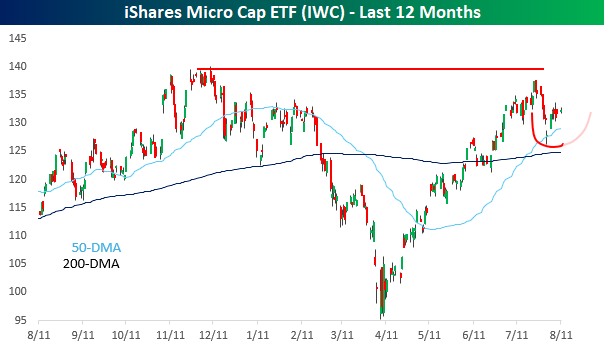

Looking at the performance of micro-caps, as measured by the iShares Microcap ETF (IWC), after testing the Q4 highs in late July, they pulled back to the 50-day moving average, where they bounced to kick off August. It’s still early, but if the bounce holds, the index could be rounding out the right side of a cup and handle formation.

The Closer – Growth and Value, EV Efficiency, Housing – 8/11/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start off by looking at the outperformance of value versus growth overseas and compare that to the two factors’ performance in the US. (page 1). We then discuss the announcement from Ford (F) regarding their manufacturing (page 2). We finish with updates on the latest housing delinquency (page 3) and inventory data (pages 4 and 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 8/11/25

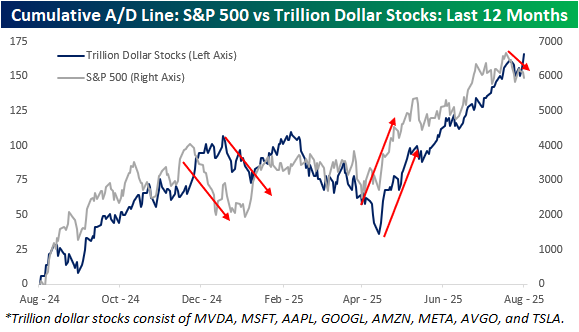

The Rich get Richer

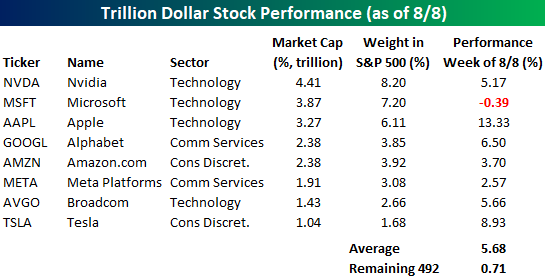

The mega-cap stocks took the baton last week and drove the market higher. While the S&P 500 was up about 2.4%, the 492 stocks in the index with market caps of less than a trillion dollars were up an average of just 0.71%. Meanwhile, the eight $1+ trillion dollar stocks were up an average of 5.7%, led higher by stocks like Apple (AAPL) and Alphabet (GOOGL) with gains of more than 5%. Weren’t these two stocks that the street had written off for dead just a couple of weeks ago?

Collectively, the eight $1+ trillion stocks account for over 35% of the S&P 500. These are, and will continue to be, the main drivers of the market.

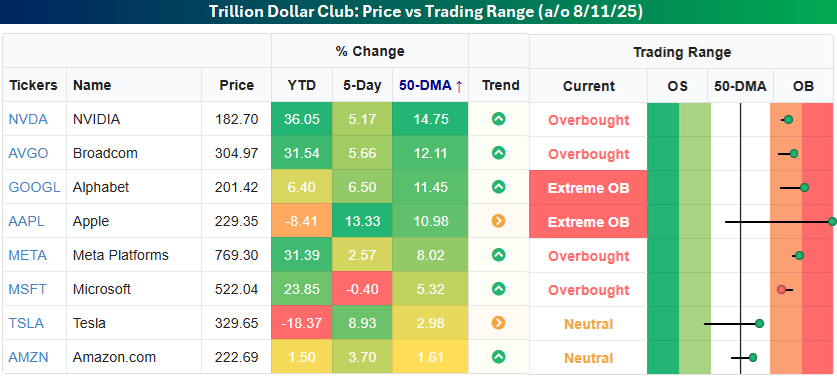

Some of the trillion dollar stocks have gotten quite extended, with Nvidia (NVDA), Broadcom (AVGO), Alphabet (GOOGL), and Apple (AAPL) now trading more than 10% above their 50-day moving averages.

In Thursday’s Morning Lineup, we noted the dispersion in YTD performance using the Dow Jones Industrial Average as an example. Within the trillion-dollar stocks, we’ve seen the same degree of divergence with more than 50 percentage points separating the group’s biggest YTD winner and loser.

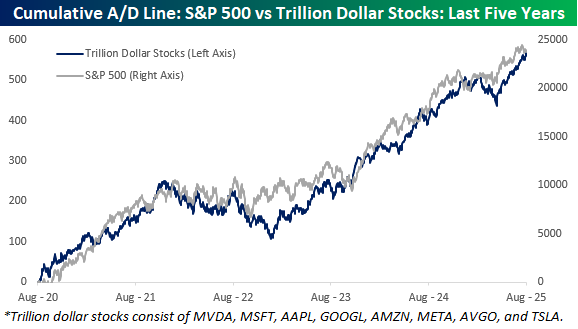

Since the trillion-dollar stocks will have such a large say in how the market moves from here, we wanted to check up on the group’s breadth compared to the S&P 500. The chart below compares the S&P 500’s cumulative A/D line to the cumulative A/D line of the trillion-dollar stocks over the last five years. For the most part, they have tracked each other very closely, and both remain near record highs, so there’s been no major divergence between the mega-caps compared to the rest of the market.

Zooming in on the last year shows similar patterns in both cumulative A/D lines, but with more granularity, you can also see some zigs in the S&P 500’s cumulative A/D line when the cumulative A/D line of the trillion-dollar stocks zags. Late last year, the S&P 500’s cumulative A/D line started to roll over about a month before the trillion-dollar stocks, and then in the Spring, the S&P 500’s A/D line bottomed a couple of weeks before the trillion-dollar stocks. That brings us to last week. As mentioned above, while the S&P 500 was up sharply last week, the majority of the gains were the result of the big moves higher in the trillion-dollar stocks. That divergence was also evident in the cumulative A/D lines as the S&P 500 finished the week well off its 7/25 high, while the one for the trillion-dollar stocks hit a new high. At this point, it’s just a modest divergence, but the last two divergences began modestly as well before turning into more extended moves.